Sistem Optimalisasi Pelacakan Sinyal Perdagangan Kuantitatif dan Strategi Keluar yang Beragam

Ikhtisar

Strategi ini adalah sistem perdagangan kuantitatif berdasarkan sinyal LuxAlgo® dan indikator overlay. Ia terutama membuka posisi long dengan menangkap kondisi alarm khusus, dan mengelola posisi dengan menggabungkan beberapa sinyal keluar. Sistem ini memiliki desain modular, mendukung penggunaan kombinasi berbagai kondisi keluar, termasuk trailing stop cerdas, konfirmasi pembalikan tren, dan stop loss persentase tradisional. Selain itu, sistem mendukung penambahan posisi di atas posisi yang sudah ada, memberikan fleksibilitas lebih besar dalam manajemen modal.

Prinsip Strategi

Logika inti strategi terdiri dari beberapa bagian kunci berikut:

- Sistem sinyal masuk: Memicu sinyal masuk long melalui kondisi alarm khusus LuxAlgo®.

- Manajemen penambahan posisi: Secara opsional mengaktifkan fungsi penambahan posisi untuk menambah posisi di atas posisi yang ada.

- Mekanisme keluar multi-level:

- Trailing stop cerdas: Memantau hubungan harga dengan garis trailing cerdas.

- Konfirmasi tren keluar: Termasuk sinyal konfirmasi short dasar dan lanjutan.

- Sinyal keluar bawaan: Memanfaatkan berbagai kondisi keluar dari indikator itu sendiri.

- Stop loss tradisional: Mendukung pengaturan stop loss tetap berdasarkan persentase.

- Manajemen jendela waktu: Menyediakan pengaturan rentang tanggal backtest yang fleksibel.

Keunggulan Strategi

- Manajemen risiko sistematis: Melalui mekanisme keluar multi-level, mengontrol risiko penurunan secara efektif.

- Manajemen posisi yang fleksibel: Mendukung berbagai strategi penambahan dan pengurangan posisi, dapat disesuaikan secara dinamis dengan kondisi pasar.

- Kustomisasi tinggi: Pengguna dapat secara bebas menggabungkan berbagai kondisi keluar untuk menciptakan sistem perdagangan yang dipersonalisasi.

- Desain modular: Setiap modul fungsi relatif independen, memudahkan pemeliharaan dan optimalisasi.

- Dukungan backtest lengkap: Menyediakan pengaturan parameter backtest terperinci, mendukung validasi data historis.

Risiko Strategi

- Risiko ketergantungan sinyal: Strategi sangat bergantung pada kualitas sinyal indikator LuxAlgo®.

- Risiko adaptasi lingkungan pasar: Kinerja strategi dapat bervariasi secara signifikan di berbagai lingkungan pasar.

- Risiko sensitivitas parameter: Kombinasi beberapa kondisi keluar dapat menyebabkan keluar terlalu dini atau kehilangan peluang.

- Risiko likuiditas: Likuiditas pasar yang tidak memadai dapat mempengaruhi eksekusi masuk dan keluar.

- Risiko implementasi teknis: Perlu memastikan operasi indikator dan strategi yang stabil, menghindari kegagalan teknis.

Arah Optimalisasi Strategi

- Optimalisasi sistem sinyal:

- Memperkenalkan lebih banyak indikator teknis untuk konfirmasi sinyal.

- Mengembangkan mekanisme penyesuaian ambang sinyal adaptif.

- Peningkatan kontrol risiko:

- Menambahkan mekanisme stop loss yang adaptif terhadap volatilitas.

- Mengembangkan sistem manajemen posisi dinamis.

- Optimalisasi kinerja:

- Mengoptimalkan efisiensi komputasi, mengurangi konsumsi sumber daya.

- Memperbaiki logika pemrosesan sinyal, mengurangi latensi.

- Perluasan fungsionalitas:

- Menambahkan lebih banyak alat analisis lingkungan pasar.

- Mengembangkan kerangka kerja optimalisasi parameter yang lebih fleksibel.

Kesimpulan

Strategi ini menyediakan solusi lengkap untuk perdagangan kuantitatif dengan menggabungkan sinyal berkualitas tinggi dari LuxAlgo® dan sistem manajemen risiko multi-level. Desain modular dan opsi konfigurasi yang fleksibel memberikannya adaptabilitas dan skalabilitas yang baik. Meskipun ada beberapa risiko bawaan, melalui optimalisasi dan perbaikan berkelanjutan, kinerja keseluruhan strategi masih memiliki ruang peningkatan yang besar. Disarankan bagi pengguna untuk memperhatikan perubahan lingkungan pasar dalam aplikasi praktis, menyesuaikan pengaturan parameter tepat waktu, dan menjaga pemantauan risiko berkelanjutan.

