Strategi Stop Loss Dinamis dan Target Profit Tingkat Lanjut

Ringkasan

Strategi ini adalah sistem perdagangan tingkat lanjut yang menggabungkan trailing stop loss dinamis, rasio risk-reward, dan keluar berdasarkan ekstrem RSI. Strategi ini melakukan perdagangan dengan mengidentifikasi formasi tertentu di pasar (formasi lilin paralel dan formasi lilin jarum), sekaligus menggunakan ATR dan titik terendah terbaru untuk menetapkan stop loss dinamis, serta menentukan target keuntungan berdasarkan rasio risk-reward yang telah ditentukan. Sistem ini juga mengintegrasikan mekanisme penilaian pasar terlalu panas/terlalu dingin berdasarkan indikator RSI, yang memungkinkan penutupan posisi secara tepat waktu saat pasar mencapai nilai ekstrem.

Prinsip Strategi

Logika inti strategi ini mencakup beberapa bagian penting berikut:

- Sinyal masuk didasarkan pada dua formasi: formasi lilin paralel (lilin besar bullish diikuti lilin besar bearish) dan formasi lilin jarum ganda.

- Trailing stop loss dinamis menggunakan pengali ATR untuk menyesuaikan harga terendah dari N lilin terbaru, memastikan level stop loss dapat beradaptasi secara dinamis dengan volatilitas pasar.

- Target keuntungan ditetapkan berdasarkan rasio risk-reward tetap, ditentukan dengan menghitung nilai risiko (R) setiap transaksi.

- Ukuran posisi dihitung secara dinamis berdasarkan jumlah risiko tetap dan nilai risiko setiap transaksi.

- Mekanisme keluar berdasarkan ekstrem RSI memicu sinyal penutupan posisi saat pasar terlalu panas atau terlalu dingin.

Keunggulan Strategi

- Manajemen risiko dinamis: Dengan menggabungkan ATR dan titik terendah terbaru, level stop loss dapat menyesuaikan secara dinamis dengan volatilitas pasar.

- Kontrol posisi yang presisi: Metode perhitungan posisi berdasarkan jumlah risiko tetap memastikan risiko setiap transaksi konsisten.

- Mekanisme keluar multidimensi: Menggabungkan tiga mekanisme keluar yaitu trailing stop, target profit tetap, dan ekstrem RSI.

- Fleksibilitas arah perdagangan: Dapat memilih hanya long, hanya short, atau perdagangan dua arah.

- Pengaturan risk-reward yang jelas: Target keuntungan setiap transaksi ditentukan dengan jelas melalui rasio risk-reward yang telah ditetapkan.

Risiko Strategi

- Risiko akurasi identifikasi formasi: Identifikasi lilin paralel dan lilin jarum mungkin mengalami kesalahan penilaian.

- Risiko slippage pada pengaturan stop loss: Pasar dengan volatilitas tinggi dapat menghadapi slippage yang signifikan.

- Keluar berdasarkan ekstrem RSI mungkin terlalu dini: Dalam tren pasar yang kuat, hal ini dapat menyebabkan keluar lebih awal dan kehilangan potensi keuntungan lebih lanjut.

- Keterbatasan rasio risk-reward tetap: Rasio risk-reward optimal dapat berbeda dalam kondisi pasar yang berbeda.

- Risiko overfitting pada optimasi parameter: Kombinasi banyak parameter dapat menyebabkan optimasi berlebihan.

Arah Optimasi Strategi

- Optimasi sinyal masuk: Dapat menambahkan lebih banyak indikator konfirmasi formasi, seperti volume perdagangan, indikator tren, dll.

- Rasio risk-reward dinamis: Menyesuaikan rasio risk-reward secara dinamis berdasarkan volatilitas pasar.

- Adaptasi parameter cerdas: Memperkenalkan algoritma pembelajaran mesin untuk optimasi parameter secara dinamis.

- Konfirmasi multi-time frame: Menambahkan mekanisme konfirmasi sinyal dari lebih banyak kerangka waktu.

- Klasifikasi lingkungan pasar: Menggunakan kombinasi parameter yang berbeda sesuai dengan kondisi pasar yang berbeda.

