Strategi Terobosan/Pembalikan Tertimbang Volume Berbasis Titik Pivot

Ringkasan

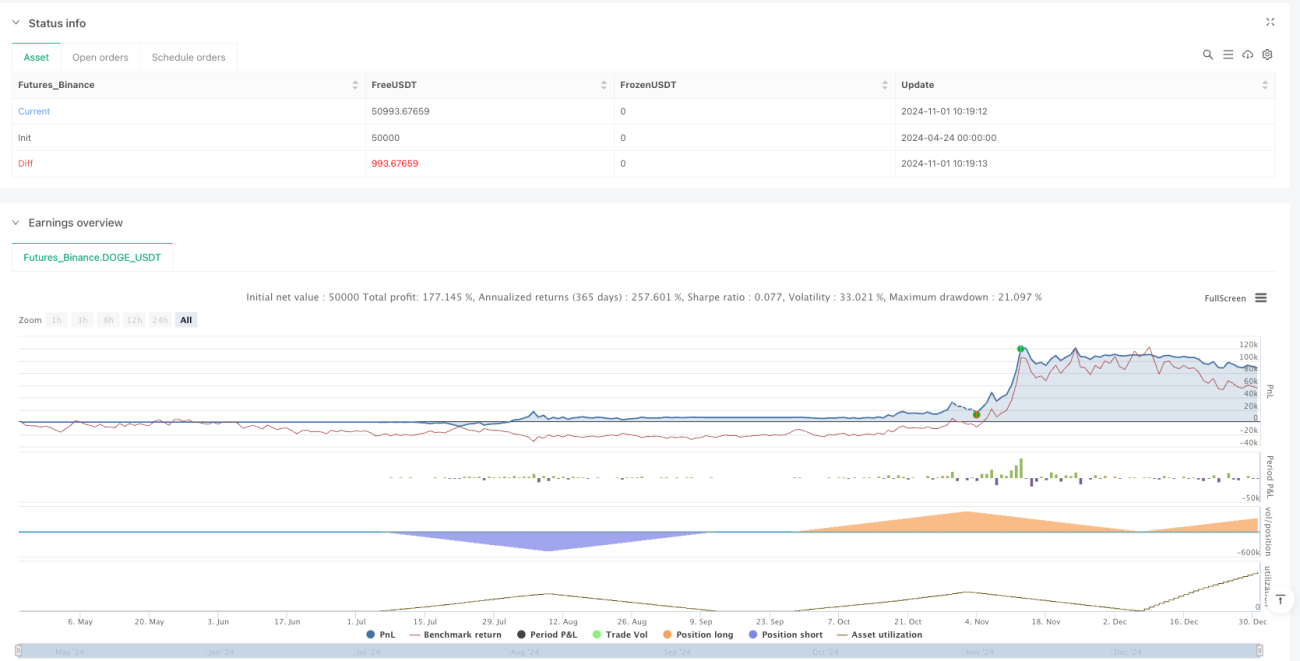

Strategi ini menggabungkan sinyal tembus/pembalikan level Support/Resistance (S/R), filter volume, dan sistem peringatan untuk menangkap titik balik kunci di pasar. Strategi mengidentifikasi sinyal tembus harga atau pembalikan, dikonfirmasi dengan volume abnormal untuk meningkatkan keandalan sinyal trading. Strategi menggunakan stop loss tetap 2% dan rasio take profit yang dapat disesuaikan (default 3%) untuk mengelola risiko.

Prinsip Strategi

- Identifikasi Support/Resistance: Menggunakan fungsi

ta.pivothigh()danta.pivotlow()untuk mengidentifikasi level harga kunci dalam periode tertentu (pivotLen). Sinyal dipicu ketika harga menembus resistance (naik 1%) atau memantul dari support (turun lalu pulih). - Filter Volume: Menghitung SMA volume (periode volSmaLength), ketika volume saat ini melebihi volMultiplier kali SMA (default 1,5x), dianggap konfirmasi valid.

- Logika Long/Short:

- Kondisi Long: Harga menembus zona resistance (close > resZone*1.01) disertai volume tinggi, atau harga mendekati zona support (dalam ±1%) terjadi "false breakdown" (low ≤ supZone tetapi close pulih) dengan volume membesar.

- Kondisi Short: Harga menembus zona support (close < supZone*0.99) disertai volume tinggi, atau harga mendekati zona resistance (dalam ±1%) terjadi "false breakout" (high ≥ resZone tetapi close turun) dengan volume membesar.

- Manajemen Risiko: Stop loss tetap 2% dan take profit yang dapat disesuaikan (default 3%) diimplementasikan melalui

strategy.exit().

Analisis Keunggulan

- Verifikasi Multi-Faktor: Menggabungkan struktur harga (S/R), volume, dan perilaku pasar (false breakout/false breakdown), signifikan mengurangi probabilitas sinyal palsu.

- Adaptasi Dinamis: Level support/resistance diperbarui secara otomatis, menyesuaikan dengan perubahan pasar.

- Kontrol Risiko Ketat: Stop loss tetap mencegah kerugian berlebihan pada satu perdagangan, rasio take profit dapat disesuaikan untuk pasar dengan volatilitas berbeda.

- Visualisasi Kuat: Garis support/resistance digambar real-time, sinyal trading ditandai dengan jelas.

- Integrasi Peringatan: Dapat dihubungkan dengan sistem trading otomatis, cocok untuk berbagai skenario trading.

Analisis Risiko

- Risiko Pasar Ranging: Sinyal false breakout sering terjadi di pasar tanpa tren, menyebabkan beberapa kali stop loss. Solusi: Tambahkan filter tren seperti ADX atau EMA.

- Sensitivitas Parameter: pivotLen dan volMultiplier perlu disesuaikan dengan pasar. Solusi: Lakukan optimasi parameter dan uji Walk-Forward.

- Keterlambatan Volume: Volume abnormal mungkin muncul setelah pergerakan harga. Solusi: Gabungkan data order book atau perpendek volSmaLength.

- Risiko Gap: Gap bukaan dapat melompati level stop loss. Solusi: Gunakan limit order atau hindari sesi volatilitas tinggi.

Arah Optimasi

- Filter Tren: Tambahkan kondisi ADX>25 atau arah 200EMA untuk menghindari trading melawan tren.

- Parameter Dinamis: Sesuaikan pivotLen dan volMultiplier secara otomatis berdasarkan volatilitas pasar (misal ATR).

- Take Profit Bertingkat: Atur dua level take profit (misal tutup setengah posisi di 2%, sisanya trailing stop) untuk meningkatkan rasio risk/reward.

- Optimasi Machine Learning: Latih model menggunakan data historis untuk mengoptimalkan parameter volMultiplier dan tpPerc.

- Verifikasi Multi-Timeframe: Perkenalkan konfirmasi S/R dari timeframe yang lebih tinggi untuk meningkatkan kualitas sinyal.

Kesimpulan

Strategi ini merancang kerangka trading probabilitas tinggi melalui verifikasi tiga lapis (posisi harga, volume, perilaku harga), sangat cocok untuk menangkap awal tren. Keunggulan inti terletak pada logika transparan dan risiko terkendali, namun perlu diperhatikan keterbatasannya di pasar ranging. Optimasi masa depan dapat difokuskan pada adaptasi parameter dan filter tren untuk meningkatkan stabilitas lebih lanjut.

/*backtest

start: 2024-04-24 00:00:00

end: 2024-12-31 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=5

strategy("S/R Breakout/Reversal + Volume + Alerts", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// === INPUTS ===- 1