両側バンドフィルター戦略

[trans]

概要

両側バンドパスフィルター戦略は、2010年にBroderがStocks & Commodities誌に発表した記事を基に改変された戦略です。この戦略は、Broderのバンドパスフィルターの値を計算し、株価の変動を識別して取引シグナルを提供します。バンドパスフィルターの値が閾値を上回った場合は売り、下回った場合は買いとし、トレンドフォローを実現します。

戦略原理

この戦略は主に以下のステップに分かれます:

-

パラメータの初期化: Broderバンドパス長さ

Length、変動係数Delta、売りゾーン閾値SellZone、買いゾーン閾値BuyZoneなどが含まれます。 -

Broderバンドパスフィルター

BPの計算: 一連の三角関数を使用してバンドパスフィルターの値を計算します。 -

ポジション方向の判断:

BPがSellZoneより高い場合は売り;BuyZoneより低い場合は買い; それ以外は現在のポジションを維持。 -

シグナルの出力: ポジション方向に基づいて買い/売りシグナルを出力。

-

ローソク足の色の設定: シグナル結果に基づいてローソク足の色を設定。

-

バンドパスフィルター曲線の描画。

この戦略は、Broderバンドパスフィルターを通じて市場の短期変動を捉え、変動が一定の幅に達したときに取引シグナルを生成し、市場トレンドに従って取引を行います。

優位性分析

-

Broderバンドパスフィルターに基づくため、市場変動に対してより敏感で、短期トレンドを捉えることができます。

-

パラメータ最適化により、変動に対する感度を調整し、異なる市場環境に適応できます。

-

戦略ロジックはシンプルで明確であり、理解・実装が容易です。

-

パラメータ調整が容易で、最適なパラメータ組み合わせを見つけることができます。

-

可視化されたバンドパスフィルター曲線により、市場変動を直感的に表示できます。

リスク分析

-

Broderバンドパスフィルターは過度に最適化されると過敏になり、誤ったシグナルを生成する可能性があります。

-

変動の終了点を特定できないため、損失が拡大する可能性があります。

-

取引頻度が高くなりすぎる可能性があり、取引コストとスリッページリスクが増加します。

-

突発的なイベントの影響を受けやすく、誤ったシグナルが発生する可能性があります。

-

異なる銘柄や市場環境に適応するために、適切にパラメータを調整する必要があります。

-

1回の取引の損失を管理するために、ストップロスを設定することを検討できます。

-

適切に退出時間を延長するか、フィルター条件を使用して誤ったシグナルを減らすことができます。

最適化の方向性

-

パラメータを最適化し、最適なパラメータ組み合わせを見つけます。最適化目標として、勝率、損益比、シャープレシオなどの指標を考慮できます。

-

フィルター条件を追加します。例えば、移動平均線のブレイクアウトや価格パターンなど、非トレンド領域での取引を避けます。

-

複数の銘柄のパラメータ組み合わせを組み合わせたバスケットトレーディングを検討し、片方向リスクを分散します。

-

ストップロスロジックを追加し、1回の取引の損失を管理します。ダイナミックストップロスやトレーリングストップロスを検討できます。

-

移動利食いを追加して、利益を確定します。トレンド段階に応じて異なる利食い位置を設定することもできます。

-

エントリーシグナルを最適化し、レンジ相場での誤ったシグナルを避けます。保有期間を延長するか、価格ブレイクアウトをエントリーシグナルとして設定することを検討できます。

-

複数銘柄のアービトラージシステムに拡張し、銘柄間の価格差を利用してヘッジします。

-

バックテスト最適化を実施し、最適な銘柄選択とリバランス戦略を見つけます。

まとめ

両側バンドパスフィルター戦略は、Broderバンドパスフィルターを計算して価格変動の強さを判断し、変動が閾値に達したときに取引シグナルを生成します。市場の短期トレンドに対する感度が高く、実装が簡単という利点があります。ただし、この戦略はパラメータと取引頻度に敏感であるため、誤ったシグナルを減らし、リスクを管理するために適切な最適化が必要です。全体的に、この戦略は短期トレンドを捉えるための一つの選択肢を提供しますが、過剰最適化の問題に注意し、他のテクニカル指標と適切に組み合わせて取引する必要があります。

