Strategi Kuantitatif Persilangan Rata-rata Bergerak SMA Tren Jangka Panjang

Ringkasan

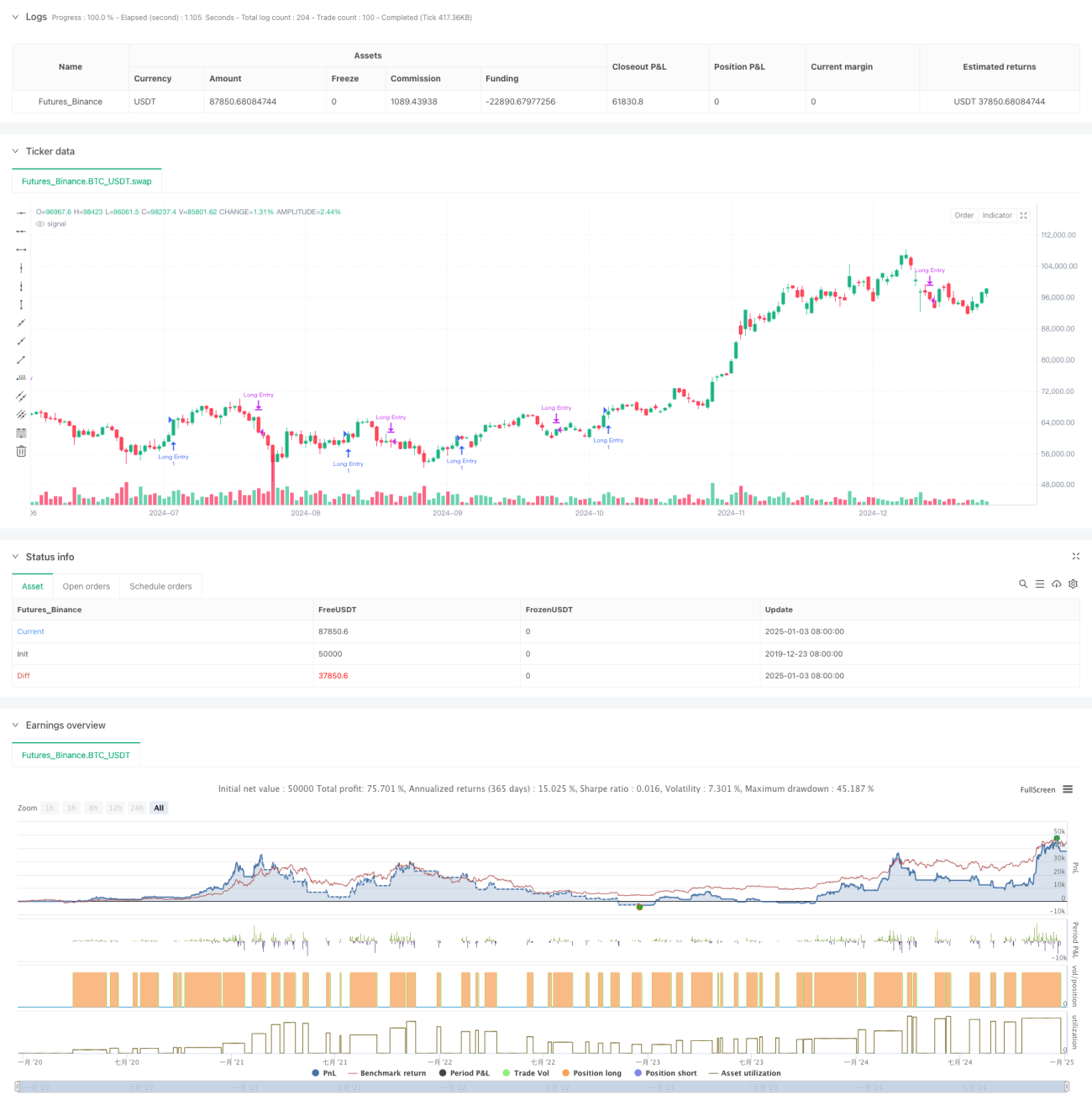

Strategi ini adalah sistem trading kuantitatif berdasarkan sinyal persilangan Simple Moving Average (SMA) multi-periode. Fokus utamanya adalah menangkap peluang koreksi jangka pendek dalam tren naik jangka panjang. Strategi ini menggunakan indikator SMA lima periode: 5, 10, 20, 60, dan 120 hari, serta menilai tren pasar dan waktu trading berdasarkan posisi relatif garis rata-rata dan sinyal persilangan.

