Strategi Perdagangan Terintegrasi Multi-Dimensi Berbasis Nadaraya-Watson

Gambaran Umum

Strategi ini adalah sistem perdagangan multidimensi yang didasarkan pada regresi kernel Nadaraya-Watson. Dengan mengintegrasikan informasi pasar dari empat dimensi: teknis, sentimen, volatilitas, dan intensi, strategi ini membentuk sinyal komprehensif untuk memandu keputusan perdagangan. Strategi ini menggunakan metode optimasi bobot untuk membobot sinyal dari berbagai dimensi, dan menggabungkan filter tren dan momentum untuk meningkatkan kualitas sinyal. Sistem ini juga mencakup modul manajemen risiko yang lengkap, melindungi modal melalui stop loss dan take profit.

Prinsip Strategi

Inti dari strategi ini adalah menghaluskan data pasar dari berbagai dimensi menggunakan metode regresi kernel Nadaraya-Watson. Secara rinci:

- Dimensi teknis menggunakan harga penutupan

- Dimensi sentimen menggunakan indikator RSI

- Dimensi volatilitas menggunakan volatilitas ATR

- Dimensi intensi menggunakan deviasi harga dari rata-rata bergerak

Setelah dimensi-dimensi ini dihaluskan dengan regresi kernel, mereka diintegrasikan dengan bobot yang telah ditentukan (teknis 0.4, sentimen 0.2, volatilitas 0.2, intensi 0.2) untuk membentuk sinyal perdagangan akhir. Ketika sinyal terintegrasi bersilangan dengan rata-rata bergeraknya, dikombinasikan dengan filter tren dan momentum untuk konfirmasi, kemudian perintah perdagangan dikeluarkan.

Kelebihan Strategi

- Analisis multidimensi memberikan perspektif pasar yang lebih komprehensif, menghindari keterbatasan indikator tunggal.

- Regresi kernel Nadaraya-Watson secara efektif mengurangi noise pasar, memberikan sinyal yang lebih halus.

- Mekanisme optimasi bobot memungkinkan penyesuaian kepentingan setiap dimensi sesuai dengan karakteristik pasar.

- Penambahan filter tren dan momentum secara signifikan meningkatkan kualitas sinyal.

- Sistem manajemen risiko yang lengkap memastikan keamanan modal.

Risiko Strategi

- Optimasi parameter yang berlebihan dapat menyebabkan overfitting.

- Banyaknya kondisi filter dapat menyebabkan hilangnya beberapa sinyal yang valid.

- Kompleksitas perhitungan regresi kernel yang tinggi dapat memengaruhi kinerja real-time.

- Alokasi bobot yang tidak tepat dapat melemahkan beberapa sinyal pasar yang penting.

Tindakan mitigasi termasuk: menggunakan pengujian di luar sampel untuk memvalidasi parameter, menyesuaikan kondisi filter secara dinamis, mengoptimalkan efisiensi komputasi, serta mengevaluasi dan menyesuaikan alokasi bobot secara berkala.

Arah Optimalisasi Strategi

- Memperkenalkan sistem bobot adaptif untuk menyesuaikan bobot setiap dimensi secara dinamis berdasarkan kondisi pasar.

- Mengembangkan mekanisme filter yang lebih cerdas untuk menyeimbangkan kualitas dan kuantitas sinyal.

- Mengoptimalkan implementasi algoritma Nadaraya-Watson untuk meningkatkan efisiensi komputasi.

- Menambahkan modul identifikasi siklus pasar, menggunakan pengaturan parameter yang berbeda pada fase pasar yang berbeda.

- Memperluas sistem manajemen risiko dengan menambahkan stop loss dinamis dan fungsi manajemen posisi.

Kesimpulan

Ini adalah strategi inovatif yang menggabungkan metode matematika dengan kebijaksanaan perdagangan. Melalui analisis multidimensi dan alat matematika canggih, strategi ini mampu menangkap berbagai aspek pasar, memberikan sinyal perdagangan yang relatif andal. Meskipun masih ada ruang untuk optimalisasi, kerangka strategi secara keseluruhan kokoh dan memiliki nilai aplikasi praktis.

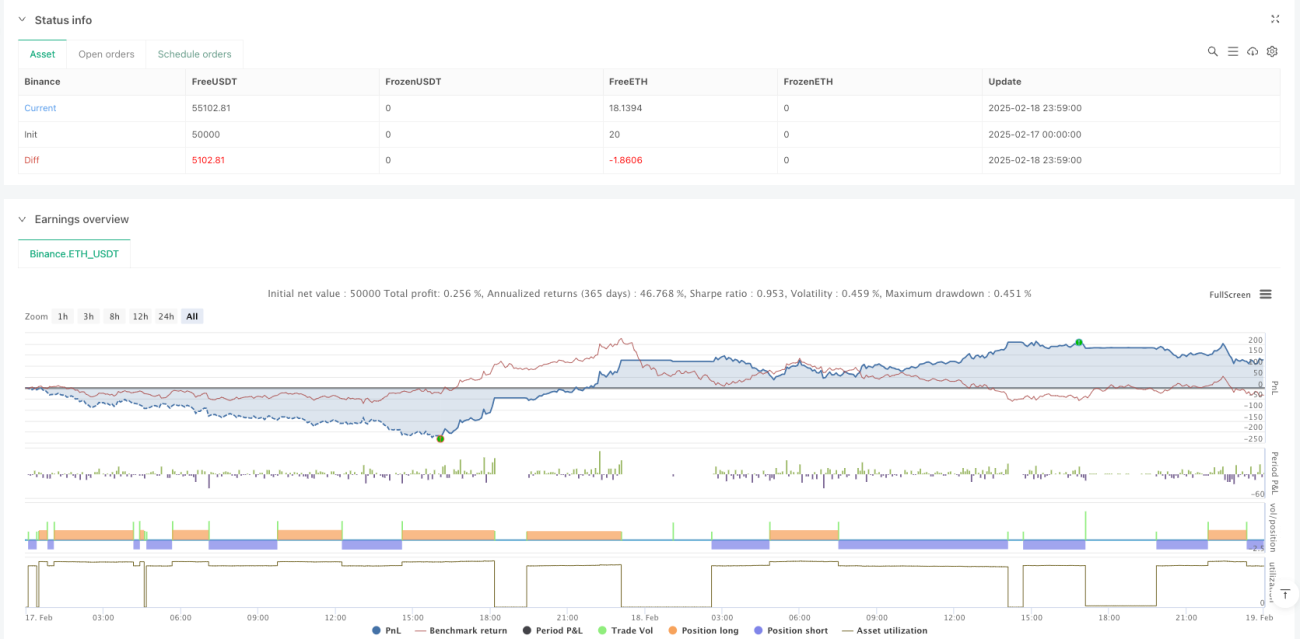

/*backtest

start: 2025-02-17 00:00:00

end: 2025-02-19 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Enhanced Multidimensional Integration Strategy with Nadaraya", overlay=true, initial_capital=10000, currency=currency.USD, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

//────────────────────────────────────────────────────────────────────────────- 1