三重モード・レンジ取引戦略

概要

トリプルモード・レンジ取引戦略は、複数のテクニカル指標を組み合わせた短期取引戦略です。この戦略は、スーパートレンド指標、SSLハイブリッド移動平均線、改良型QQE指標を組み合わせることで、安定した取引シグナルを生成します。暗号通貨や株式など、ボラティリティの高い取引商品に適しており、特にブレイクアウト後の相場で良好なパフォーマンスを示します。

原理

エントリーシグナル

ロングエントリー:

- スーパートレンドがショートからロングに転換

- 終値がSSLハイブリッドベースラインの上限を上抜け

- 改良型QQEが青色(ロング)

ショートエントリー:

- スーパートレンドがロングからショートに転換

- 終値がSSLハイブリッドベースラインの下限を下抜け

- 改良型QQEが赤色(ショート)

エグジットシグナル

ロングエグジット:スーパートレンドがロングからショートに転換

ショートエグジット:スーパートレンドがショートからロングに転換

ストップロス

パーセンテージストップロス、ATRストップロス、または最近の高値・安値によるストップロスを選択可能

テイクプロフィット(利確)

利確リターン比率を設定し、自動的に利確価格を計算

資金管理

資金管理ロジックを使用してポジションサイズを制御するかどうかを選択可能

描画

- スーパートレンドライン、SSLハイブリッド移動平均線チャネルの描画

- EMA移動平均線の描画を選択可能

- ロング・ショートのエントリーライン、ストップロスライン、テイクプロフィットラインの描画

- ロング・ショートのエントリーラベルの描画

メリット

- 複数指標の組み合わせによる安定した取引シグナル

スーパートレンド、SSLハイブリッド移動平均線、改良型QQE指標を組み合わせることで、異なる指標が相互に検証し合い、ダマシのブレイクアウトをフィルタリングし、高品質な取引シグナルを形成します。

- ボラティリティの高い商品に適したレンジ取引

短期取引方式を採用し、中短期の価格変動を捉えることに特化しています。スーパートレンドは価格トレンドを効果的に追跡し、SSLハイブリッド移動平均線はサポート・レジスタンスラインを明確に識別します。両者を組み合わせることで、レンジ相場で利益を得ることができます。

- 複数のストップロス・利確方法から選択可能

ストップロスはパーセンテージ、ATR値、または最近の極値から選択できます。利確はリターン比率を設定可能。資金管理でポジションサイズを制御できます。ユーザーは商品特性とリスク選好に応じて自由に組み合わせられます。

- 明確な描画

戦略の描画は明確で、ストップロスラインや利確ラインが視覚的に表示されます。エントリーラインのマークにより取引シグナルを容易に識別できます。

リスクと最適化

- 小幅な損失が発生する可能性

短期取引であるため、通常のレンジ相場での小幅な損失を完全に回避することはできません。ストップロス幅を適度に緩和したり、資金管理ロジックを最適化することで対処できます。

- ダマシのブレイクアウトリスク

価格がダマシのブレイクアウトを起こした場合、誤ったシグナルが発生する可能性があります。異なる期間のEMAをテストしてダマシをフィルタリングしたり、トレンド識別指標のパラメータを最適化することで対処できます。

- 指標の劣化リスク

基礎指標が機能しなくなった場合、複数の誤ったシグナルが発生します。指標の有効性を定期的に検証し、問題があれば適宜調整する必要があります。

- バックテスト期間の最適化

現在のバックテスト期間は固定されており、商品ごとに異なる相場サイクルに対応できません。各商品の主要取引時間帯に合わせた最適化が推奨されます。

- 商品適合性の最適化

商品のデータ特性に合わせて戦略パラメータを微調整し、ロング・ショートの勝率を高めることができます。ステップワイズ最適化を用いて、異なるパラメータが戦略に与える影響を比較することを推奨します。

まとめ

本戦略は複数の指標を組み合わせて取引シグナルを形成し、ダマシのブレイクアウトを効果的にフィルタリングできるため、ボラティリティの高い暗号通貨や個別株に適しています。また、複数のストップロス・利確方法から選択可能で、柔軟に使用できます。総じて、本戦略は安定した取引シグナルを生成し、中短期のレンジ相場で良好な利益を得ることができます。さらなる最適化により、異なる取引商品に合わせたパラメータ調整が可能となり、戦略のプロフィットファクターを向上させることができます。本戦略は、さらなる研究に値する効率的な取引システムです。

