Strategi Pembalikan Tingkat Lanjut Berdasarkan RSI dan Volume dalam Perdagangan Kuantitatif

Ikhtisar

Ini adalah strategi trading reversal berdasarkan indikator RSI dan volume. Strategi ini mengidentifikasi kondisi overbought dan oversold di pasar, dikombinasikan dengan konfirmasi volume, untuk melakukan trading kebalikan ketika harga berada dalam kondisi ekstrem. Ide inti strategi ini adalah melakukan trading ketika indikator RSI memberikan sinyal overbought atau oversold, dan volume berada di atas rata-rata, dengan menggunakan garis tengah RSI (50) sebagai sinyal keluar.

Prinsip Strategi

Strategi ini terutama didasarkan pada komponen inti berikut:

- Perhitungan indikator RSI: Menggunakan RSI periode 14 untuk memonitor momentum harga

- Konfirmasi volume: Menggunakan rata-rata bergerak sederhana (SMA) volume periode 20

- Logika masuk:

- Posisi long: Ketika RSI di bawah 30 (oversold) dan volume lebih besar dari rata-rata bergeraknya

- Posisi short: Ketika RSI di atas 70 (overbought) dan volume lebih besar dari rata-rata bergeraknya

- Logika keluar:

- Keluar long: RSI menembus ke atas 50

- Keluar short: RSI menembus ke bawah 50

Keunggulan Strategi

- Keputusan trading yang sistematis: Membangun sistem trading yang objektif melalui kombinasi indikator teknis yang jelas

- Mekanisme konfirmasi ganda: Menggabungkan dua dimensi RSI dan volume untuk meningkatkan keandalan sinyal

- Manajemen risiko yang baik: Menggunakan manajemen modal persentase dan melarang pembukaan posisi berulang

- Dukungan visual: Menyertakan fungsi tampilan grafik lengkap untuk memudahkan analisis dan pemantauan

- Kemampuan adaptasi yang kuat: Parameter utama dapat disesuaikan untuk beradaptasi dengan berbagai kondisi pasar

Risiko Strategi

- Risiko kelanjutan tren: Dalam pasar dengan tren kuat, strategi reversal mungkin sering mengalami kerugian

- Risiko false breakout: Volume tinggi belum tentu menandakan pembalikan pasar yang sebenarnya

- Sensitivitas parameter: Pemilihan periode RSI dan ambang overbought/oversold sangat mempengaruhi kinerja strategi

- Dampak slippage: Selama periode volatilitas ekstrem, harga eksekusi dapat menyimpang secara signifikan dari yang diharapkan

- Risiko manajemen modal: Posisi dengan persentase tetap mungkin terlalu agresif dalam kondisi pasar tertentu

Arah Optimasi Strategi

- Filter tren: Menambahkan indikator penentu tren untuk menghindari trading reversal selama tren kuat

- Parameter dinamis: Menyesuaikan ambang overbought/oversold RSI secara dinamis berdasarkan volatilitas pasar

- Optimasi keluar: Menambahkan mekanisme stop loss dan trailing stop untuk meningkatkan kemampuan manajemen risiko

- Peningkatan analisis volume: Menambahkan analisis pola volume untuk meningkatkan kualitas sinyal

- Filter waktu: Menambahkan jendela waktu trading untuk menghindari sesi trading yang tidak efisien

