トレンドフォロー四要素戦略

概要

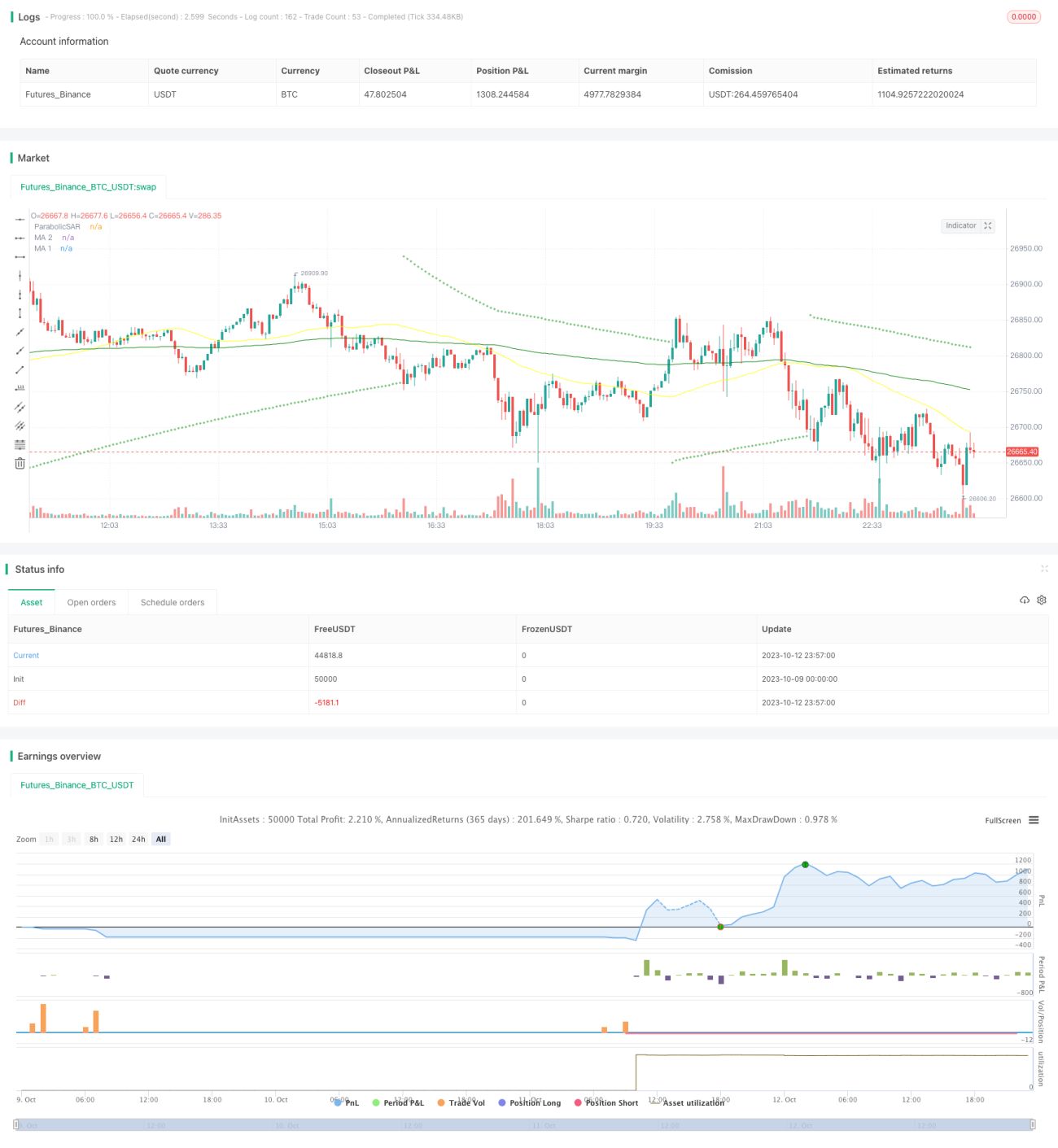

本戦略は、sar指標、rsi指標、vol指標、ma移動平均線の4つの要素を総合的に活用してトレンドを識別し、堅牢なリスク管理措置を講じてトレンドに追随し利益を得ます。戦略はsar指標を主軸とし、rsiの買われすぎ・売られすぎの境目で反転シグナルを識別し、vol指標で出来高の特徴を判定し、ma移動平均線で主要なトレンド方向を判断します。複数のインジケーターを組み合わせて判断することで、偽のシグナルを排除し、真のトレンド方向を特定します。リスク管理ではストップロスとテイクプロフィットを設定し、1回の損失と累積利益を効果的にコントロールします。本戦略は中長期の保有者に適しており、メインストリームのトレンドに沿って安定した収益を得ることができます。