Kesimpulan

Ini adalah strategi perdagangan yang dirancang dengan baik, yang membangun sistem perdagangan lengkap dengan menggabungkan beberapa konsep analisis teknis yang matang. Keunggulan strategi ini terletak pada sistem manajemen risiko yang komprehensif dan aturan perdagangan yang fleksibel, tetapi perlu diperhatikan juga masalah optimasi parameter dan adaptasi pasar. Melalui arah optimasi yang disarankan, strategi ini masih memiliki ruang untuk peningkatan lebih lanjut.

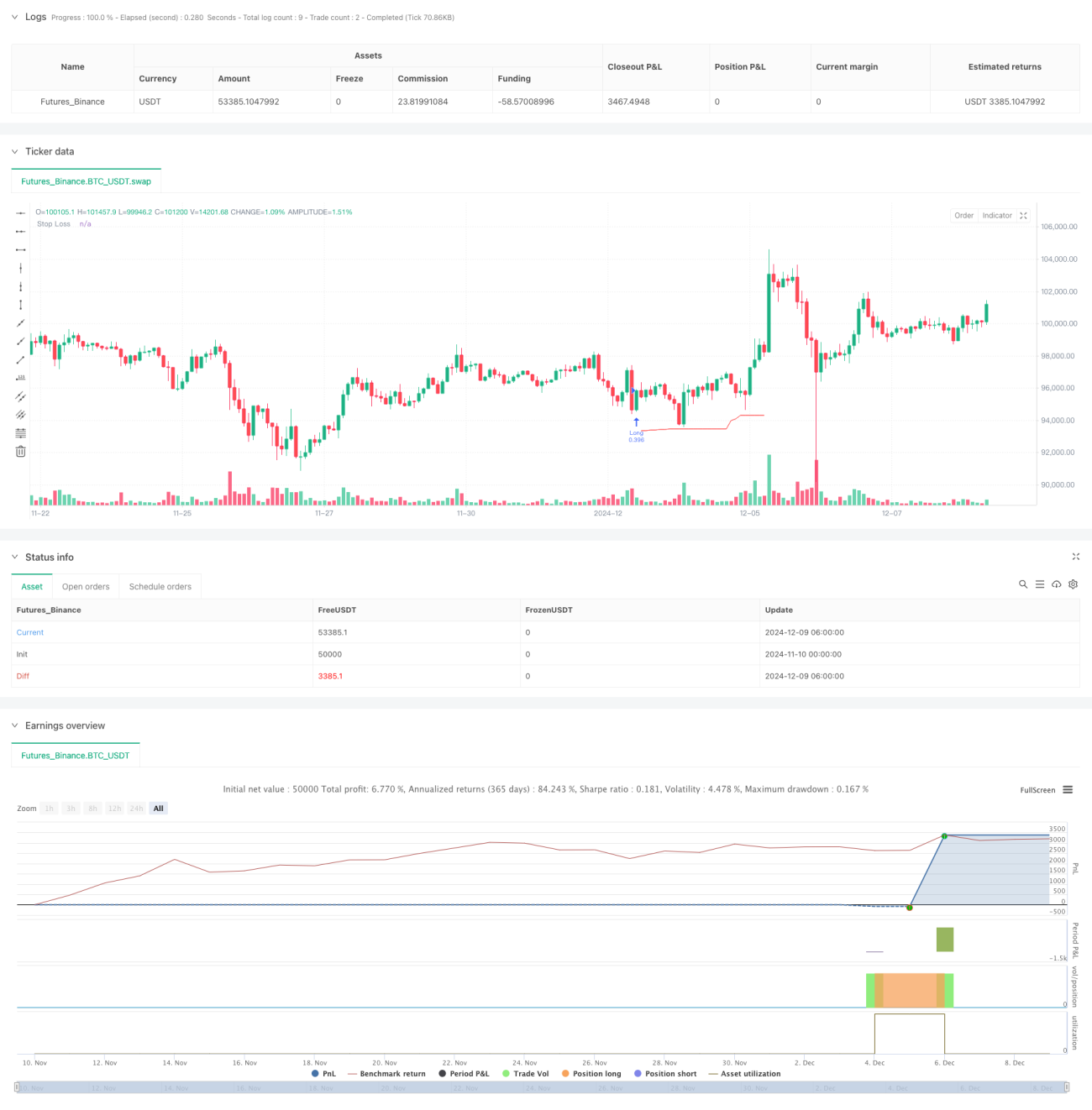

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading | www.TheArtOfTrading.com

// @version=5

strategy("Trailing stop 1", overlay=true)- 1