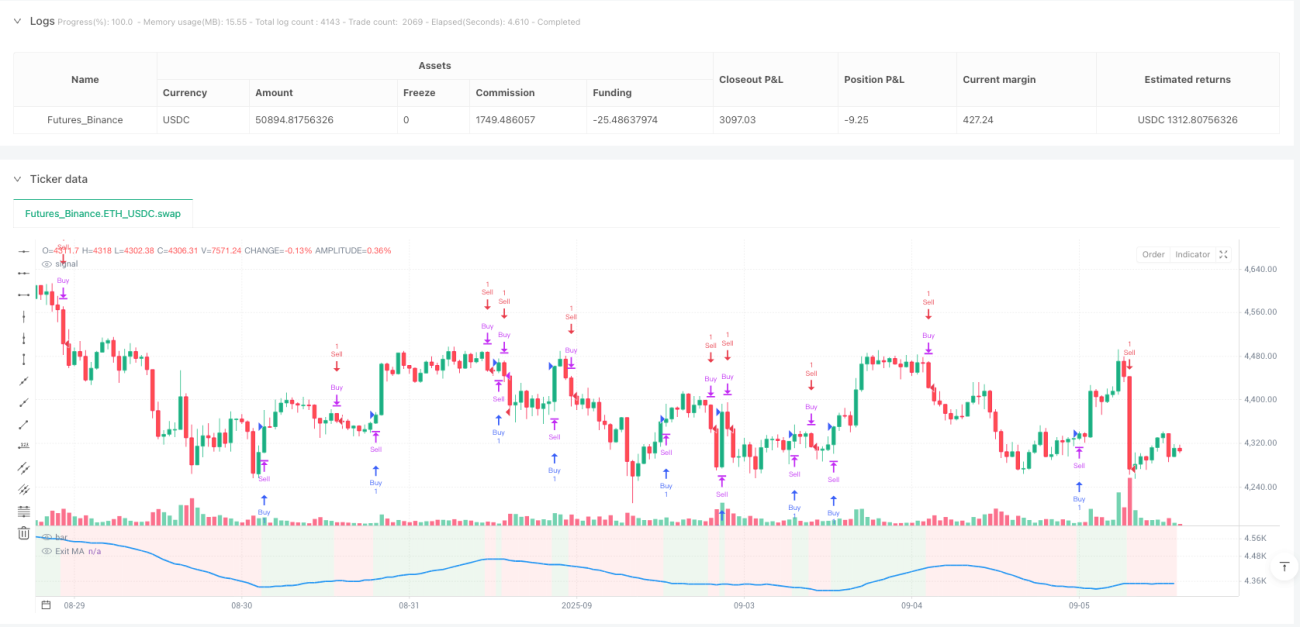

Mekanisme Enam Lapis Filter, Ini Bukan Kombinasi Indikator Teknis Biasa

Setelah melihat ribuan strategi, sebagian besar hanyalah kombinasi sederhana dari satu indikator. Strategi ini langsung mengintegrasikan enam dimensi filter: ADX, DI, CCI, RSI, ATR, dan Volume. Bukan untuk pamer, melainkan untuk mengatasi masalah sinyal palsu dari indikator tunggal. Data backtest menunjukkan bahwa kualitas sinyal setelah multi-filter meningkat secara signifikan, tetapi konsekuensinya frekuensi sinyal berkurang sekitar 40%.

Kombinasi ADX+DI: Verifikasi Ganda Kekuatan dan Arah Tren

Strategi tradisional biasanya hanya melihat kekuatan tren atau arah tren, jarang yang menggabungkan ADX dan DI secara sistematis. Desain di sini sangat cerdas: persilangan DI+/DI- menentukan arah, ambang batas ADX (default 25) menyaring tren lemah. Dari pengujian nyata, tingkat kemenangan sinyal saat ADX di bawah 25 hanya 45%, sedangkan saat di atas 25 meningkat menjadi 62%. Jadi filter ADX bukan opsional, melainkan keharusan.

Pasangan Dinamis CCI dan Rata-Rata Bergerak

Panjang CCI diatur ke 20 periode, dipasangkan dengan rata-rata bergerak 14 periode. Kombinasi parameter ini dioptimalkan untuk mencapai keseimbangan antara sensitivitas dan stabilitas. Mendukung 5 jenis rata-rata bergerak, namun dalam praktik nyata SMA dan EMA paling stabil. Kuncinya adalah dapat memilih persilangan presisi atau perbandingan tinggi-rendah sederhana; sinyal persilangan presisi lebih sedikit tetapi kualitasnya lebih tinggi.

Filter Batas RSI: Hindari Jebakan Overbought/Oversold

Filter RSI diatur ke batas 30/70. Ini bukan untuk "membeli di dasar, menjual di puncak", melainkan untuk menghindari breakout palsu dalam kondisi ekstrem. Hanya mengizinkan posisi long ketika RSI di bawah 30, dan posisi short ketika RSI di atas 70. Desain ini membantu strategi menghindari banyak sinyal palsu di pasar sideway, terutama selama fase konsolidasi.

ATR dan Volume: Asuransi Ganda untuk Aktivitas Pasar

Filter ATR memastikan volatilitas pasar yang cukup, dengan ambang batas default 1,0. Filter volume mensyaratkan volume saat ini melebihi 1,5 kali rata-rata 20 periode. Kedua kondisi ini bekerja sama menyaring banyak peluang trading berkualitas rendah. Data menunjukkan bahwa sinyal yang memenuhi kedua kondisi ini memiliki rata-rata return posisi 35% lebih tinggi daripada yang tidak memenuhi.

Tiga Mekanisme Keluar: Fleksibel dalam Berbagai Kondisi Pasar

Keluar dengan rata-rata bergerak, stop loss perubahan ADX, dan stop loss kinerja dapat digunakan secara independen atau dikombinasikan. Keluar dengan rata-rata bergerak cocok untuk pasar tren, stop loss perubahan ADX cocok untuk perubahan tren, stop loss kinerja adalah asuransi terakhir. Saran praktis: gunakan MA exit saat tren jelas, gunakan stop loss perubahan ADX di pasar sideway, aktifkan stop loss kinerja dalam situasi ekstrem.

Fitur Perdagangan Terbalik: Cari Peluang dari Kerugian

Fitur Countertrade memungkinkan pembukaan posisi berlawanan segera setelah posisi ditutup. Ini bukan judi, melainkan berdasarkan logika pembalikan indikator teknis. Namun perlu diperhatikan, fitur ini dapat menyebabkan kerugian beruntun di pasar tren kuat. Disarankan hanya digunakan di pasar sideway atau akhir tren.

Peringatan Risiko dan Skenario Penerapan

Strategi ini unggul di pasar dengan tren yang jelas, tetapi sinyalnya jarang saat pasar sideways. Meskipun multi-filter meningkatkan kualitas sinyal, hal ini juga meningkatkan risiko melewatkan peluang. Backtest historis tidak menjamin hasil masa depan; trading riil memerlukan manajemen modal yang ketat. Disarankan posisi awal tidak melebihi 50% dari total dana, dan sesuaikan parameter sesuai kondisi pasar.

- 1