ブレイクアウト・トレーリングストップV2戦略

概要

本戦略は、ブレイクアウト戦略とトレンドフォロー型ストップロス戦略の利点を組み合わせたものであり、長期チャートにおけるサポート・レジスタンスのブレイクアウトシグナルを捉えると同時に、移動平均線を用いたストップロストレールにより、長期トレンドの方向に利益を上げつつリスクを管理することを目的としています。

戦略の原理

-

戦略はまず、異なるパラメータを持つ複数の移動平均線を計算し、それぞれトレンド判断、サポート・レジスタンス、ストップロストレールに使用します。

-

次に、指定期間内の最高値と最安値を見つけ、エントリーのためのサポート・レジスタンス領域とします。価格がこれらのサポート・レジスタンスをブレイクしたときにシグナルが発生します。

-

戦略は、最高値のブレイクを買いシグナルとして買いエントリーし、最安値のブレイクを売りシグナルとして売りエントリーします。

-

エントリー後は、最安値のブレイクポイントをストップロスとしてポジションを保有します。

-

ポジションが利益状態に入ると、ストップロスは移動平均線を追跡するように切り替わります。価格が移動平均線を下回った場合、そのローソク足の最安値にストップポイントを設定します。

-

これにより利益を確定しつつ、ポジションがトレンドに沿って動くのに十分な余地を持たせることができます。

-

戦略はまた、平均真実範囲(ATR)を追加し、適切な範囲内でのブレイクのみでエントリーし、過度に拡大したブレイクを避けるようにします。

戦略の優位性分析

-

ブレイクアウト戦略とトレンドフォロー型ストップロス戦略の二重の利点を組み合わせています。

-

長期トレンドに沿ったブレイクでエントリーできるため、利益を得る確率が向上します。

-

ストップロス戦略はポジションを保護すると同時に、十分な動きの余地を与えます。

-

ボラティリティフィルターを追加することで、過度な上昇による不利なブレイクを回避します。

-

自動売買が可能で、一部時間帯のコピートレードに適しています。

-

異なる期間の移動平均線をカスタマイズして操作できます。

-

ストップロストレール方式を柔軟に調整できます。

戦略のリスク分析

-

ブレイクアウト戦略は、偽のブレイクのリスクが発生しやすいです。ブレイク確認を適度に緩和することも可能です。

-

ブレイクシグナルを発生させるには十分な値動きが必要であり、不安定な相場では効果が薄れやすいです。

-

一部のブレイクはあまりにも短すぎて捉えられない可能性があります。時間軸を短くして機会を増やすこともできます。

-

トレーリングストップはレンジ相場ではストップが頻発する可能性があります。ストップ幅を適度に広げることもできます。

-

ボラティリティフィルターが一部の機会を逃す可能性があります。フィルターパラメータを緩和することもできます。

戦略の最適化の方向性

-

異なる移動平均線パラメータの組み合わせをテストし、最適なパラメータを見つけます。

-

チャネルやローソク足パターンなど、異なるブレイク確認メカニズムをテストします。

-

異なるストップロストレール方式を試し、最適なストップロスを見つけます。

-

ポジションスコアなどの資金管理戦略を最適化します。

-

統計的テクニカル指標フィルターを追加し、フィルターの精度を向上させます。

-

異なる銘柄での戦略効果をテストします。

-

機械学習アルゴリズムを追加し、戦略効果を向上させます。

まとめ

本戦略はブレイクアウトの考え方とトレンドフォロー型ストップロスの考え方を統合し、長期トレンドの方向性が正しいという前提のもとで、利益空間を最適化することができます。鍵となるのは最適なパラメータの組み合わせを見つけ、優れた資金管理戦略と組み合わせて、長期トレンドの機会を捉えつつリスクを管理可能にすることです。本戦略はさらなる最適化を経て、信頼性の高い長期トレンド戦略となる可能性を秘めています。

