トレンド反転ボラティリティ複合戦略

1

Follow

1802

Followers

概要

この戦略は、トレンド反転戦略と統計的ボラティリティ戦略を組み合わせた連合戦略であり、より強力な取引シグナルを獲得することを目的とします。

戦略の原理

本戦略は以下の2つの部分で構成されます。

-

トレンド反転戦略

- 123パターンを使用してトレンドの反転ポイントを判断します。具体的には、終値が2日連続で上昇し、かつ9日ストキャスティクス・スローラインが50未満の場合は強気と見なし、終値が2日連続で下落し、かつ9日ストキャスティクス・ファストラインが50超の場合は弱気と見なします。

-

統計的ボラティリティ戦略

- 極値法を用いて過去30日間の統計的ボラティリティを計算します。ボラティリティが0.5%を超える場合は強気、0.16%未満の場合は弱気と見なします。

最終的に、両方の戦略のシグナルが一致(両方とも強気または両方とも弱気)した場合にのみ取引シグナルを生成し、一致しない場合は取引を行いません。

戦略の優位性分析

本戦略は異なるタイプの2つの戦略を組み合わせることで、シグナルの信頼性を高めます。

- 123パターンによる判断はトレンド反転ポイントを正確に捉え、突発的な価格変動による誤った判断を防ぎます。

- 統計的ボラティリティは直近1ヶ月の市場の変動状況を反映し、ボラティリティが高く取引機会の多い時間帯をフィルタリングできます。

両戦略が相互に検証し合うことで、市場の重要な転換点をより的確に捉え、より正確で信頼性の高い取引シグナルを得ることができます。

リスク分析

- 123パターンは偽のブレイクアウトによるリスクを完全には回避できません。異常な値動きが発生した場合、シグナルを誤認識する可能性があります。

- 統計的ボラティリティは過去のデータのみを考慮しており、将来のボラティリティのトレンドを予測できません。市場のボラティリティが急激に拡大または収縮した場合も誤ったシグナルを発生させる恐れがあります。

- 両戦略はパラメータの最適化に依存しています。パラメータ設定が適切でない場合、シグナルの品質は大幅に低下します。

- 連合戦略は信頼性を高める一方で、強い単独シグナルを見逃す可能性もあります。

最適化の方向性

- ボリンジャーバンドやKDJなどの追加インジケーターを組み合わせ、投票メカニズムを形成する。

- 機械学習アルゴリズムを導入し、より多くの過去データを利用してトレンド反転の確率を判断する。

- シグナルの強弱をフィルタリングするためのしきい値を設定し、ノイズの影響を排除する。

- パラメータ設定を最適化し、異なる銘柄や期間に応じてパラメータを調整する。

- 連合戦略のリスクを管理するためにストップロス・メカニズムを追加する。

まとめ

本戦略はトレンド反転戦略と統計的ボラティリティ戦略を組み合わせることでシグナルの品質を向上させ、市場の重要な転換点において比較的正確な取引指示を提供します。ただし、誤認識リスクやパラメータ最適化の問題に注意する必要があります。さらに多くのインジケーターや機械学習などの手段を組み合わせることで、より安定した信頼性の高い取引シグナルを得ることができます。

Source

Pine

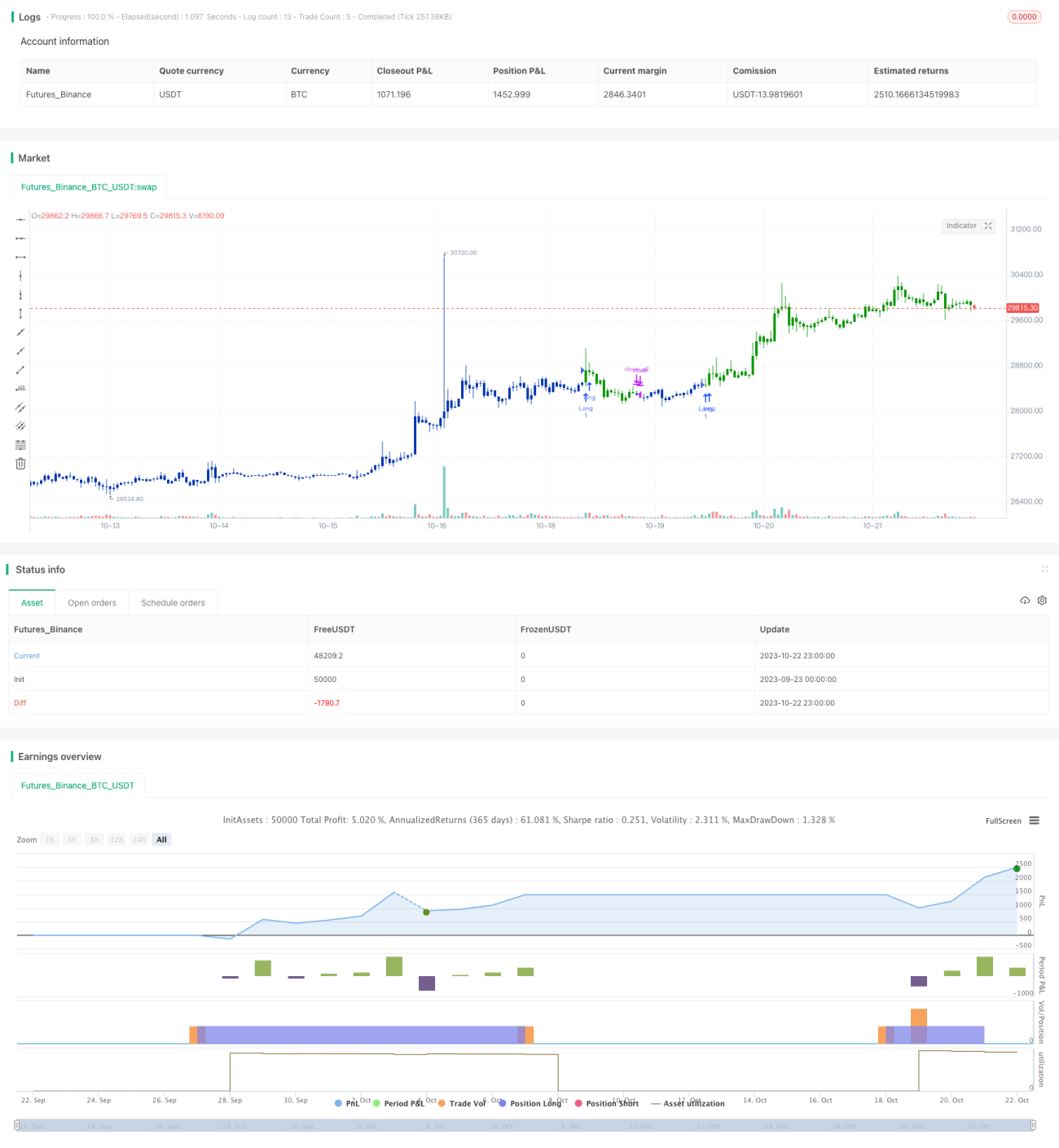

/*backtest

start: 2023-09-23 00:00:00

end: 2023-10-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 31/07/2021

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1