Strategi Trend Following Tingkat Lanjut dengan Trailing Stop Loss Adaptif

Gambaran Umum

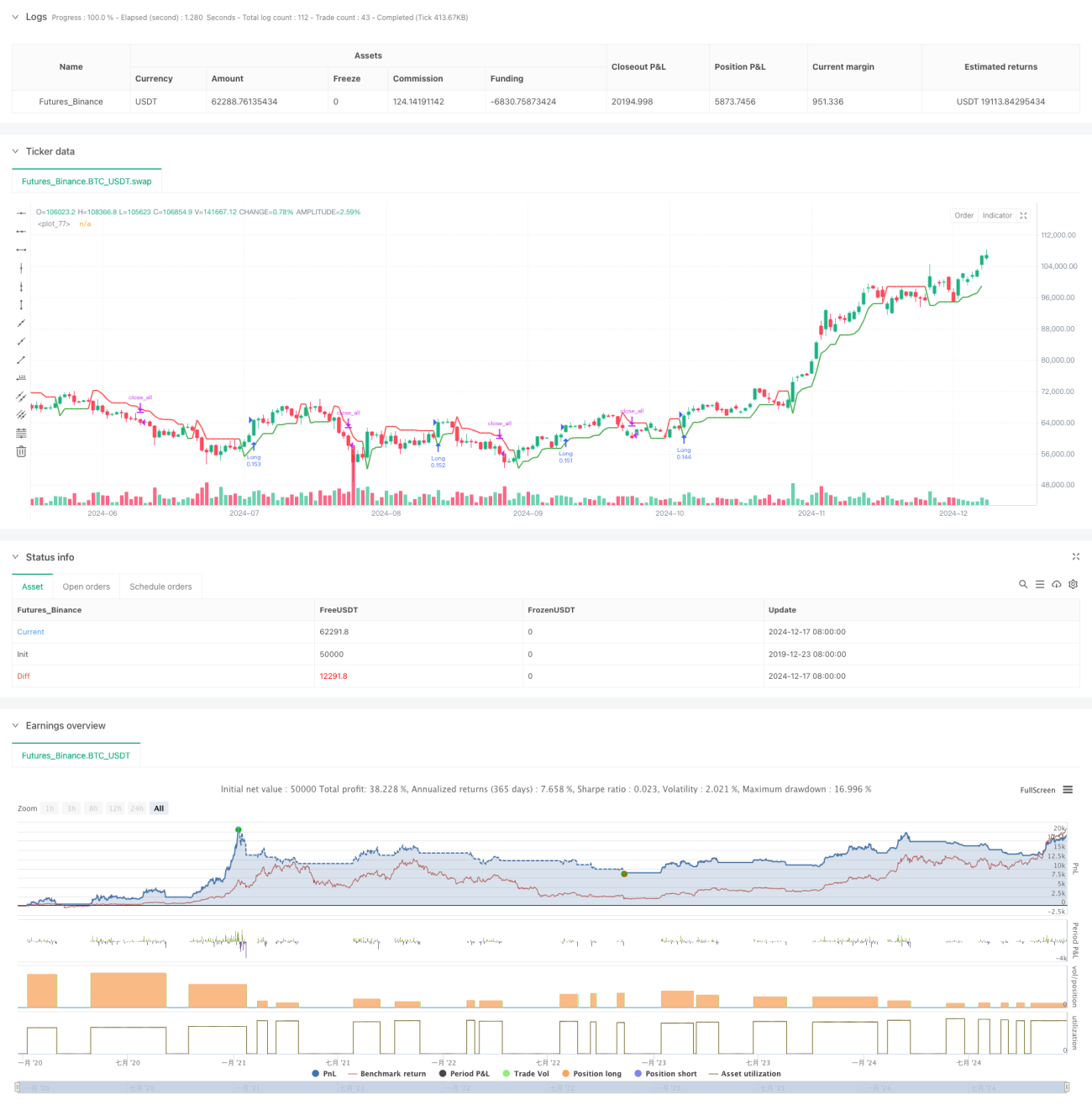

Ini adalah strategi pengikut tren yang didasarkan pada indikator Supertrend, dikombinasikan dengan mekanisme stop loss trailing adaptif. Strategi ini terutama menggunakan indikator Supertrend untuk mengidentifikasi arah tren pasar, dan memanfaatkan stop loss trailing yang disesuaikan secara dinamis untuk mengelola risiko serta mengoptimalkan waktu keluar. Strategi ini mendukung berbagai metode stop loss, termasuk stop loss persentase, stop loss ATR, dan stop loss titik tetap, sehingga dapat disesuaikan secara fleksibel dengan kondisi pasar yang berbeda.

