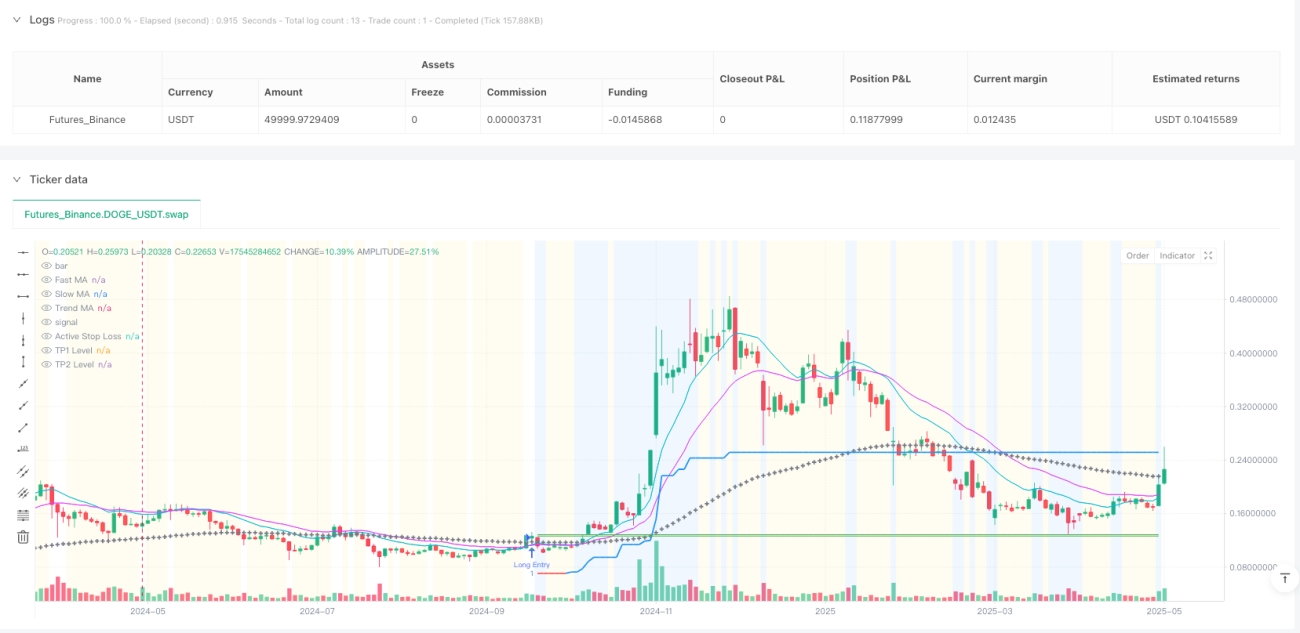

Ringkasan Strategi

Strategi perdagangan kuantitatif pelacak volatilitas persilangan rata-rata bergerak adaptif adalah strategi sistematis yang dirancang khusus untuk perdagangan frekuensi tinggi dan operasi jangka pendek. Inti strategi ini menggunakan persilangan antara rata-rata bergerak cepat (MA) dan rata-rata bergerak lambat sebagai pemicu sinyal utama, sekaligus menggabungkan berbagai filter kunci dan alat manajemen risiko yang presisi untuk menangkap fluktuasi harga kecil namun cepat. Strategi ini sangat dapat dikonfigurasi, memungkinkan pengguna untuk secara fleksibel memilih jenis rata-rata bergerak (EMA, SMA, WMA, HMA, VWMA) dan parameter periodenya, sehingga sesuai dengan kebutuhan perdagangan di berbagai ritme pasar. Selain itu, strategi ini siap digunakan dengan API, dapat diintegrasikan secara mulus ke dalam sistem perdagangan otomatis untuk mengeksekusi sinyal dengan cepat, sangat cocok bagi pedagang jangka pendek yang mengejar keuntungan kecil frekuensi tinggi.

Prinsip Strategi

Logika inti dari strategi ini terdiri dari beberapa bagian kunci berikut:

-

Sinyal Masuk: Terutama menggunakan persilangan/penembusan antara MA cepat dan MA lambat sebagai kondisi pemicu masuk. Pengguna dapat secara fleksibel mengonfigurasi jenis MA (EMA, SMA, WMA, HMA, VWMA) dan panjang periode untuk menyesuaikan sensitivitas sinyal dan beradaptasi dengan berbagai kondisi pasar.

