RSI二重トレンドラインを活用したロング・ショート双方向取引戦略

概要

RSIダブルバンド発振線ロングショート双方向取引戦略は、RSIインジケーターを利用した双方向取引戦略です。この戦略は、RSIの買われ過ぎ・売られ過ぎの原理に加え、ダブルバンド設定と移動平均線の取引シグナルを組み合わせることで、効率的な双方向の建玉と決済を実現します。

戦略の原理

本戦略は主にRSIインジケーターの買われ過ぎ・売られ過ぎの原理に基づいて取引判断を行います。まずRSI値(vrsi)と、ダブルバンドの上限バンド(sn)および下限バンド(ln)を算出します。RSI値が下限バンド(ln)を下抜けた場合に買いシグナル、上限バンド(sn)を上抜けた場合に売りシグナルを生成します。

また、ローソク足の値動きの変化を検出し、さらに買い・売りシグナルを生成します。具体的には、ローソク足が下から上にブレイクした場合に買いシグナル(longLocic)、上から下にブレイクした場合に売りシグナル(shortLogic)を生成します。さらに、パラメータスイッチにより、買いのみ、売りのみ、またはシグナルの反転が可能です。

買い・売りシグナルが発生すると、シグナル回数をカウントし、建玉回数を制御します。パラメータで異なる追加ポジションのルールを設定できます。決済条件には、利確、損切り、トレーリングストップなどが含まれ、異なる利確・損切りのパーセンテージを設定できます。

要するに、本戦略はRSIインジケーター、移動平均線のクロス、統計的な追加ポジション、利確・損切りなど複数のテクニカル手法を統合し、自動化されたロング・ショート双方向取引を実現します。

戦略の優位性

- RSIの買われ過ぎ・売られ過ぎの原理を活用し、適切なタイミングで買い・売りポジションを構築。

- ダブルバンド設定により誤シグナルを防止。上限バンドは買いポジションの早期決済を防ぎ、下限バンドは売りポジションの早期決済を防ぐ。

- 移動平均線の取引シグナルで偽ブレイクをフィルタリング。価格が移動平均線をブレイクした場合のみシグナルを生成し、ダマシを回避。

- シグナル回数と追加ポジション回数を統計し、リスクを管理。

- 利確・損切りパーセンテージをカスタマイズ可能で、収益とリスクをコントロール。

- トレーリングストップにより利益をさらに確定。

- 買いのみ、売りのみ、またはシグナル反転が可能で、様々な市場環境に対応。

- 自動取引システムにより、人手によるコストを削減。

戦略のリスク

- RSIインジケーターは反転失敗のリスクがある。RSIが買われ過ぎ・売られ過ぎ領域に入っても必ずしも反転するとは限らない。

- 固定の利確・損切りポイントには約定リスクがある。設定が不適切だと早期の損切りや利確を招く可能性がある。

- テクニカル指標に依存するため、パラメータ最適化のリスクがある。指標パラメータの設定を誤ると戦略の効果に悪影響を及ぼす。

- 複数の条件が同時にトリガーされ、約定漏れのリスクがある。

- 自動取引システムには異常エラーのリスクがある。

これらのリスクに対しては、パラメータ設定の最適化、利確・損切り戦略の調整、流動性フィルタの追加、シグナル生成ロジックの改善、異常エラーモニタリングの追加などの改善が可能です。