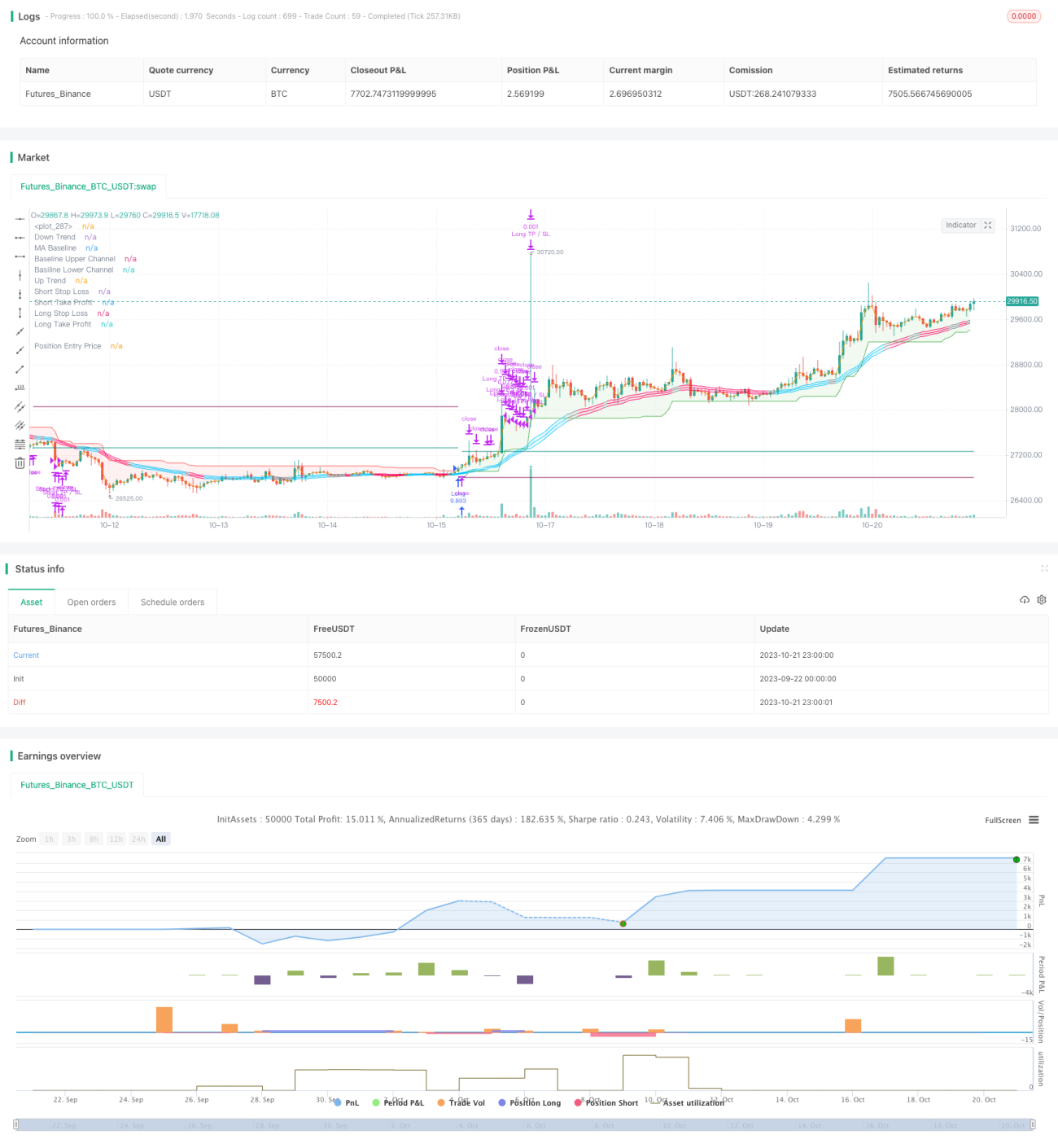

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1