Ikhtisar

Ini adalah strategi trading inovatif yang menggabungkan analisis zona likuiditas dan dinamika struktur pasar internal, bertujuan untuk mengidentifikasi titik masuk dengan probabilitas tinggi. Strategi ini melacak interaksi harga dengan level pasar kunci dan memanfaatkan pergeseran pasar internal untuk memicu trading, memberikan metode masuk pasar yang fleksibel dan presisi bagi para trader.

Prinsip Strategi

Logika inti strategi didasarkan pada dua komponen kunci: identifikasi zona likuiditas dan pergeseran pasar internal. Zona likuiditas ditentukan secara dinamis dengan menganalisis titik tertinggi dan terendah lokal, sementara pergeseran pasar internal menilai perubahan arah pasar berdasarkan penembusan harga di atas level bullish atau bearish sebelumnya.

Strategi ini memiliki fitur inti sebagai berikut:

- Logika pergeseran pasar internal: tidak bergantung pada pola candlestick tradisional, tetapi berdasarkan penembusan harga pada level kunci.

- Pelacakan zona likuiditas: mengidentifikasi zona likuiditas kunci secara dinamis untuk mencegah trading dalam kondisi pasar lemah.

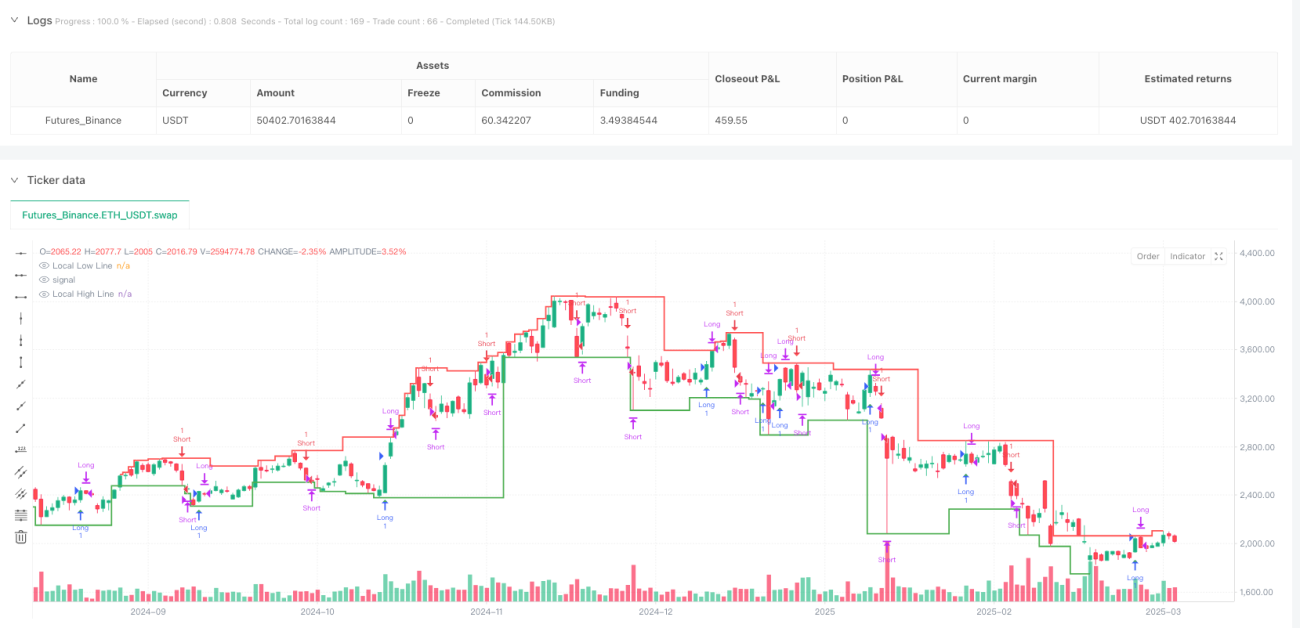

- Fleksibilitas mode: menyediakan tiga mode trading: "Both", "Bullish Only", dan "Bearish Only".

- Manajemen risiko: dapat menyesuaikan level stop loss dan take profit secara kustom.

- Kontrol rentang waktu: dapat mengontrol periode trading secara presisi.

Keunggulan Strategi

- Adaptasi dinamis: strategi dapat merespons perubahan struktur pasar dengan cepat.

- Entri presisi: menggabungkan zona likuiditas dan pergeseran pasar internal untuk meningkatkan akurasi entri.

- Risiko terkendali: dilengkapi mekanisme stop loss dan take profit bawaan.

- Fleksibilitas tinggi: dapat memilih mode trading sesuai dengan kondisi pasar yang berbeda.

- Analisis multidimensi: mempertimbangkan aksi harga, likuiditas, dan struktur pasar secara bersamaan.

Risiko Strategi

- Volatilitas pasar yang ekstrem dapat memicu stop loss.

- Di pasar yang bergerak sideways (ranging), sinyal yang sering muncul dapat meningkatkan biaya trading.

- Pengaturan parameter yang tidak tepat dapat mempengaruhi kinerja strategi.

- Hasil backtest mungkin berbeda dengan perdagangan langsung (real-time).

Arah Optimasi Strategi

- Memperkenalkan algoritma pembelajaran mesin untuk optimasi parameter adaptif.

- Menambahkan lebih banyak filter seperti volume perdagangan, indikator volatilitas.

- Mengembangkan mekanisme verifikasi multi-timeframe.

- Mengoptimalkan algoritma stop loss dan take profit dengan mempertimbangkan penyesuaian dinamis volatilitas pasar.

Kesimpulan

Ini adalah strategi trading inovatif yang menggabungkan analisis likuiditas dan dinamika struktur pasar. Dengan logika pergeseran pasar internal yang fleksibel dan pelacakan zona likuiditas yang presisi, strategi ini menyediakan alat trading yang kuat bagi para trader. Kunci dari strategi ini terletak pada daya adaptasi dan kemampuan analisis multidimensinya, yang memungkinkan efisiensi eksekusi yang tinggi di berbagai kondisi pasar.

- 1