Kesimpulan

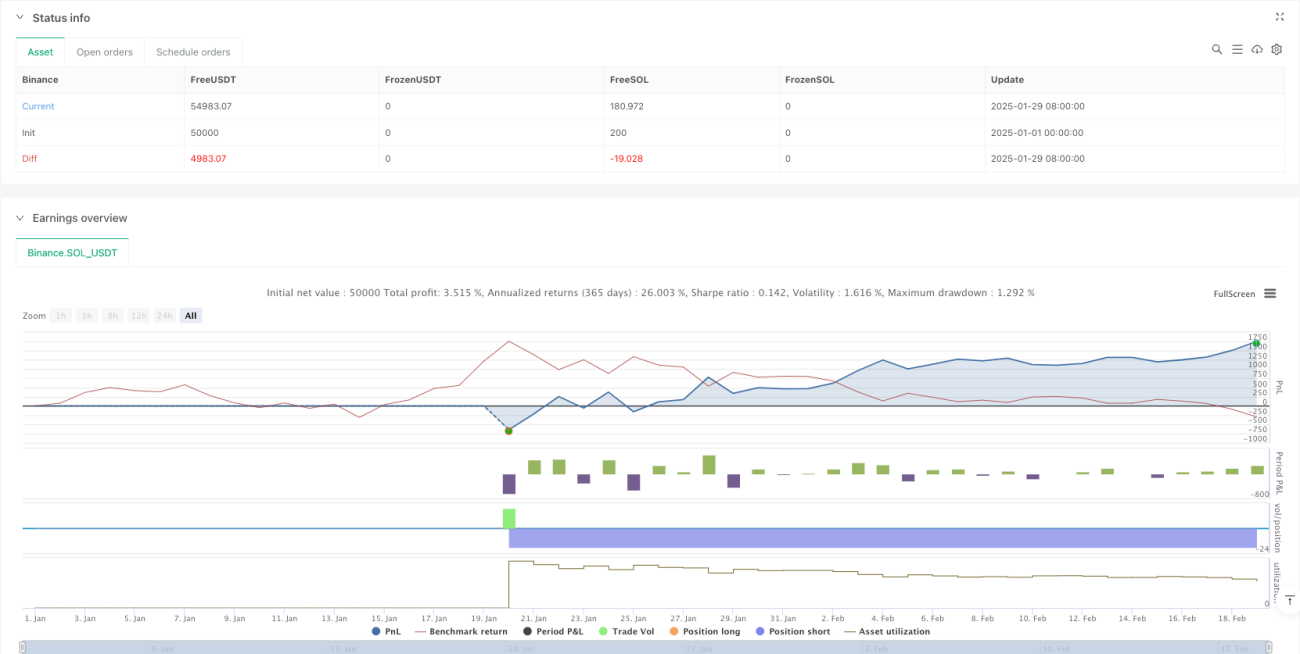

Strategi ini membangun sistem trading reversal yang lengkap dengan menggabungkan indikator RSI dan analisis volume. Strategi ini dirancang dengan baik, memiliki operabilitas dan fleksibilitas yang baik. Melalui arah optimasi yang disarankan, strategi ini masih memiliki ruang untuk peningkatan lebih lanjut. Saat diterapkan pada trading live, disarankan untuk menguji parameter secara menyeluruh dan melakukan optimasi yang ditargetkan sesuai dengan karakteristik pasar.

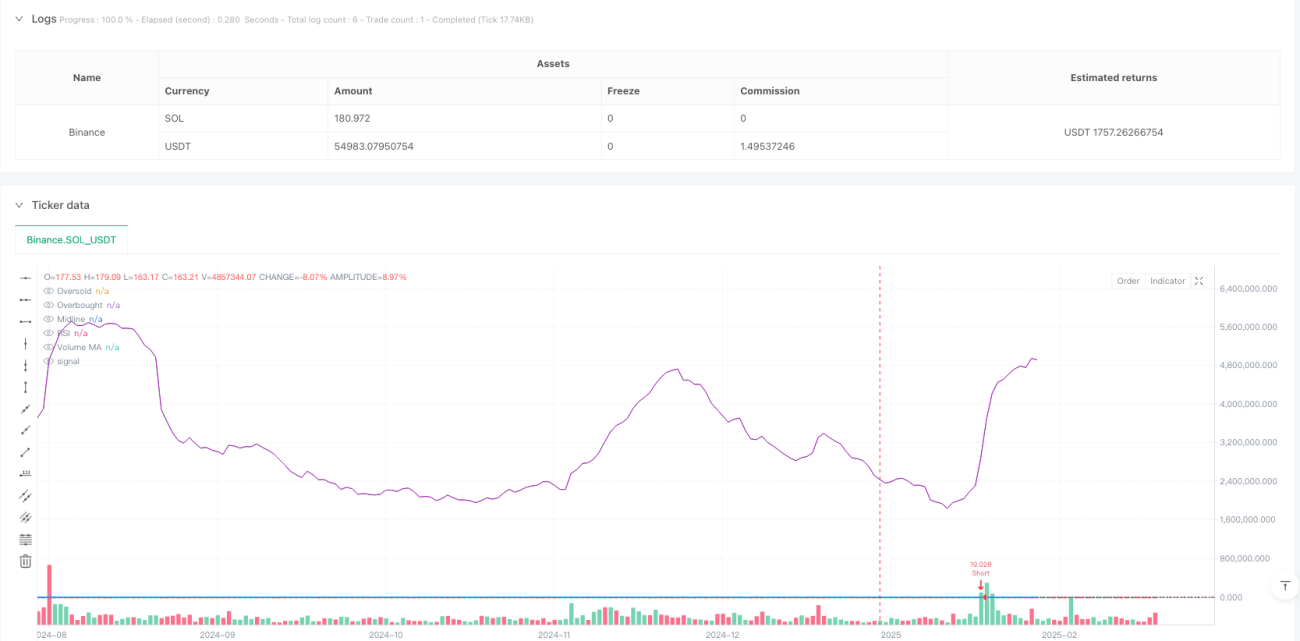

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-19 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("RSI & Volume Contrarian Strategy", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10, pyramiding=0)

//---------------------------- 1