-

価格差を利用したヘッジのためのクロスアセットアービトラージシステムに拡張する。

-

最適な資産選択とリバランス戦略のためのバックテスト最適化。

要約

デュアルバンドパスフィルター戦略は、Broderのバンドパスフィルターを使用して価格変動を判断し、変動がしきい値に達したときにシグナルを生成します。短期的なトレンドに対する高い感度と実装の容易さが利点です。しかし、パラメータや取引頻度に敏感であり、誤ったシグナルを減らしリスクを管理するための最適化が必要です。全体的には、短期的なトレンドを捉えるための選択肢を提供しますが、過学習を避け、他のテクニカルツールと組み合わせて取引することが推奨されます。

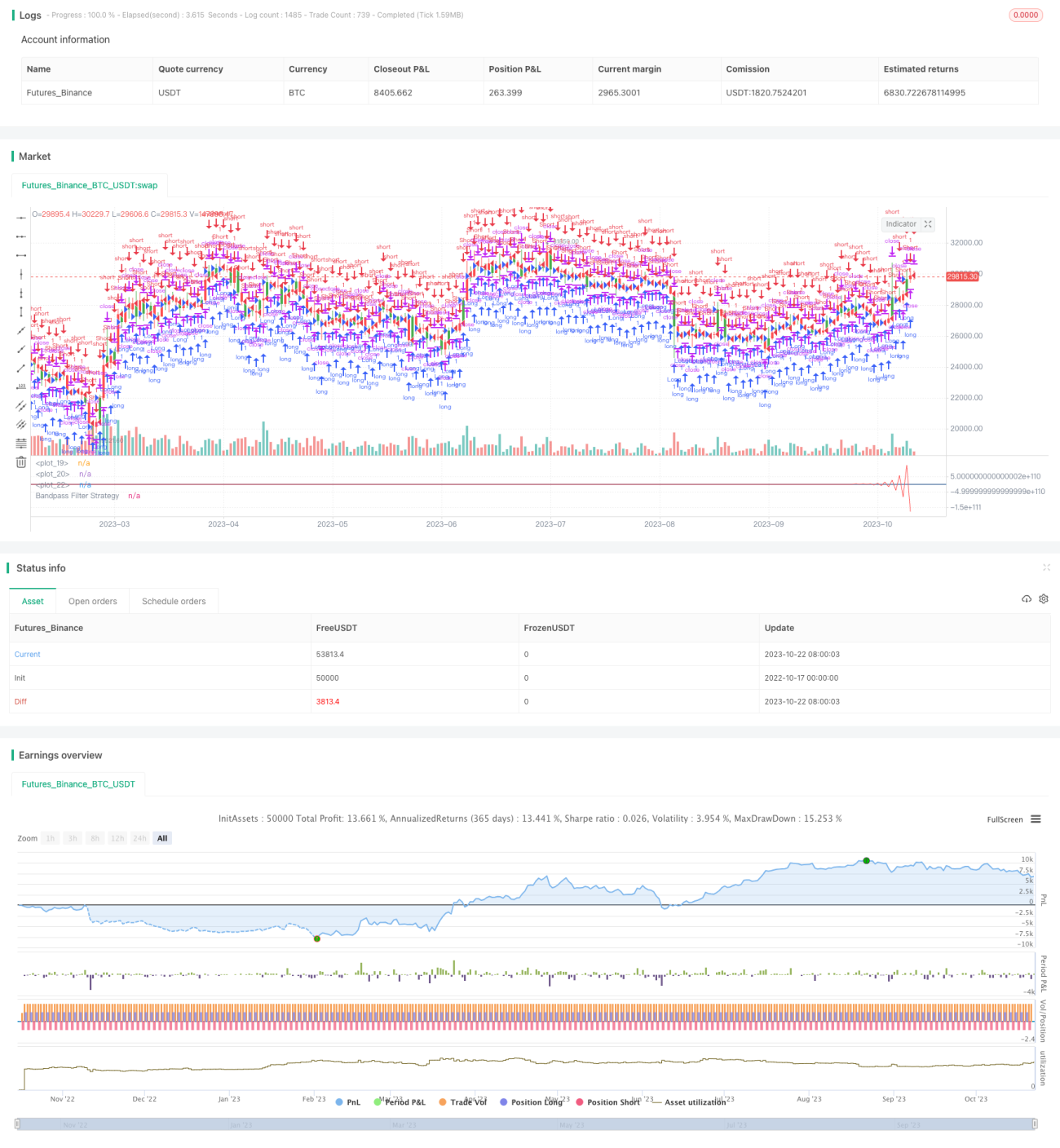

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/09/2018

// The related article is copyrighted material from- 1