戦略の最適化方向

- 異なる期間パラメータをテストし、RSIインジケーターパラメータを最適化。

- 異なる利確・損切りパーセンテージ設定をテスト。

- 出来高や収益率のフィルタを追加し、流動性不足を回避。

- シグナル生成ロジックを改善し、移動平均線クロス方式を改良。

- 複数期間のバックテストを追加し、安定性を検証。

- 他の指標を追加し、シグナル効果を最適化。

- ポジション管理戦略を導入。

- 異常エラーの監視を追加。

- 自動トレーリングストップロスアルゴリズムを最適化。

- 機械学習を導入し戦略を強化することも検討。

まとめ

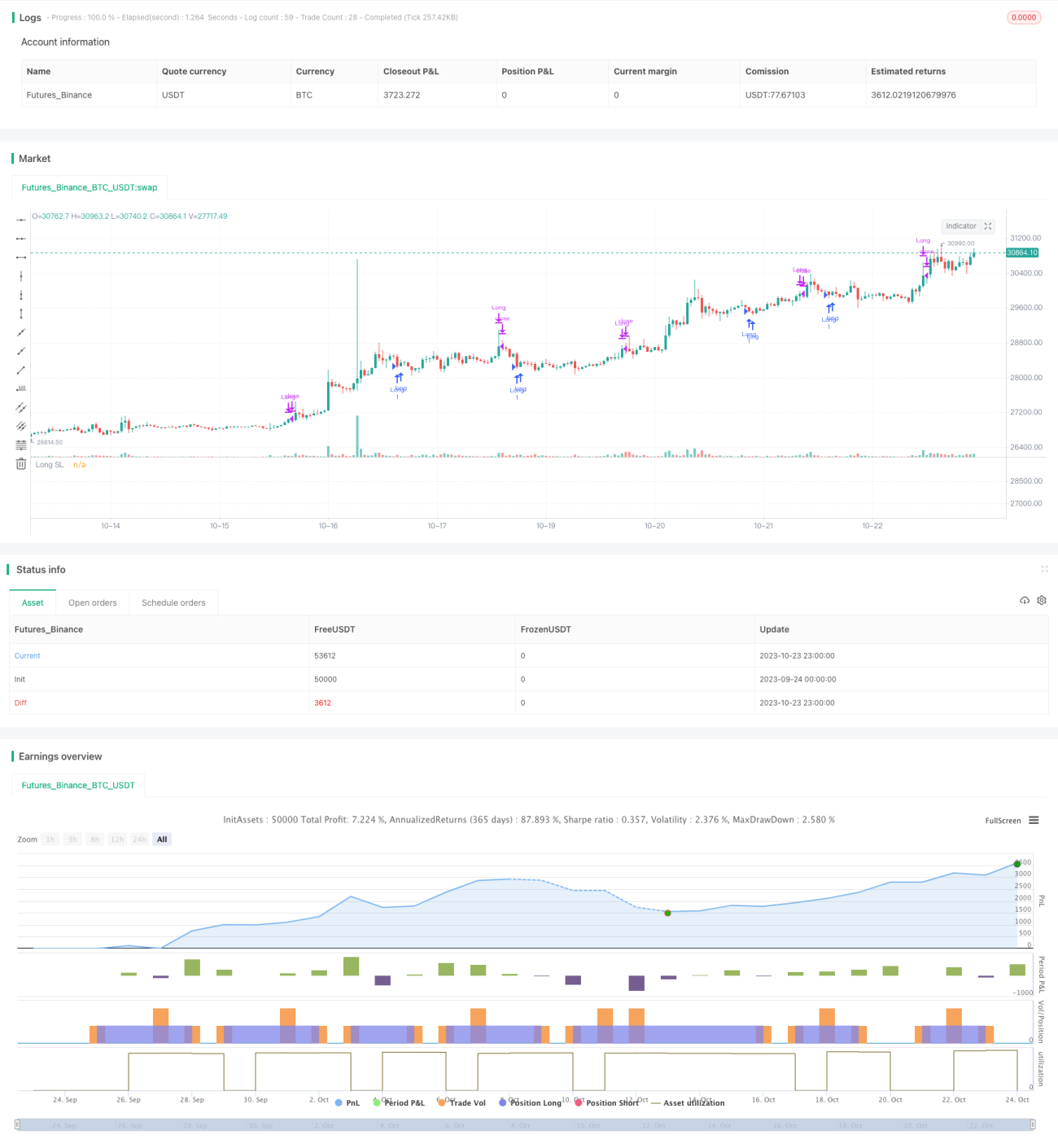

RSIダブルバンド発振線ロングショート双方向取引戦略は、RSIインジケーター、統計的な建玉・損切り原理などの複数のテクニカル手法を統合し、自動化された双方向取引を実現します。本戦略はカスタマイズ性が高く、ユーザーはニーズに応じてパラメータを調整し、様々な市場環境に適応できます。一方で、パラメータ設定の最適化、リスク管理戦略、シグナル生成ロジックなどの改善余地もあり、より安定性と信頼性を高めることができます。総じて、本戦略はユーザーに比較的高効率な定量取引ソリューションを提供します。

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1