Prinsip Strategi

Logika inti strategi didasarkan pada elemen kunci berikut:

- Menggunakan indikator Supertrend sebagai acuan utama dalam penentuan tren, yang menggabungkan ATR (Average True Range) untuk mengukur volatilitas pasar

- Sinyal masuk dipicu oleh perubahan arah Supertrend, mendukung posisi long, short, atau trading dua arah

- Mekanisme stop loss menggunakan stop loss trailing adaptif yang dapat menyesuaikan posisi stop loss secara otomatis berdasarkan volatilitas pasar

- Sistem manajemen transaksi mencakup manajemen posisi (secara default 15% dari akun) dan filter waktu

Keunggulan Strategi

- Kemampuan menangkap tren yang kuat: Dengan indikator Supertrend, dapat mengidentifikasi tren utama secara efektif, mengurangi kesalahan penilaian

- Pengendalian risiko yang baik: Menggunakan mekanisme stop loss yang beragam, mampu beradaptasi dengan kondisi pasar yang berbeda

- Fleksibilitas tinggi: Mendukung berbagai arah trading dan konfigurasi metode stop loss

- Adaptasi yang kuat: Stop loss trailing akan menyesuaikan secara otomatis berdasarkan volatilitas pasar, meningkatkan kemampuan adaptasi strategi

- Sistem backtest yang lengkap: Dilengkapi dengan fungsi filter waktu, memudahkan analisis kinerja historis

Risiko Strategi

- Risiko pembalikan tren: Dapat menghasilkan sinyal palsu di pasar yang sangat fluktuatif

- Risiko slippage: Eksekusi stop loss trailing mungkin dipengaruhi oleh likuiditas pasar

- Sensitivitas parameter: Pengaturan faktor Supertrend dan periode ATR memiliki dampak besar pada kinerja strategi

- Ketergantungan pada kondisi pasar: Di pasar yang bergerak sideways, dapat menyebabkan perdagangan yang sering dan meningkatkan biaya

Arah Optimasi Strategi

- Optimalisasi filter sinyal: Dapat menambahkan indikator teknis tambahan untuk menyaring sinyal palsu

- Optimalisasi manajemen posisi: Dapat menyesuaikan proporsi posisi secara dinamis berdasarkan volatilitas pasar

- Peningkatan mekanisme stop loss: Dapat menggabungkan harga rata-rata biaya untuk merancang logika stop loss yang lebih kompleks

- Optimalisasi waktu masuk: Dapat menambahkan analisis struktur harga untuk meningkatkan akurasi masuk

- Penyempurnaan sistem backtest: Dapat menambahkan lebih banyak indikator statistik untuk mengevaluasi kinerja strategi

Kesimpulan

Ini adalah strategi pengikut tren yang dirancang dengan baik dan risikonya terkendali. Dengan menggabungkan indikator Supertrend dan mekanisme stop loss yang fleksibel, strategi ini dapat mengendalikan risiko secara efektif sambil mempertahankan profitabilitas yang tinggi. Strategi ini memiliki konfigurasi yang kuat, cocok digunakan di berbagai kondisi pasar, namun perlu melalui optimasi parameter dan validasi backtest yang memadai. Ke depannya, stabilitas dan profitabilitas strategi dapat ditingkatkan lebih lanjut dengan menambahkan lebih banyak alat analisis teknis dan metode pengendalian risiko.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Supertrend Strategy with Adjustable Trailing Stop [Bips]", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15)

// Inputs- 1