Strategi Stop Loss dan Take Profit Adaptif untuk Trading Ekuilibrium dengan Trailing Drawdown

Ikhtisar

Strategi ini adalah sistem trading adaptif berbasis gap dan perubahan harga, yang mencapai keuntungan stabil dengan menetapkan titik masuk yang fleksibel serta stop loss dan take profit dinamis. Strategi ini menggunakan metode pyramiding (penambahan posisi bertahap) dan menggabungkan sistem manajemen order OCA untuk mengendalikan risiko. Sistem secara otomatis menyesuaikan arah posisi berdasarkan pergerakan pasar, dan menutup posisi tepat waktu saat sinyal pembalikan muncul.

Prinsip Strategi

Strategi ini beroperasi terutama melalui mekanisme inti berikut:

- Mekanisme Trading Gap: Mengidentifikasi gap naik dan turun, menempatkan order stop loss untuk masuk pada posisi gap.

- Pengikut Tren: Menentukan arah tren berdasarkan hubungan antara harga pembukaan dan penutupan.

- Pyramiding: Memungkinkan maksimal 100 order terbuka pada arah yang sama.

- Take Profit/Stop Loss Dinamis: Menetapkan level take profit dan stop loss secara dinamis berdasarkan harga rata-rata posisi.

- Manajemen Order OCA: Menggunakan order kombinasi OCA untuk memastikan order take profit dan stop loss saling eksklusif.

- Batasan Trading Harian: Mengontrol risiko dengan menetapkan jumlah maksimum order yang dieksekusi dalam sehari.

Keunggulan Strategi

- Kemampuan Adaptasi Tinggi: Strategi dapat secara otomatis menyesuaikan arah trading dan ukuran posisi sesuai dengan kondisi pasar.

- Risiko Terkendali: Risiko dikendalikan melalui berbagai mekanisme, termasuk stop loss, order OCA, dan batasan trading harian.

- Fleksibilitas Tinggi: Mendukung pyramiding, memungkinkan perolehan keuntungan lebih besar dalam tren yang kuat.

- Efisiensi Eksekusi Tinggi: Menggunakan order stop loss untuk masuk, memungkinkan pembukaan posisi cepat pada level harga kunci.

- Tingkat Sistematisasi Tinggi: Keputusan trading sepenuhnya sistematis, mengurangi dampak emosional dari campur tangan manusia.

Risiko Strategi

- Risiko Slippage: Mungkin menghadapi slippage parah dalam kondisi pasar yang cepat.

- Risiko Overtrading: Seringnya masuk dan keluar pasar dapat menyebabkan biaya trading yang tinggi.

- Risiko Sistemik: Dalam pasar yang sangat volatil, kerugian besar mungkin terjadi.

- Risiko Manajemen Modal: Pyramiding dapat menyebabkan penggunaan modal yang terlalu tinggi.

- Risiko Teknis: Gangguan dalam eksekusi program dapat menyebabkan masalah pada manajemen order.

Arah Optimasi Strategi

- Memasukkan Indikator Volatilitas: Menyesuaikan parameter take profit dan stop loss secara dinamis berdasarkan volatilitas pasar.

- Mengoptimalkan Mekanisme Pyramiding: Merancang aturan pyramiding yang lebih rinci untuk menghindari penggunaan modal berlebihan.

- Menyempurnakan Sistem Manajemen Risiko: Menambahkan lebih banyak indikator risiko, seperti batas drawdown harian maksimum.

- Meningkatkan Eksekusi Order: Mengoptimalkan mekanisme kelipatan order untuk mengurangi dampak slippage.

- Menambahkan Penilaian Sentimen Pasar: Menggabungkan indikator volume perdagangan untuk mengoptimalkan waktu masuk.

Kesimpulan

Ini adalah strategi trading yang dirancang dengan baik dan logis, yang menjamin stabilitas dan keamanan trading melalui berbagai mekanisme. Keunggulan inti strategi ini terletak pada kemampuan adaptasi dan kontrol risikonya, namun tetap perlu mewaspadai risiko yang ditimbulkan oleh volatilitas pasar. Melalui optimasi dan penyempurnaan yang berkelanjutan, strategi ini diharapkan dapat mempertahankan kinerja yang stabil di berbagai kondisi pasar.