Prinsip Strategi

Logika inti strategi terdiri dari beberapa bagian kunci:

- Menilai tren jangka panjang melalui posisi relatif SMA20 dan SMA60. Ketika SMA20 berada di atas SMA60, pasar dikonfirmasi dalam tren naik.

- Dalam kondisi tren naik jangka panjang yang terkonfirmasi, ketika SMA5 jangka pendek naik kembali dari bawah SMA20 ke atas, sinyal beli dipicu. Ini menunjukkan pasar telah memantul setelah koreksi jangka pendek dalam tren naik.

- Ketika SMA20 memotong ke atas SMA5, sinyal tutup posisi dipicu. Ini menunjukkan momentum kenaikan jangka pendek melemah, berpotensi memasuki masa penyesuaian.

- Strategi ini juga menyertakan fungsi filter waktu, yang memungkinkan pembatasan rentang waktu backtest, meningkatkan fleksibilitas strategi.

Keunggulan Strategi

- Logika strategi jelas dan sederhana, mudah dipahami dan diimplementasikan, tanpa melibatkan perhitungan yang rumit.

- Dengan penggunaan kombinasi rata-rata bergerak multi-periode, strategi efektif menyaring kebisingan pasar, meningkatkan keandalan sinyal trading.

- Strategi berfokus pada peluang koreksi dalam pasar tren, sesuai dengan konsep inti "trading tren".

- Menggunakan SMA sebagai pengganti EMA, mengurangi sensitivitas terhadap perubahan harga dan menekan sinyal palsu.

- Logika masuk dan keluar yang jelas, memudahkan eksekusi dan pengendalian risiko.

Risiko Strategi

- Sistem rata-rata bergerak memiliki keterlambatan, yang dapat menyebabkan waktu masuk dan keluar yang kurang optimal.

- Di pasar yang bergejolak (sideways), persilangan rata-rata bergerak yang sering dapat menghasilkan terlalu banyak sinyal palsu.

- Strategi tidak memiliki mekanisme filter volatilitas, sehingga berpotensi menghadapi risiko drawdown besar selama periode volatilitas tinggi.

- Tidak mempertimbangkan indikator teknis lain seperti volume perdagangan, sehingga keandalan sinyal masih perlu ditingkatkan.

- Parameter rata-rata bergerak tetap mungkin tidak cocok untuk semua kondisi pasar.

Arah Optimasi Strategi

- Memperkenalkan indikator ATR untuk menyaring volatilitas, menghindari trading saat volatilitas terlalu tinggi.

- Menambahkan mekanisme konfirmasi volume untuk meningkatkan keandalan sinyal trading.

- Mengembangkan mekanisme periode rata-rata bergerak adaptif, sehingga strategi lebih mampu beradaptasi dengan berbagai kondisi pasar.

- Menambahkan filter kekuatan tren, seperti indikator ADX, untuk memastikan trading dalam tren yang kuat.

- Menyempurnakan mekanisme stop-loss, misalnya dengan menambahkan trailing stop, untuk mengendalikan risiko dengan lebih baik.

Kesimpulan

Strategi ini membangun sistem trading yang berfokus pada penangkapan peluang koreksi dalam tren naik jangka panjang melalui penggunaan kombinasi SMA multi-periode. Desain strategi sederhana dan praktis, memiliki pemahaman dan eksekusi yang baik. Dengan memperkenalkan langkah-langkah optimasi seperti filter volatilitas dan konfirmasi volume, ketahanan dan keandalan strategi diharapkan dapat ditingkatkan lebih lanjut.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Long-Term Growing Stock Strategy", overlay=true)

// Date Range

// STEP 1. Create inputs that configure the backtest's date range- 1