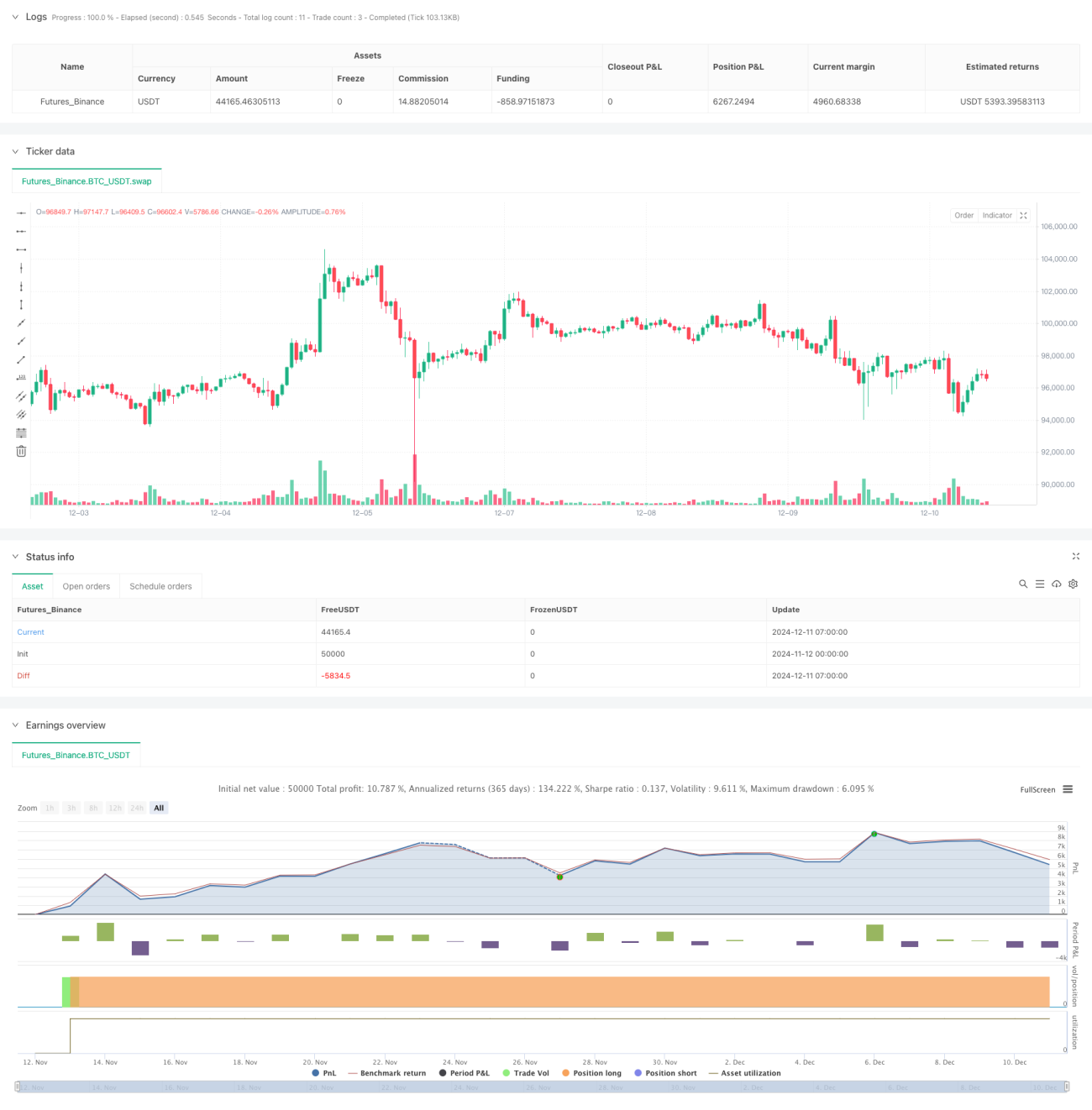

/*backtest

start: 2024-11-12 00:00:00

end: 2024-12-11 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

// This strategy is NOT from the LuxAlgo® developers. We created this to compliment their hard work. No association with LuxAlgo® is intended nor implied.

- 1