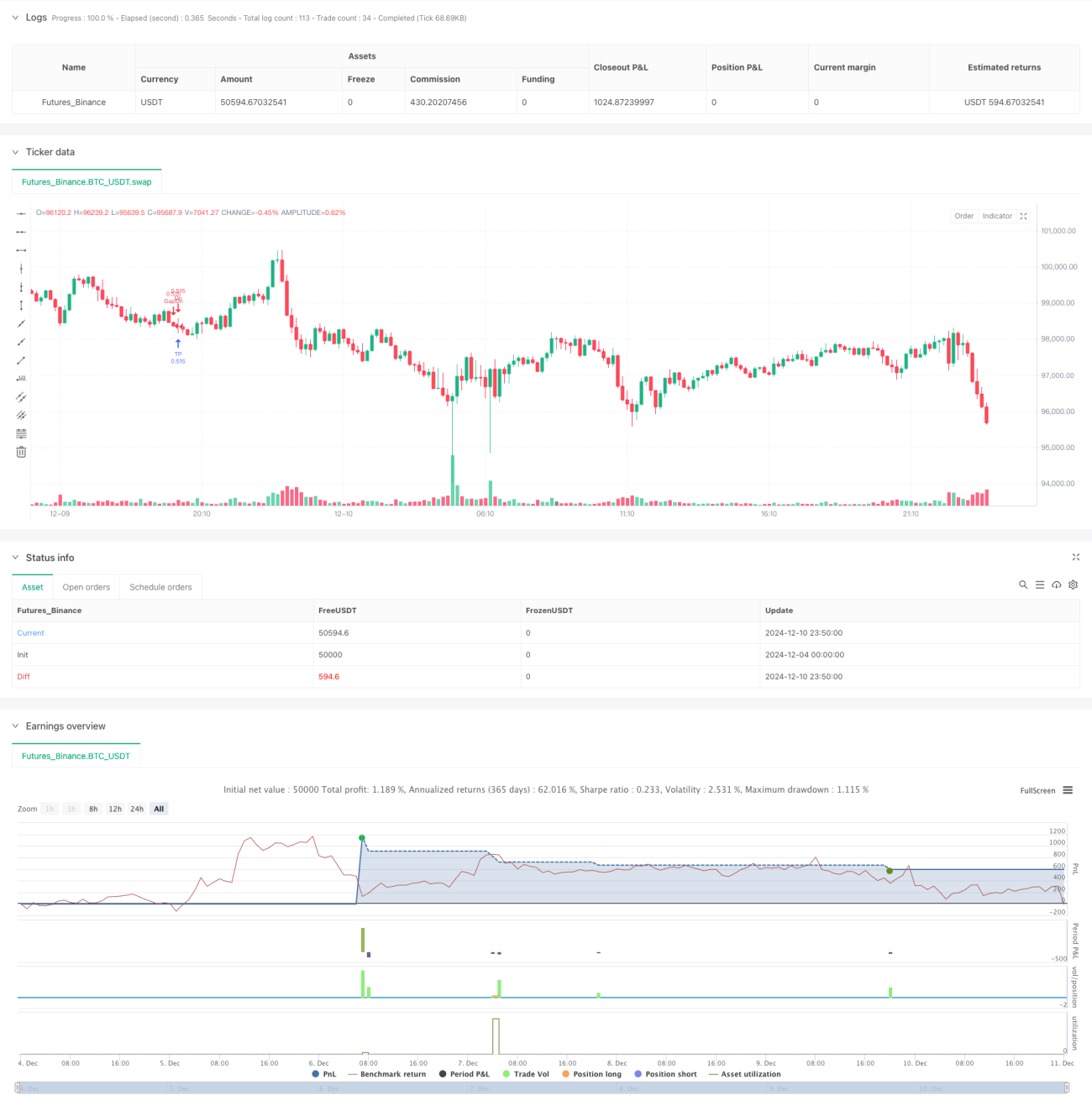

/*backtest

start: 2024-12-04 00:00:00

end: 2024-12-11 00:00:00

period: 10m

basePeriod: 10m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Greedy Strategy - maclaurin", pyramiding = 100, calc_on_order_fills=false, overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

backtestStartDate = input(timestamp("1 Jan 1990"),

title="Start Date", group="Backtest Time Period",- 1