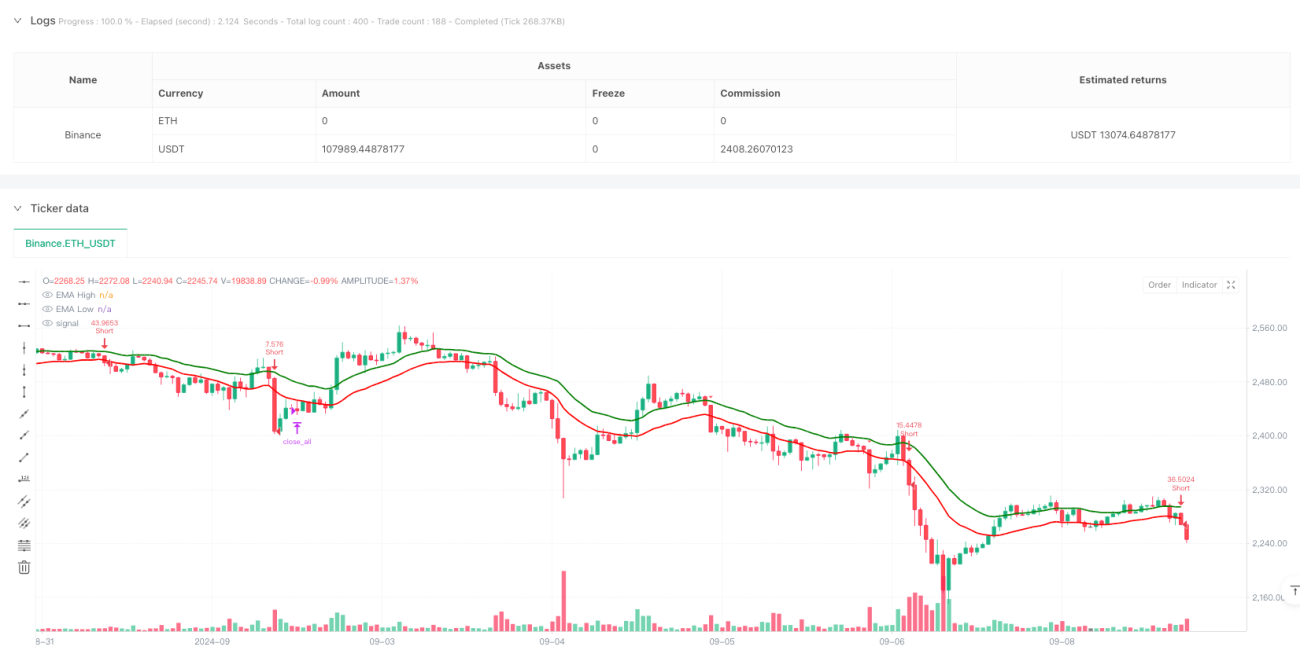

Gambaran Umum

Ini adalah strategi trading intraday berdasarkan beberapa indikator teknikal, yang terutama memanfaatkan sinyal ganda seperti saluran EMA, RSI overbought/oversold, dan konfirmasi tren MACD. Strategi ini berjalan pada timeframe 3 menit, menangkap tren pasar melalui breakout saluran EMA tinggi-rendah yang dikombinasikan dengan konfirmasi cross RSI dan MACD, serta dilengkapi dengan stop loss dan take profit dinamis berbasis ATR, beserta waktu tutup posisi tetap.

Prinsip Strategi

Strategi ini menggunakan EMA periode 20 yang dihitung dari harga tertinggi dan terendah untuk membentuk saluran. Entry dilakukan ketika harga menembus saluran dan memenuhi kondisi berikut:

- Entry Long: Harga penutupan menembus ke atas garis atas EMA, RSI antara 50-70, garis MACD memotong ke atas garis sinyal.

- Entry Short: Harga penutupan menembus ke bawah garis bawah EMA, RSI antara 30-50, garis MACD memotong ke bawah garis sinyal.

- Menggunakan ATR untuk menghitung posisi stop loss secara dinamis, dengan take profit berdasarkan rasio risk-reward 2,5 kali.

- Risiko per transaksi sebesar 1% dari akun, ukuran posisi dihitung secara dinamis berdasarkan jarak stop loss.

- Semua posisi ditutup paksa pada pukul 15:00 Waktu Standar India.

Keunggulan Strategi

- Validasi silang beberapa indikator teknikal meningkatkan keandalan sinyal trading.

- Stop loss dinamis berdasarkan ATR lebih sesuai dengan volatilitas pasar.

- Rasio risiko tetap dan rasio risk-reward yang jelas, mengontrol risiko secara efektif.

- Memperhitungkan biaya transaksi, termasuk kalkulasi komisi.

- Melarang penambahan posisi searah, menghindari risiko over-posisi.

- Waktu tutup tetap, menghindari risiko overnight.

Risiko Strategi

- Beberapa indikator dapat menyebabkan keterlambatan sinyal, mempengaruhi waktu entry.

- Saluran EMA dapat menghasilkan false breakout yang sering di pasar sideways.

- Rasio risk-reward tetap mungkin kurang fleksibel di berbagai kondisi pasar.

- Batasan rentang RSI dapat melewatkan beberapa tren besar.

- Penutupan paksa pada jam tertentu dapat memaksa keluar di posisi kritis.

Arah Optimasi Strategi

- Pertimbangkan menambahkan indikator volume sebagai konfirmasi tambahan.

- Sesuaikan rasio risk-reward secara dinamis berdasarkan karakteristik volatilitas pada sesi yang berbeda.

- Masukkan indikator volatilitas pasar untuk menyesuaikan ambang RSI secara dinamis.

- Pertimbangkan menambahkan filter kekuatan tren untuk mengurangi false breakout.

- Dapat mempertimbangkan penyesuaian parameter berdasarkan karakteristik sesi intraday yang berbeda.

- Tambahkan analisis volatilitas historis untuk mengoptimalkan manajemen posisi.

Kesimpulan

Strategi ini membangun sistem trading yang relatif lengkap melalui kombinasi beberapa indikator teknikal. Keunggulan strategi terletak pada kontrol risiko yang cukup baik, termasuk mekanisme stop loss dinamis, risiko tetap, dan penutupan posisi pada akhir sesi. Meskipun ada risiko keterlambatan tertentu, kinerja strategi dapat ditingkatkan lebih lanjut melalui optimasi parameter dan penambahan indikator pendukung. Strategi ini sangat cocok untuk pasar trading intraday dengan volatilitas tinggi, untuk memperoleh keuntungan stabil melalui kontrol risiko yang ketat dan konfirmasi sinyal ganda.

- 1