-

Filter Tren: Secara opsional, strategi dapat menggunakan rata-rata bergerak jangka panjang sebagai filter tren besar, memastikan perdagangan hanya dilakukan sesuai arah tren utama, menghindari perdagangan jangka pendek yang melawan tren di pasar yang memiliki arah yang kuat.

-

Filter Konfirmasi:

- Filter Volatilitas ATR: Dirancang untuk menghentikan sementara masuknya posisi di pasar yang sangat datar atau "mati", di mana volatilitas di bawah ambang dinamis (berdasarkan rata-rata ATR), membantu mencegah osilasi di kondisi tidak bertren dan berenergi rendah.

- Filter Volume: Memvalidasi sinyal masuk dengan mensyaratkan partisipasi pasar minimal (perbandingan volume dengan rata-rata bergeraknya), menghindari masuk berdasarkan lonjakan likuiditas rendah atau aksi harga yang tidak signifikan.

-

Paket Manajemen Risiko:

- Stop Loss Volatilitas Awal: Stop loss awal berdasarkan ATR menyediakan titik awal objektif untuk definisi risiko setiap perdagangan, menyesuaikan dengan volatilitas terkini.

- Trailing Stop ATR: Sangat penting untuk pasar yang dinamis, garis trailing stop menyesuaikan seiring pergerakan harga yang menguntungkan, bertujuan melindungi keuntungan dari perdagangan jangka pendek yang sukses, sekaligus memotong kerugian relatif cepat saat tren berbalik.

- Stop Loss Impas (Opsional): Setelah mencapai TP1 atau harga bergerak sejauh ATR tertentu, stop loss secara otomatis dipindahkan ke harga masuk (ditambah buffer) untuk menetralisir risiko perdagangan yang telah menunjukkan kesuksesan awal dengan cepat.

- Dua Tingkat Profit: Menetapkan dua target profit TP1 dan TP2, TP1 dirancang untuk mengambil profit sebagian dengan cepat (misal 50%), sedangkan TP2 bertujuan meraih profit lebih besar dari sisa posisi.

-

Manajemen Posisi: Menggunakan ukuran posisi tetap (fixed quantity), memungkinkan kontrol presisi atas ukuran posisi setiap perdagangan, sangat penting untuk penerapan risiko yang konsisten dan pembangkitan perintah API di lingkungan frekuensi tinggi.

Keunggulan Strategi

Melalui analisis mendalam terhadap kode, strategi ini memiliki keunggulan yang jelas sebagai berikut:

-

Konfigurasi Tinggi: Pengguna dapat secara fleksibel menyesuaikan berbagai parameter, termasuk jenis MA dan periode, pengaturan filter, serta parameter manajemen risiko, sehingga strategi dapat beradaptasi dengan berbagai lingkungan pasar dan gaya perdagangan.

-

Mekanisme Filter Berlapis: Menggabungkan filter tren, volatilitas, dan volume, secara efektif mengurangi sinyal palsu dan kebisingan pasar, meningkatkan kualitas perdagangan.

-

Manajemen Risiko yang Komprehensif: Strategi ini dilengkapi dengan beberapa mekanisme stop loss (awal, trailing, impas) dan dua target profit, mencapai kontrol risiko dan perlindungan keuntungan yang presisi.

-

Desain Ramah API: Logika masuk dan keluar yang jelas menghasilkan sinyal yang tidak ambigu, memudahkan integrasi dengan sistem perdagangan eksternal, memungkinkan eksekusi order hampir secara instan.

-

Kontrol Posisi Presisi: Ukuran posisi tetap menyederhanakan muatan untuk titik akhir API, membuat eksekusi otomatis lebih andal.

-

Adaptabilitas Tinggi: Melalui penyesuaian parameter, strategi dapat berubah dari mode perdagangan jangka pendek frekuensi tinggi menjadi mode pelacakan tren jangka panjang, beradaptasi dengan berbagai kondisi pasar dan preferensi perdagangan individu.

Risiko Strategi

Meskipun strategi ini dirancang dengan baik, masih terdapat beberapa risiko dan tantangan potensial:

-

Risiko Optimasi Parameter: Karena strategi memiliki banyak parameter yang dapat dikonfigurasi, optimasi berlebihan dapat menyebabkan hasil backtest bagus tetapi kinerja aktual buruk (overfitting). Investor harus memvalidasi pada data di luar sampel atau melakukan forward testing untuk menghindari risiko ini.

