Strategi Trading Futures dengan Stop-Loss Dinamis Berdasarkan Banyak Indikator Teknis

Ringkasan Strategi

Strategi ini adalah sistem trading futures canggih yang menggabungkan beberapa kondisi teknis dan analisis time frame lebih tinggi untuk mengidentifikasi peluang trading dengan probabilitas tinggi. Strategi ini menggunakan pendekatan konfluensi multi-kondisi, di mana beberapa kondisi teknis harus terpenuhi secara bersamaan sebelum masuk ke posisi. Strategi ini mengintegrasikan beberapa konsep teknis modern, termasuk Gap Nilai Wajar (FVG), Blok Pesanan (Order Blocks), Sapuan Likuiditas (Liquidity Sweeps), dan sinyal Break of Structure (BOS), serta memanfaatkan indikator dari berbagai periode waktu untuk mengonfirmasi arah tren.

Prinsip Strategi

Inti dari strategi ini adalah menggunakan kombinasi dari beberapa metode analisis teknis untuk memastikan bahwa posisi hanya diambil ketika beberapa indikator memberikan sinyal secara bersamaan. Secara spesifik, strategi ini terdiri dari beberapa komponen kunci berikut:

- Gap Nilai Wajar (FVG) – Teridentifikasi ketika terdapat celah harga yang signifikan antara dua candle, menunjukkan adanya ruang yang belum terisi di pasar.

- Blok Pesanan – Area kunci di mana harga membentuk pembalikan, biasanya ditandai dengan candle penolakan yang kuat, yang kemudian menjadi level support atau resistance.

- Sapuan Likuiditas – Mengidentifikasi situasi di mana harga menembus level higher high atau lower low sebelumnya lalu segera berbalik, yang biasanya menunjukkan bahwa institusi besar sedang mengumpulkan likuiditas.

- Break of Structure (BOS) – Terjadi ketika harga menembus struktur sebelumnya, membentuk higher high atau lower low baru.

- Konfirmasi Tren Time Frame Lebih Tinggi – Menggunakan EMA (Exponential Moving Average) pada time frame 15 menit dan 60 menit untuk mengonfirmasi arah tren secara keseluruhan.

Strategi hanya akan menghasilkan sinyal masuk jika setidaknya dua kondisi dasar (satu dalam mode debug) ditambah sinyal BOS terpenuhi, dan sejalan dengan tren time frame yang lebih tinggi.

Manajemen risiko: Strategi ini menggunakan ATR (Average True Range) untuk menetapkan level stop loss dinamis, dengan jarak stop loss biasanya 1,5 kali nilai ATR. Metode ini meningkatkan jarak stop loss saat volatilitas tinggi dan menguranginya saat volatilitas rendah, membuat stop loss lebih cerdas.

Untuk take profit, strategi menggunakan pendekatan take profit bertahap: ketika keuntungan mencapai setara dengan risiko (1R), 50% posisi ditutup, sementara sisa posisi dipindahkan ke titik impas, sehingga menciptakan peluang trading tanpa risiko. Selain itu, terdapat mekanisme keluar berdasarkan waktu: jika posisi tidak bergerak ke arah yang menguntungkan dalam waktu yang ditentukan (default 30 menit), posisi akan ditutup secara otomatis.

Strategi ini juga memiliki fitur manajemen akun: ketika akun mencapai target keuntungan yang telah ditetapkan ($3.000) atau memicu trailing stop (dimulai setelah akun memiliki keuntungan lebih dari $2.500), semua posisi akan ditutup secara otomatis.

Keunggulan Strategi

Setelah menganalisis kode secara mendalam, kami dapat menyimpulkan beberapa keunggulan yang jelas:

- Sistem Konfirmasi Ganda – Mensyaratkan beberapa kondisi teknis terpenuhi secara bersamaan sebelum masuk, secara efektif mengurangi sinyal palsu dan meningkatkan kualitas trading.

- Manajemen Risiko Cerdas – Menggunakan stop loss dinamis berbasis ATR, yang lebih adaptif terhadap perubahan volatilitas pasar dibandingkan dengan titik tetap atau persentase tetap.

- Filter Tren Time Frame Lebih Tinggi – Memanfaatkan arah tren dari time frame yang lebih tinggi, hanya trading searah tren, menghindari trading melawan tren.

- Strategi Take Profit Bertahap – Melalui penutupan posisi bertahap dan pemindahan stop loss ke titik impas, mengamankan sebagian keuntungan sambil memberikan peluang tanpa risiko untuk sisa posisi.

- Mekanisme Keluar Berbasis Waktu – Menutup posisi yang tidak efektif secara otomatis, mencegah dana terjebak terlalu lama dalam posisi yang tidak bergerak.

