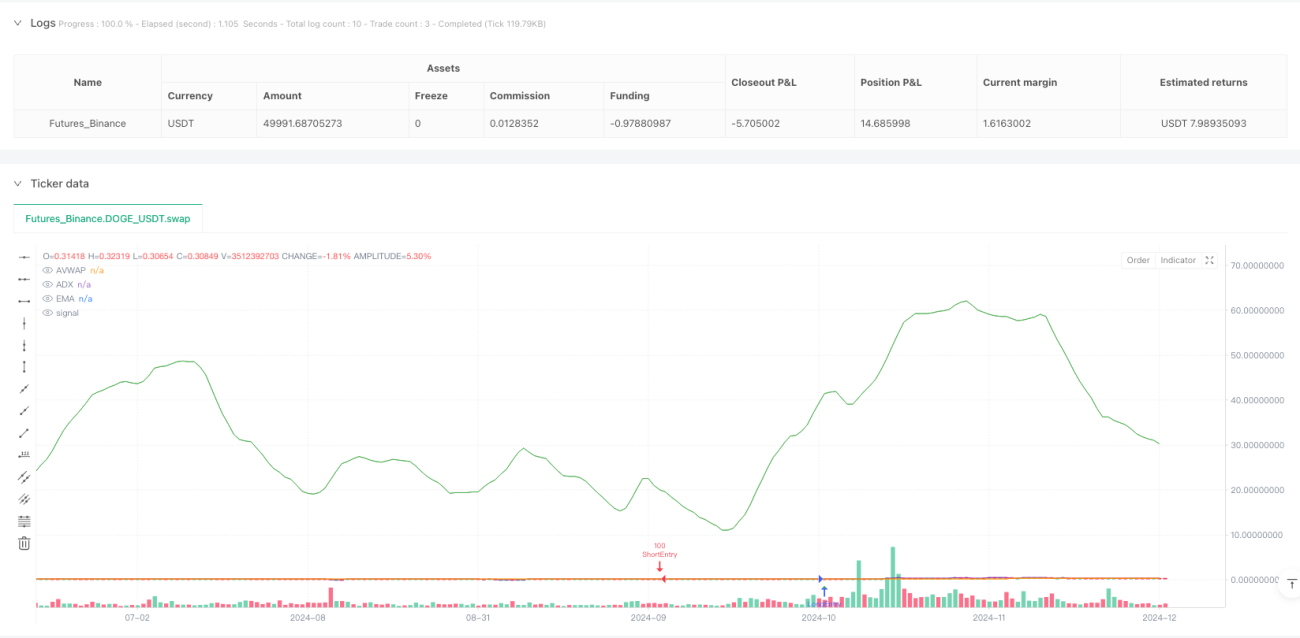

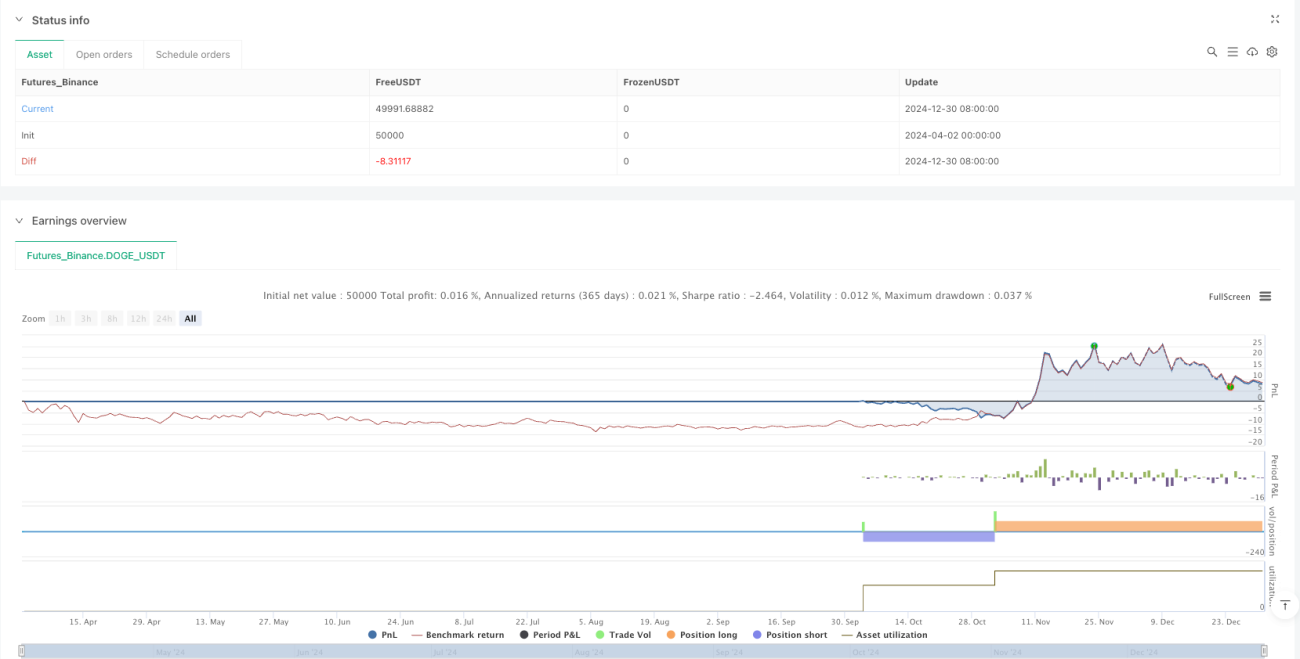

Ringkasan

Ini adalah strategi perdagangan multi-indikator yang kompleks, menggabungkan Volume Weighted Average Price (AVWAP), Fixed Range Volume Profile (FRVP), Exponential Moving Average (EMA), Relative Strength Index (RSI), Average Directional Index (ADX), dan Moving Average Convergence Divergence (MACD) serta alat analisis teknis lainnya, yang bertujuan untuk mengidentifikasi peluang perdagangan dengan probabilitas tinggi melalui agregasi indikator.

Prinsip Strategi

Strategi menentukan sinyal masuk melalui beberapa kondisi:

- Persilangan harga dengan AVWAP

- Posisi harga relatif terhadap EMA

- Penilaian kekuatan RSI

- Momentum tren MACD

- Konfirmasi kekuatan tren ADX

- Filter volume

Strategi berfokus pada sesi perdagangan Asia, London, dan New York, di mana likuiditas biasanya lebih baik dan sinyal perdagangan lebih andal. Logika masuk mencakup mode posisi panjang dan pendek, serta dilengkapi dengan mekanisme take profit dan stop loss bertingkat.

Keunggulan Strategi

- Kombinasi multi-indikator, meningkatkan akurasi sinyal

- Filter volume dinamis, menghindari perdagangan dengan likuiditas rendah

- Strategi take profit dan stop loss yang fleksibel

