Strategi Trading Pengikut Tren dan Pembalikan Harga Keseimbangan Ganda

Ikhtisar Strategi

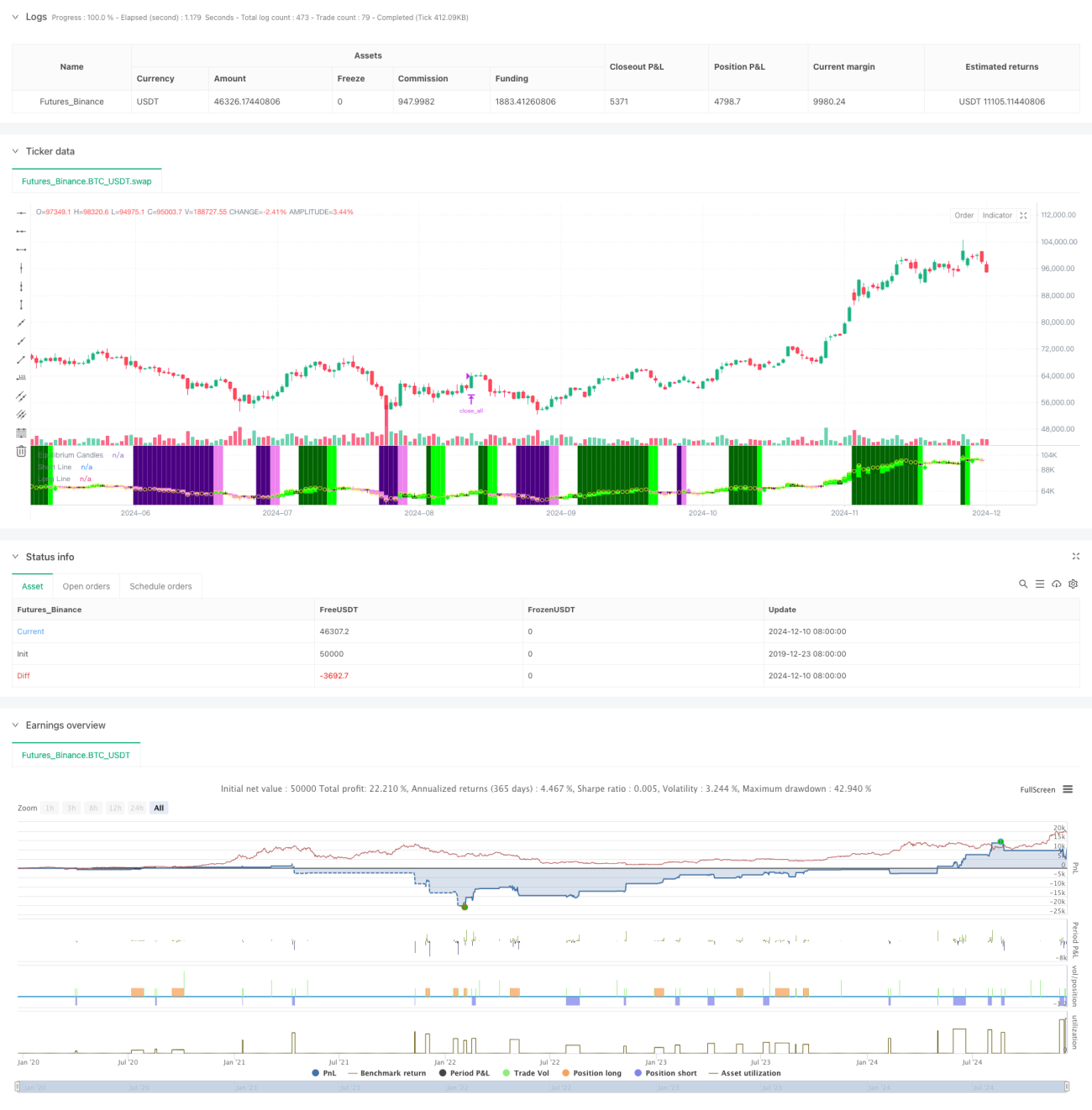

Strategi ini adalah sistem perdagangan yang menggabungkan trend following dan reversal trading berdasarkan titik keseimbangan harga. Harga keseimbangan dihitung dengan mencari nilai tengah dari harga tertinggi dan terendah dalam X candle terakhir, dan arah tren ditentukan berdasarkan posisi harga penutupan relatif terhadap harga keseimbangan. Ketika harga terus-menerus berada di satu sisi harga keseimbangan selama jumlah candle yang ditentukan, sistem akan menganggap tren telah terbentuk. Peluang masuk akan dicari pada saat pullback pertama (ketika harga menembus harga keseimbangan). Strategi ini dapat dipilih untuk beroperasi dalam mode trend following atau reversal trading sesuai dengan pengaturan.

