Sistem Perdagangan Tren Gabungan Persilangan Rata-rata Bergerak Ganda dengan Dukungan dan Resistensi Camarilla

Ikhtisar

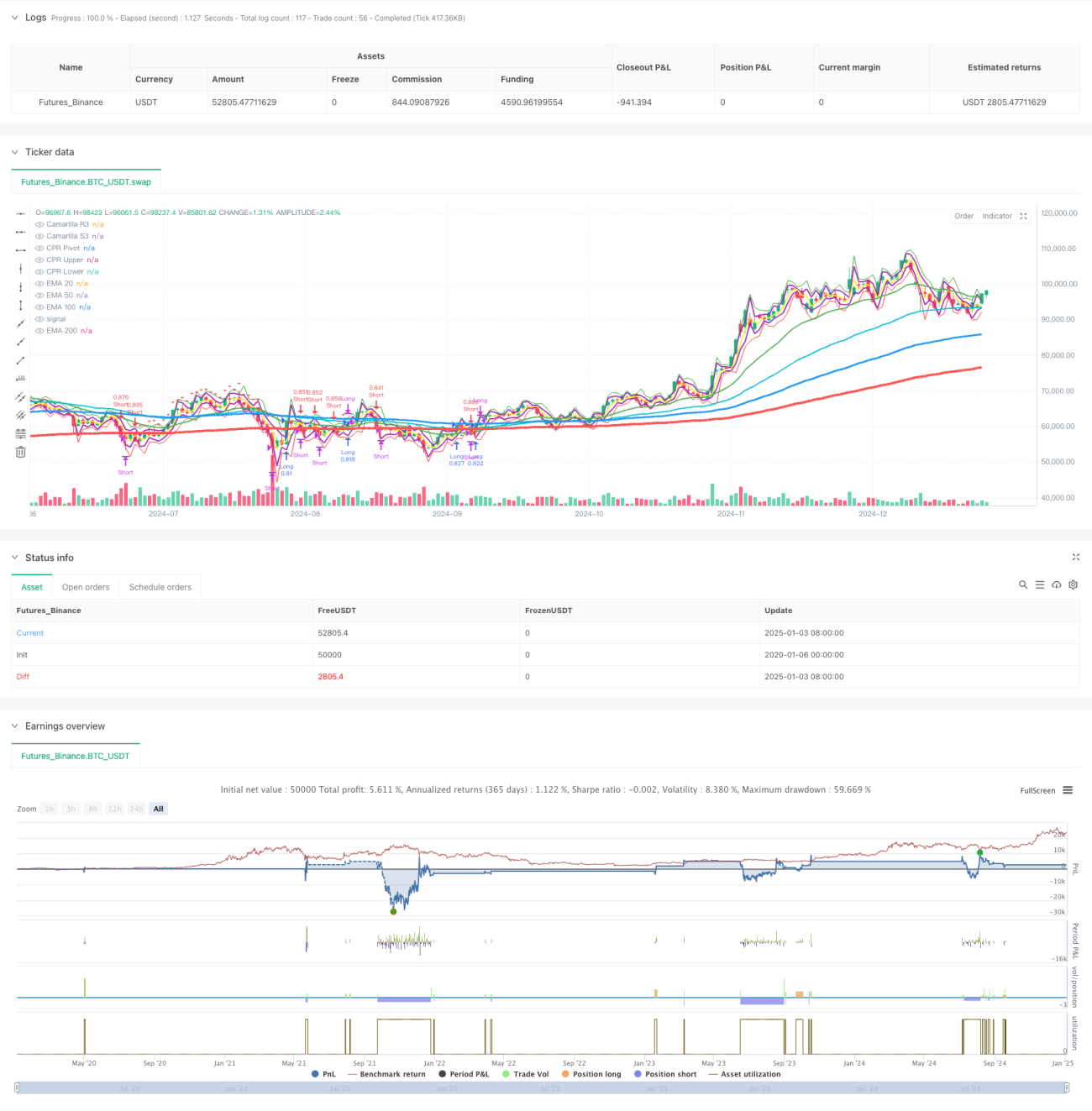

Strategi ini adalah sistem perdagangan yang mengikuti tren yang menggabungkan beberapa rata-rata pergerakan eksponensial (EMA), level support dan resistensi Camarilla, dan Rentang Pivot (CPR). Strategi ini mengidentifikasi tren pasar dan peluang perdagangan potensial dengan menganalisis hubungan harga dengan beberapa rata-rata pergerakan serta rentang harga penting. Sistem ini menerapkan manajemen modal dan langkah-langkah pengendalian risiko yang ketat, termasuk ukuran posisi persentase dan mekanisme keluar yang beragam.

Prinsip Strategi

Strategi ini terutama didasarkan pada beberapa komponen inti berikut:

- Sistem multi-rata-rata bergerak (EMA20/50/100/200) digunakan untuk mengonfirmasi arah dan kekuatan tren

- Level support dan resistensi Camarilla (R3/S3) untuk mengidentifikasi level harga kunci

- Rentang Pivot (CPR) untuk menentukan rentang perdagangan intraday

- Sinyal masuk didasarkan pada persilangan harga dengan EMA200 dan konfirmasi EMA20

- Strategi keluar mencakup dua mode: pergerakan poin tetap dan persentase

- Sistem manajemen modal menyesuaikan ukuran posisi secara dinamis berdasarkan ukuran akun

Keunggulan Strategi

- Kombinasi indikator teknis multi-dimensi memberikan sinyal perdagangan yang lebih andal

- Mekanisme keluar yang fleksibel beradaptasi dengan berbagai kondisi pasar

- Sistem manajemen modal yang lengkap mengendalikan risiko secara efektif

- Karakteristik mengikuti tren membantu menangkap pergerakan besar

- Komponen visual memudahkan pedagang memahami struktur pasar

Risiko Strategi

- Dapat menghasilkan sinyal palsu di pasar yang bergejolak (sideways)

- Banyak indikator dapat menyebabkan keterlambatan sinyal perdagangan

- Titik keluar tetap mungkin berkinerja buruk di pasar dengan volatilitas tinggi

- Membutuhkan modal yang relatif besar untuk menahan drawdown

- Biaya perdagangan dapat mempengaruhi profitabilitas strategi secara keseluruhan

Arah Optimasi Strategi

- Memperkenalkan indikator volatilitas untuk menyesuaikan parameter masuk/keluar secara dinamis

- Menambahkan modul identifikasi kondisi pasar untuk beradaptasi dengan berbagai lingkungan pasar

- Mengoptimalkan sistem manajemen modal dengan menambahkan manajemen posisi dinamis

- Menambahkan filter waktu perdagangan untuk meningkatkan kualitas sinyal

- Mempertimbangkan untuk menambahkan analisis volume guna meningkatkan keandalan sinyal

Kesimpulan

Strategi ini membangun sistem perdagangan yang lengkap dengan mengintegrasikan beberapa alat analisis teknis klasik. Keunggulan sistem ini terletak pada analisis pasar multi-dimensi dan manajemen risiko yang ketat, namun juga perlu memperhatikan kemampuan beradaptasi terhadap berbagai kondisi pasar yang berbeda. Melalui optimasi dan perbaikan berkelanjutan, strategi ini diharapkan dapat meningkatkan profitabilitas sambil tetap mempertahankan stabilitas.

- 1