-

Dampak Biaya Transaksi: Perdagangan frekuensi tinggi berarti banyak transaksi, komisi dan slippage yang terakumulasi dapat secara signifikan mempengaruhi profitabilitas bersih. Pastikan untuk menghitung biaya-biaya ini secara akurat dalam pengaturan dan backtest sebelum digunakan.

-

Fluktuasi Kualitas Sinyal: Di berbagai kondisi pasar, keandalan sinyal persilangan MA dapat berubah, terutama di pasar yang bergerak sideways atau sangat fluktuatif.

-

Ketergantungan Teknis: Sebagai strategi yang siap-API, efektivitasnya sebagian bergantung pada kecepatan eksekusi dan stabilitas teknis. Keterlambatan sistem atau kegagalan dapat menyebabkan hilangnya peluang atau penyimpangan eksekusi.

-

Batasan Ukuran Dana: Ukuran posisi tetap mungkin tidak cocok untuk semua ukuran akun. Akun kecil mungkin menghadapi risiko berlebihan, sementara akun besar mungkin tidak dapat memanfaatkan dana secara optimal.

Arah Optimasi Strategi

Berdasarkan desain strategi dan potensi risiko, berikut adalah beberapa arah optimasi yang mungkin:

-

Parameter Adaptif: Merancang parameter kunci (seperti pengali ATR dan periode MA) agar menyesuaikan secara otomatis berdasarkan kondisi pasar, meningkatkan kemampuan adaptasi strategi di berbagai fase pasar.

-

Peningkatan Filter Cerdas: Mengintegrasikan indikator kondisi pasar tambahan (seperti struktur pasar, pengenalan pola volatilitas, atau korelasi aset terkait) untuk meningkatkan akurasi filter lebih lanjut.

-

Manajemen Posisi Dinamis: Mengganti ukuran posisi tetap dengan perhitungan posisi dinamis berdasarkan ukuran akun, volatilitas saat ini, dan kinerja strategi terkini, untuk mencapai manajemen modal yang lebih cerdas.

-

Konfirmasi Multi-Timeframe: Memvalidasi sinyal pada kerangka waktu yang berbeda, memastikan arah perdagangan konsisten dengan struktur pasar yang lebih besar, mengurangi perdagangan yang tidak perlu.

-

Integrasi Pembelajaran Mesin: Menggunakan algoritma pembelajaran mesin untuk menganalisis kinerja sinyal historis, memprediksi probabilitas keberhasilan sinyal di masa depan, dan memprioritaskan eksekusi perdagangan dengan probabilitas kemenangan tinggi.

-

Manajemen Sesi Perdagangan: Menambahkan filter waktu perdagangan, menghindari sesi dengan likuiditas rendah atau volatilitas tinggi, fokus pada jendela perdagangan paling efisien.

-

Filter Korelasi: Untuk perdagangan multi-aset, menambahkan analisis korelasi dengan pasar terkait, menghindari paparan berlebihan terhadap faktor risiko tertentu.

Kesimpulan

Strategi perdagangan kuantitatif pelacak volatilitas persilangan rata-rata bergerak adaptif adalah sistem perdagangan frekuensi tinggi yang komprehensif, menggunakan persilangan MA sebagai pemicu sinyal, dikombinasikan dengan berbagai filter kunci dan alat manajemen risiko yang presisi, dirancang khusus untuk menangkap fluktuasi harga kecil namun cepat. Kekuatan strategi ini terletak pada konfigurasi tingginya dan kerangka kerja manajemen risiko yang komprehensif, memungkinkan pedagang untuk menyetel parameter perdagangan secara halus sesuai toleransi risiko pribadi dan kondisi pasar.

Bagi pedagang frekuensi tinggi, strategi ini menyediakan logika masuk dan keluar yang jelas, serta kemampuan integrasi yang mulus dengan platform eksekusi eksternal, yang sangat penting untuk mengeksekusi keputusan dengan cepat di pasar yang berubah seketika. Namun, saat menggunakan strategi ini, perhatian khusus harus diberikan pada risiko akumulasi biaya transaksi dan optimasi berlebihan, memastikan robustness dan profitabilitas strategi dalam perdagangan nyata.

Pada akhirnya, strategi ini mewakili pendekatan yang seimbang – memanfaatkan kekuatan indikator teknis dan alat manajemen risiko, sambil mempertahankan fleksibilitas yang cukup untuk beradaptasi dengan kondisi pasar yang terus berubah. Melalui penyesuaian parameter yang hati-hati dan perbaikan pemantauan berkelanjutan, strategi ini dapat menjadi komponen berharga dalam portofolio perdagangan kuantitatif.

- 1