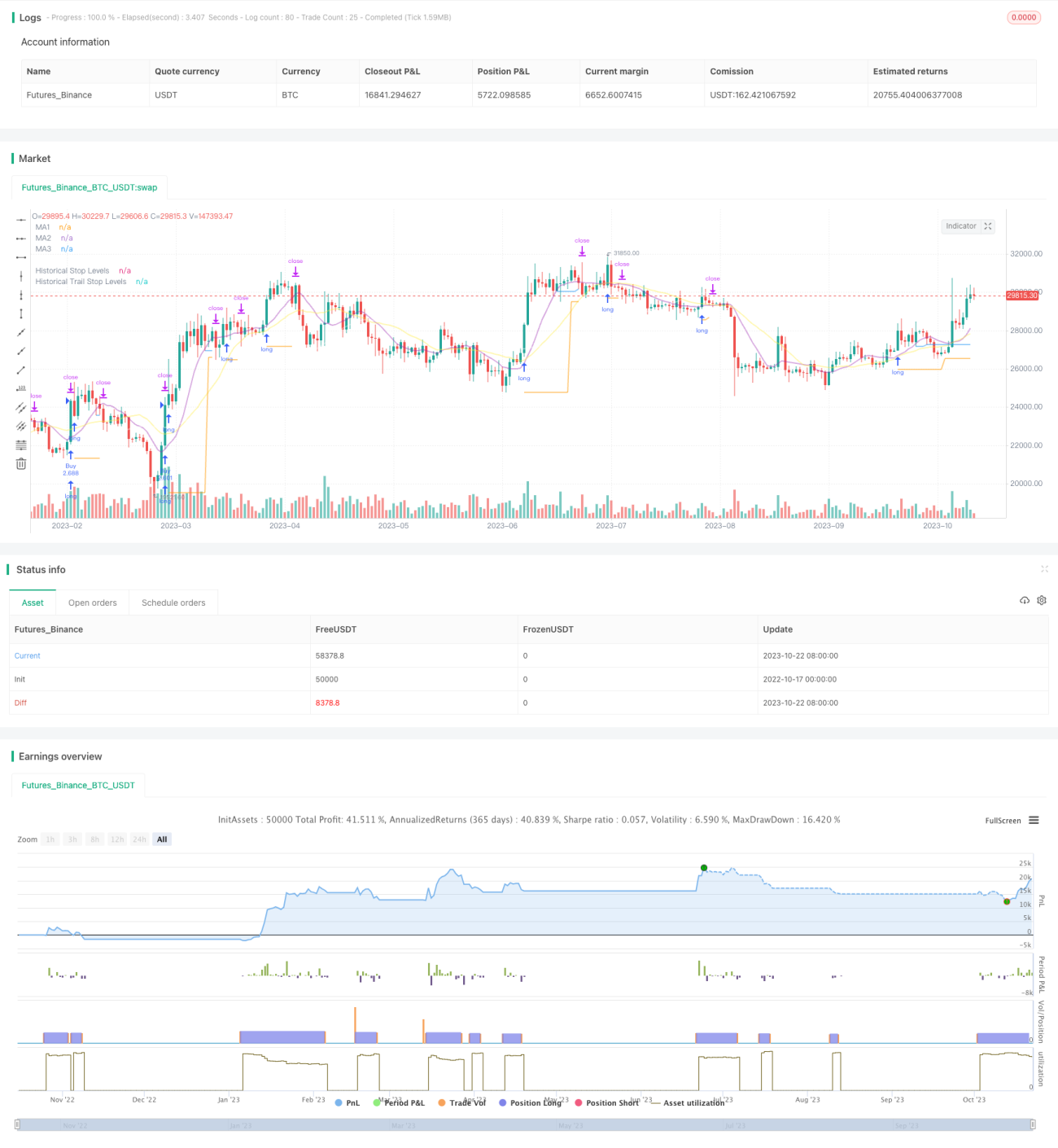

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1