- Optimasi strategi berdasarkan sesi perdagangan yang berbeda

- Mekanisme manajemen risiko dinamis

- Sinyal visual untuk membantu pengambilan keputusan

Risiko Strategi

- Kombinasi multi-indikator dapat meningkatkan kompleksitas sinyal

- Data backtest mungkin mengandung risiko overfitting

- Kinerja dapat tidak stabil di berbagai kondisi pasar

- Biaya transaksi dan slippage dapat mempengaruhi keuntungan aktual

Arah Optimasi Strategi

- Memperkenalkan algoritma pembelajaran mesin untuk menyesuaikan parameter secara dinamis

- Menambahkan lebih banyak adaptasi sesi perdagangan

- Mengoptimalkan strategi take profit dan stop loss

- Memperkenalkan lebih banyak kondisi filter

- Mengembangkan model strategi universal lintas instrumen

Kesimpulan

Ini adalah strategi perdagangan yang sangat disesuaikan dan multi-dimensi, yang mencoba meningkatkan kualitas dan akurasi sinyal perdagangan dengan mengintegrasikan beberapa indikator teknis dan karakteristik sesi perdagangan. Strategi ini menunjukkan kompleksitas agregasi indikator dan manajemen risiko dinamis dalam perdagangan kuantitatif.

/*backtest

start: 2024-04-02 00:00:00

end: 2024-12-31 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=6

strategy("FRVP + AVWAP by Grok", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// User Inputs- 1