- Manajemen Akun Keseluruhan – Melindungi keuntungan akun secara keseluruhan dengan menetapkan target profit dan trailing stop, mencapai manajemen modal yang solid.

- Adaptabilitas Tinggi – Menawarkan fleksibilitas tinggi melalui berbagai parameter, yang dapat disesuaikan dengan kondisi pasar dan gaya trading yang berbeda.

- Integrasi Indikator Teknis Profesional – Menggabungkan berbagai konsep analisis teknis tingkat lanjut yang biasanya hanya digunakan oleh trader profesional.

Risiko Strategi

Meskipun strategi ini dirancang dengan baik, tetap ada beberapa potensi risiko, termasuk:

- Risiko Overfitting Parameter – Strategi bergantung pada pengaturan banyak parameter; jika dioptimalkan secara berlebihan, dapat menyebabkan overfitting dan kinerja buruk di kondisi pasar masa depan. Solusinya adalah menggunakan periode pengujian yang cukup panjang dan melakukan forward testing.

- Ketergantungan pada Kondisi Pasar – Strategi ini mungkin unggul di pasar yang trending, tetapi dapat menghasilkan lebih banyak sinyal palsu di pasar yang bergerak sideways. Solusinya adalah menambahkan filter kondisi pasar, menyesuaikan frekuensi trading atau berhenti trading sama sekali ketika pasar teridentifikasi sebagai sideway.

- Risiko Slippage Eksekusi – Selama volatilitas tinggi, harga masuk dan keluar mungkin berbeda secara signifikan dari yang diharapkan, memengaruhi kinerja strategi. Solusinya adalah mensimulasikan slippage realistis dalam backtest, dan menggunakan limit order daripada market order dalam trading nyata.

- Risiko Kegagalan Teknis – Sistem trading otomatis dapat menghadapi kegagalan teknis atau gangguan koneksi internet. Solusinya adalah menyiapkan sistem cadangan dan mekanisme intervensi manual.

- Kompleksitas Manajemen – Kompleksitas strategi dapat menyulitkan diagnosis masalah atau pemahaman mengapa trading tertentu gagal. Solusinya adalah menyimpan log trading terperinci dan menganalisis kinerja strategi secara berkala.

- Risiko Likuiditas Pasar – Dalam kondisi pasar tertentu, seperti sebelum dan sesudah rilis berita penting, likuiditas dapat turun dengan cepat, menyebabkan slippage lebih besar atau ketidakmampuan untuk keluar dari posisi. Solusinya adalah menghindari trading selama rilis data ekonomi penting, atau mengurangi ukuran posisi pada periode tersebut.

Arah Optimasi Strategi

Berdasarkan analisis kode, berikut adalah beberapa arah optimasi potensial:

- Meningkatkan Identifikasi Tren – Strategi saat ini menggunakan persilangan EMA sederhana untuk menentukan tren; dapat dipertimbangkan untuk menambahkan indikator tren lain seperti ADX (Average Directional Index) untuk mengonfirmasi kekuatan tren, karena pasar dengan tren kuat biasanya memberikan peluang trading yang lebih baik.

- Adaptasi Kondisi Pasar – Tambahkan mekanisme identifikasi kondisi pasar untuk secara otomatis menyesuaikan parameter strategi di berbagai lingkungan pasar (trending, sideway, volatilitas tinggi, volatilitas rendah). Ini akan membuat strategi lebih fleksibel dan adaptif terhadap kondisi pasar yang berbeda.

- Optimasi Entry Timing – Pertimbangkan untuk menambahkan indikator momentum seperti RSI atau Stochastic untuk memastikan bahwa entry searah tren juga menghindari entry pada kondisi overbought atau oversold yang berlebihan, sehingga mengurangi risiko pembalikan.

- Peningkatan Strategi Take Profit – Target take profit 1R yang tetap saat ini mungkin terlalu konservatif atau agresif; dapat dipertimbangkan untuk menyesuaikan target take profit secara dinamis berdasarkan volatilitas atau level support/resistance, menetapkan target yang lebih jauh saat volatilitas tinggi.

- Manajemen Risiko yang Lebih Halus – Perkenalkan mekanisme penyesuaian ukuran posisi dinamis berdasarkan kinerja strategi baru-baru ini dan volatilitas pasar, meningkatkan risiko saat strategi berkinerja baik dan menguranginya saat berkinerja buruk.

- Tambahkan Filter Waktu Intraday – Pasar futures memiliki karakteristik yang berbeda pada sesi waktu yang berbeda; menambahkan filter waktu dapat menghindari periode dengan likuiditas rendah atau tanpa arah yang jelas.

- Integrasi Indikator Sentimen Pasar – Tambahkan indikator sentimen pasar seperti VIX untuk menyesuaikan parameter strategi atau menghentikan trading saat sentimen ekstrem.

