Sistem Trading Trend Following dengan Trailing Stop Loss Dinamis ATR

Ikhtisar

Strategi ini adalah sistem pengikut tren yang menggunakan trailing stop dinamis berdasarkan ATR (Average True Range). Ini menggabungkan EMA sebagai filter tren, dan mengontrol pembentukan sinyal dengan menyesuaikan parameter sensitivitas dan periode ATR. Sistem ini tidak hanya mendukung posisi long, tetapi juga posisi short, dan memiliki mekanisme manajemen keuntungan yang lengkap.

Prinsip Strategi

- Menggunakan indikator ATR untuk menghitung volatilitas harga, dan menentukan jarak trailing stop berdasarkan koefisien sensitivitas (Key Value) yang ditetapkan.

- Menentukan arah tren pasar melalui EMA, hanya membuka posisi long saat harga di atas EMA, dan posisi short saat harga di bawah EMA.

- Ketika harga menembus garis trailing stop dan sesuai dengan arah tren, sinyal trading dipicu.

- Sistem menggunakan manajemen posisi dengan pengambilan keuntungan bertahap:

- Saat keuntungan 20%-50%, tingkatkan stop loss ke harga pokok untuk melindungi modal.

- Saat keuntungan 50%-80%, ambil sebagian keuntungan dan perketat stop loss.

- Saat keuntungan 80%-100%, perketat lebih lanjut stop loss untuk melindungi laba.

- Saat keuntungan lebih dari 100%, tutup semua posisi untuk mengambil laba.

Keunggulan Strategi

- Trailing stop dinamis dapat melacak tren secara efektif, melindungi laba tanpa keluar terlalu dini.

- Filter tren EMA secara efektif mengurangi risiko dari false breakout.

- Mekanisme pengambilan keuntungan bertahap memastikan realisasi keuntungan sekaligus memberi ruang bagi tren untuk berkembang.

- Mendukung trading dua arah (long dan short), memungkinkan memanfaatkan peluang pasar secara optimal.

- Parameter yang dapat disesuaikan dengan baik, cocok untuk berbagai kondisi pasar.

Risiko Strategi

- Di pasar yang sideways, dapat terjadi trading yang sering dan menyebabkan kerugian.

- Pada awal pembalikan tren, dapat terjadi drawdown yang besar.

- Pengaturan parameter yang tidak tepat dapat mempengaruhi kinerja strategi.

Saran pengendalian risiko:

- Disarankan digunakan di pasar dengan tren yang jelas.

- Pilih parameter dengan hati-hati, dapat dioptimalkan melalui backtesting.

- Tetapkan batas drawdown maksimum.

- Pertimbangkan untuk menambahkan filter kondisi pasar.

Arah Optimasi Strategi

- Menambahkan mekanisme identifikasi kondisi pasar, menggunakan parameter berbeda dalam kondisi pasar yang berbeda.

- Memperkenalkan indikator pendukung seperti volume untuk meningkatkan keandalan sinyal.

- Mengoptimalkan mekanisme manajemen keuntungan, menyesuaikan target keuntungan secara dinamis berdasarkan volatilitas.

- Menambahkan filter waktu untuk menghindari trading pada periode yang tidak menguntungkan.

- Pertimbangkan untuk menambahkan filter volatilitas, mengurangi frekuensi trading saat volatilitas berlebihan.

Kesimpulan

Ini adalah sistem pengikut tren yang terstruktur dengan baik dan logis. Dengan menggabungkan trailing stop dinamis ATR dan filter tren EMA, sistem ini berhasil mengendalikan risiko sambil mengikuti tren. Desain mekanisme pengambilan keuntungan bertahap juga mencerminkan pemikiran trading yang matang. Strategi ini memiliki kepraktisan dan skalabilitas yang kuat, dan melalui optimalisasi serta penyempurnaan berkelanjutan, diharapkan dapat mencapai hasil trading yang lebih baik.

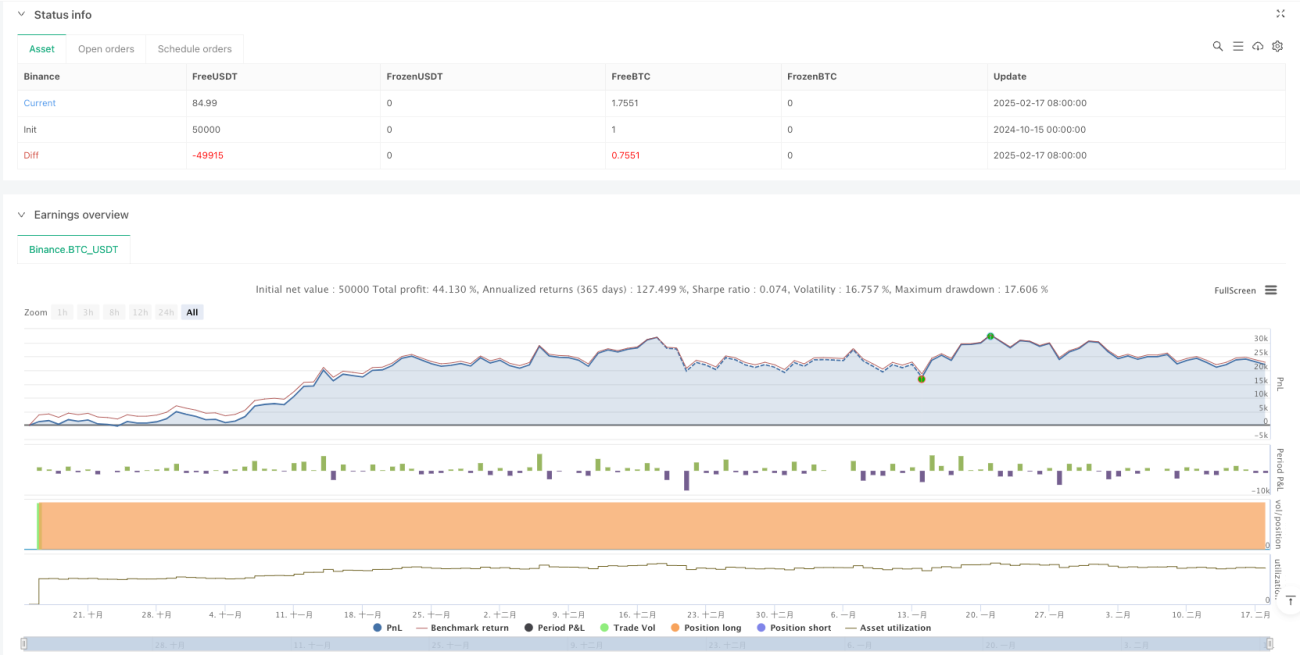

/*backtest

start: 2024-10-15 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Enhanced UT Bot with Long & Short Trades", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input Parameters- 1