Prinsip Strategi

- Perhitungan Harga Keseimbangan: Menggunakan titik tengah antara harga tertinggi dan terendah dari X candle terakhir sebagai harga keseimbangan, metode ini sama dengan perhitungan garis dasar Ichimoku Cloud.

- Penentuan Tren: Ketika harga terus-menerus berada di sisi yang sama dari harga keseimbangan selama X candle berturut-turut (default 7), maka tren dianggap telah terbentuk.

- Sinyal Masuk: Sinyal masuk dipicu pada saat pullback pertama setelah tren terbentuk (ketika harga menembus harga keseimbangan).

- Stop Loss dan Take Profit: Menggunakan persentil ke-60 dari ATR untuk menyesuaikan jarak stop loss dan take profit secara dinamis, memberikan fleksibilitas dalam manajemen risiko.

- Perlindungan Fluktuasi Ekstrem: Ketika harga menyimpang dari titik keseimbangan melebihi kelipatan ATR yang ditentukan, sistem akan secara otomatis menutup posisi untuk mencegah drawdown yang besar.

Keunggulan Strategi

- Adaptif: Dapat secara fleksibel beralih antara mode trend following dan reversal trading sesuai dengan karakteristik pasar.

- Manajemen Risiko yang Baik: Menggunakan stop loss ATR dinamis dan dilengkapi dengan mekanisme perlindungan fluktuasi ekstrem.

- Operasi yang Jelas: Sinyal perdagangan yang jelas, tidak bergantung pada kombinasi indikator teknis yang kompleks.

- Visualisasi yang Baik: Menggunakan candle berwarna dan latar belakang untuk memberikan tampilan status pasar yang intuitif.

- Ramah untuk Otomatisasi: Dapat dengan mudah diintegrasikan dengan platform perdagangan seperti MT5 untuk perdagangan otomatis.

Risiko Strategi

- Risiko Pasar Ranging: Dapat menghasilkan sinyal palsu yang sering terjadi di pasar yang bergerak sideways atau ranging.

- Pengaruh Slippage: Mungkin menghadapi slippage yang signifikan selama volatilitas tinggi.

- Sensitivitas Parameter: Parameter inti seperti periode keseimbangan, siklus penentuan tren, dll., perlu dioptimalkan secara hati-hati untuk pasar yang berbeda.

- Risiko Transisi Pasar: Periode transisi pasar dari tren ke ranging dapat menyebabkan drawdown yang besar.

Arah Optimasi Strategi

- Identifikasi Lingkungan Pasar: Menambahkan modul penilaian lingkungan pasar untuk menyesuaikan parameter strategi secara dinamis dalam kondisi pasar yang berbeda.

- Filter Sinyal: Pertimbangkan untuk menambahkan indikator tambahan seperti volume perdagangan dan volatilitas untuk menyaring sinyal palsu.

- Manajemen Posisi: Perkenalkan mekanisme manajemen posisi yang lebih kompleks, seperti penyesuaian dinamis berdasarkan volatilitas.

- Multi-Timeframe: Integrasikan sinyal dari beberapa timeframe untuk meningkatkan akurasi perdagangan.

- Optimasi Biaya Transaksi: Optimalkan waktu masuk dan keluar berdasarkan karakteristik biaya dari berbagai instrumen perdagangan.

Kesimpulan

Ini adalah sistem perdagangan tren yang dirancang dengan baik, menyediakan logika perdagangan yang jelas melalui konsep inti harga keseimbangan. Ciri terbesar dari strategi ini adalah fleksibilitasnya yang tinggi; dapat digunakan baik untuk trend following maupun reversal trading, dan dilengkapi dengan mekanisme pengendalian risiko yang komprehensif. Meskipun mungkin menghadapi tantangan dalam kondisi pasar tertentu, melalui optimasi berkelanjutan dan penyesuaian yang fleksibel, strategi ini diharapkan dapat mempertahankan kinerja yang stabil di berbagai lingkungan pasar.

- 1