Strategi Terobosan Tren dengan Penggabungan Indikator Teknis Multidimensi

Ikhtisar

Strategi ini adalah sistem trading breakout tren yang menggabungkan beberapa indikator teknis dan pola grafik. Dengan mengidentifikasi formasi grafik kunci (seperti double top/double bottom, head and shoulders top/bottom) dan breakout harga, strategi ini menangkap titik balik tren pasar, sekaligus menggabungkan indikator teknis seperti EMA, ATR, dan volume untuk penyaringan sinyal dan manajemen risiko, sehingga mencapai pelacakan tren dan pengendalian risiko yang efisien.

Prinsip Strategi

Logika inti strategi terdiri dari tiga bagian utama:

- Identifikasi Pola Grafik: Menggunakan metode jendela geser untuk mengidentifikasi formasi teknis klasik seperti double top/double bottom dan head and shoulders, dengan membandingkan titik tertinggi/terendah dan konfirmasi crossover EMA untuk mendeteksi sinyal pembalikan tren.

- Sistem Konfirmasi Tren: Menggunakan EMA periode 50 sebagai filter tren, dikombinasikan dengan breakout harga untuk mengonfirmasi arah tren, dan memverifikasi validitas sinyal melalui filter volume (volume harus lebih tinggi 120% dari rata-rata volume 20 hari).

- Sistem Manajemen Risiko: Menetapkan stop loss dan take profit secara dinamis berdasarkan ATR periode 14, dengan pengali ATR 1,5x untuk kontrol rasio risiko-imbal hasil yang presisi.

Keunggulan Strategi

- Penggabungan Sinyal Multidimensi: Menggabungkan informasi pasar dari berbagai dimensi – pola grafik, moving average, volatilitas, dan volume – untuk meningkatkan keandalan sinyal.

- Manajemen Risiko Dinamis: Menggunakan ATR untuk menyesuaikan level stop loss dan take profit secara dinamis, sehingga adaptif terhadap berbagai kondisi pasar.

- Tingkat Otomatisasi Tinggi: Sistem secara otomatis mengidentifikasi pola, menghasilkan sinyal trading, dan mengeksekusi order, mengurangi intervensi manual.

- Visualisasi yang Jelas: Melalui penanda grafik dan sistem peringatan, sinyal trading ditampilkan secara intuitif.

Risiko Strategi

- Risiko False Breakout: Di pasar yang bergerak sideways, sinyal breakout palsu dapat muncul; diperlukan konfirmasi volume yang ketat.

- Risiko Lagging: Indikator seperti moving average dan ATR memiliki sifat lagging, sehingga mungkin melewatkan momen entry terbaik.

- Sensitivitas Parameter: Efektivitas strategi sangat dipengaruhi oleh pengaturan parameter; diperlukan optimasi melalui backtest untuk menentukan parameter optimal.

- Ketergantungan pada Lingkungan Pasar: Di pasar sideways tanpa tren yang jelas, kinerja strategi mungkin kurang optimal.

Arah Optimasi Strategi

- Memperkenalkan Identifikasi Lingkungan Pasar: Menambahkan indikator kekuatan tren (misalnya ADX) untuk membedakan pasar tren dan pasar sideways, serta menyesuaikan parameter strategi secara dinamis.

- Mengoptimalkan Penyaringan Sinyal: Dapat mempertimbangkan penambahan indikator osilator seperti RSI untuk menyaring lebih lanjut sinyal breakout palsu.

- Menyempurnakan Kontrol Risiko: Memperkenalkan sistem manajemen posisi yang menyesuaikan ukuran posisi secara dinamis berdasarkan volatilitas pasar.

- Meningkatkan Adaptabilitas: Mengembangkan sistem parameter adaptif yang secara otomatis mengoptimalkan parameter strategi sesuai kondisi pasar.

Kesimpulan

Strategi ini secara efektif menangkap titik balik tren pasar melalui integrasi berbagai indikator teknis multidimensi. Desain sistem secara menyeluruh mempertimbangkan elemen kunci seperti pembangkitan sinyal, konfirmasi tren, dan manajemen risiko, sehingga memiliki kepraktisan yang kuat. Melalui arah optimasi yang disarankan, stabilitas dan adaptabilitas strategi diharapkan dapat ditingkatkan lebih lanjut. Dalam penerapan live trading, disarankan agar trader menyesuaikan parameter strategi sesuai dengan karakteristik pasar spesifik dan toleransi risiko pribadi.

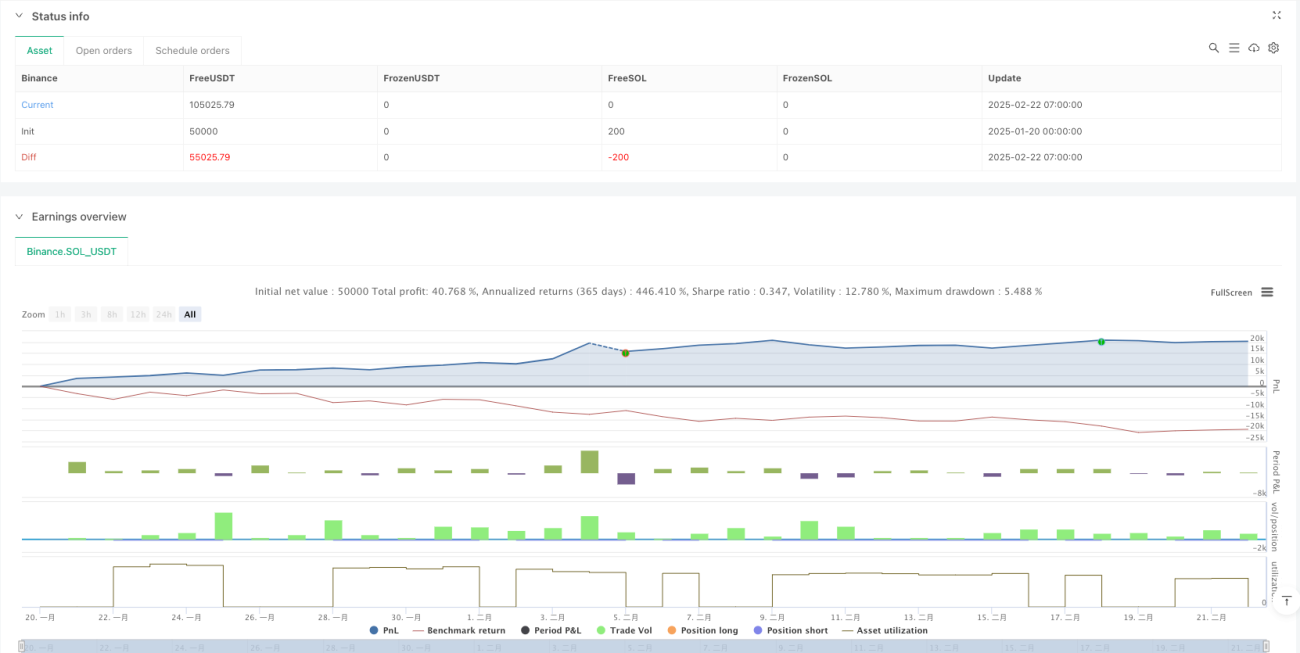

/*backtest

start: 2025-01-20 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Ultimate Pattern Finder", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// 🎯 CONFIGURABLE PARAMETERS- 1