- Optimasi Efisiensi Kode – Kode saat ini memiliki beberapa operasi perulangan yang dapat memengaruhi efisiensi eksekusi, terutama pada time frame yang lebih kecil. Mengoptimalkan perulangan ini dapat meningkatkan kecepatan respons strategi.

Kesimpulan

Ini adalah strategi trading futures multi-indikator yang dirancang dengan baik, menggabungkan berbagai konsep analisis teknis modern, serta dilengkapi dengan manajemen risiko dan modal yang komprehensif. Strategi ini mengurangi sinyal palsu dengan mensyaratkan beberapa kondisi terpenuhi secara bersamaan dan konfirmasi tren dari time frame yang lebih tinggi, sambil menggunakan stop loss dinamis berbasis ATR dan strategi take profit bertahap untuk mengoptimalkan rasio risiko-imbal hasil.

Keunggulan utama strategi ini terletak pada sistem konfirmasi berlapis dan manajemen risiko cerdas, yang memungkinkannya menangkap peluang trading dengan probabilitas tinggi sambil menjaga risiko tetap rendah. Namun, kompleksitas strategi juga membawa tantangan dalam optimasi parameter dan adaptasi pasar, yang memerlukan pemantauan berkelanjutan dan penyesuaian berkala untuk mempertahankan efektivitasnya.

Dengan menerapkan langkah-langkah optimasi yang disarankan, terutama meningkatkan adaptasi kondisi pasar dan menyempurnakan sistem manajemen risiko, strategi ini berpotensi mempertahankan kinerja yang stabil di berbagai lingkungan pasar. Secara keseluruhan, ini adalah strategi canggih yang cocok untuk trader berpengalaman, dan dengan pemantauan serta penyesuaian yang tepat, dapat menjadi alat yang kuat dalam sistem trading.

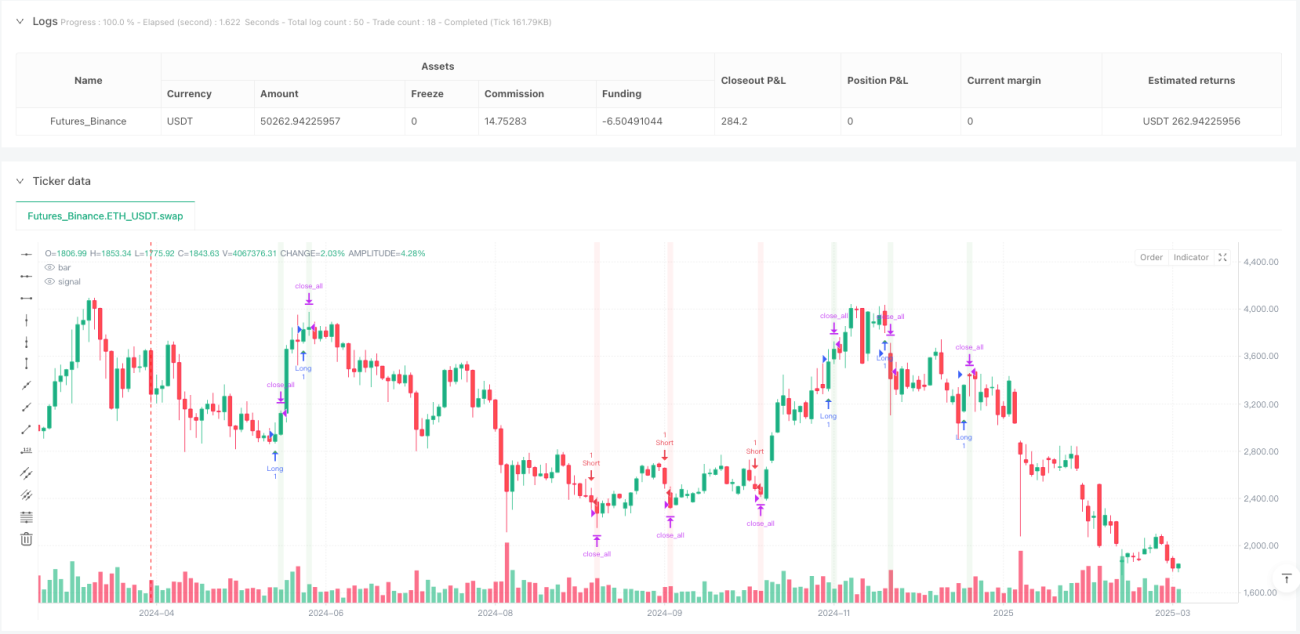

/*backtest

start: 2024-04-02 00:00:00

end: 2025-04-01 00:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

// @version=5

strategy("NQ Futures Trading Strategy", overlay=true, initial_capital=50000, default_qty_type=strategy.cash, default_qty_value=5000)

// ==========================================- 1