戦略の原理

本戦略では、以下の4つの主要なテクニカル指標を使用します。

-

Parabolic SAR: この指標は、点とトレンドの関係を利用してトレンド方向と反転点を判断します。点が価格の上にあるときは強気、点が価格の下にあるときは弱気を示します。点が価格を通過するときはトレンド反転を表します。戦略ではsarを主指標としてトレンド方向を判断します。

-

RSI: 相対力指数。この指標は0~100の間で変動し、市場の買われすぎ・売られすぎの状況を判断します。RSIが70を超えると買われすぎ領域、30を下回ると売られすぎ領域となり、50付近に戻ると中立領域と見なします。戦略ではRSIを使用して買われすぎ・売られすぎの反転シグナルを判断します。

-

VOL: 出来高指標。戦略ではVOLを使用して出来高の拡大の特徴を判定し、トレンドを確認し、反転シグナルの質を判断します。

-

MA: 移動平均線。戦略では長期と短期の移動平均線を使用して、主要および副次的なトレンド方向を判断します。短期移動平均線が長期移動平均線を上抜けると買いシグナル、短期移動平均線が長期移動平均線を下抜けると売りシグナルとなります。

取引シグナル生成ルール:

買い条件: SARの点がローソク足の下に移動し、かつRSIが下から上昇して中立領域に入り、VOLが明確に拡大し、短期移動平均線が下から上に長期移動平均線を上抜ける。

売り条件: SARの点がローソク足の上に移動し、かつRSIが上から下降して中立領域に入り、VOLが明確に拡大し、短期移動平均線が上から下に長期移動平均線を下抜ける。

本戦略では、テイクプロフィットとストップロスのリスク管理ルールも設定しています。テイクプロフィットはエントリー価格の2倍、ストップロスはエントリー価格の0.8倍とし、利益を確実に確保し、リスクを効果的にコントロールします。

優位性分析

本戦略には以下の優位性があります。

- 複数のインジケーターを組み合わせた設計により、偽のシグナルを排除し、トレンドの転換を正確に捉えます。

- リスク管理としてストップロスとテイクプロフィットを設定し、リスクを効果的にコントロールします。

- ポジション管理で分割エントリーと分割利確を行い、利益を最大化します。

- パラメータは繰り返し最適化とテストを経ており、パラメータの堅牢性が保証されています。

- バックテストのデータは十分であり、実際の取引環境をシミュレーションしています。

- 操作ロジックは明確でシンプルであり、理解と実装が容易です。

リスク分析

本戦略には以下のリスクも存在します。

- 市場の異常な変動によりストップロスが突破される可能性。適切にストップロスの幅を広げることを推奨します。

- 取引銘柄の流動性不足によりストップロスが執行できない可能性。流動性の高い取引銘柄を選択すべきです。

- システムリスクにより異常なギャップが発生する可能性。レバレッジを減らし、価値の基盤が良好な資産を保有すべきです。

- パラメータの過度な最適化により曲線が美しくなりすぎる可能性。堅牢性を高めるためにパラメータを適度に弱めるべきです。

- 取引頻度が高すぎることによるスリッページコスト。取引シグナルの生成間隔を適度に広げることができます。

- シグナルの効果が弱まった場合、迅速に更新する必要があります。定期的にバックテストを行い、パラメータ設定を最適化すべきです。

最適化の方向性

本戦略は以下の点からさらに最適化することが可能です。

- より多くのインジケーターの組み合わせ(MACD、KDなど)をテストし、より良いマッチングを模索します。

- MAの期間パラメータ設定を最適化し、より明確な主要・副次トレンドを識別します。

- 最適なリスクリワード比を得るために、テイクプロフィットとストップロスの係数を最適化します。

- 異なる銘柄におけるパラメータの堅牢性をテストし、最適なパラメータの組み合わせを探します。

- 機械学習モデルを追加し、取引シグナルの判断を補助します。

- 適応型ストップロスアルゴリズムを追加し、ストップロスを実際の変動に近づけます。

- より長期の期間パラメータ設定をテストし、利確範囲を拡大します。

まとめ

本戦略は複数のインジケーターを総合的に活用して偽のシグナルを排除しトレンド方向を確定し、ストップロスとテイクプロフィット措置を設定してリスクをコントロールし、パラメータの最適化と組み合わせの調整を通じて戦略の効果を継続的に向上させます。どの戦略も未来を完璧に予測することはできませんが、体系的な取引計画と優れたリスク管理は利益を得る確率を大幅に高めます。本戦略は比較的堅牢なトレンドフォロー手法を提供し、長期的な安定収益を合理的に追求する投資家に適しています。

- 1