多次元指標に基づく短期トレンド戦略

概要

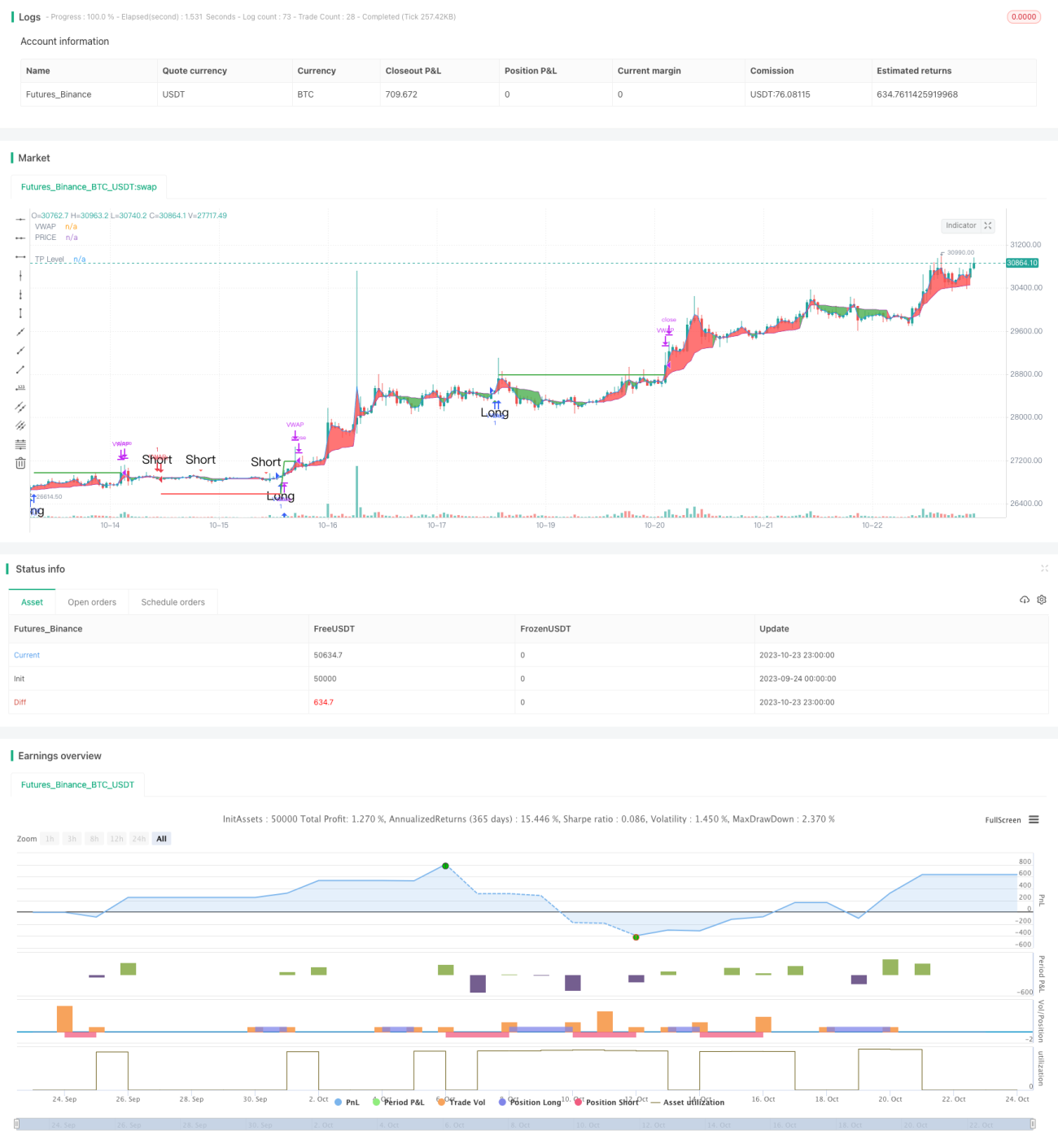

本戦略は、サポート・レジスタンスライン、移動平均線システム、オーバーボート・オーバーソールド指標という3つの異なる次元のテクニカル指標を融合し、それらの複合シグナルに基づいて短期トレンドの方向性を判断し、高い勝率を獲得することを目的としています。

戦略の原理

コードではまず、価格のサポート・レジスタンスラインを計算します。これには標準オシレーション軸とフィボナッチのサポート・レジスタンスラインが含まれ、チャート上に描画されます。価格がこれらの重要な水準をブレイクした際は、重要なトレンドシグナルとみなします。

次に、加重移動平均線VWAPと平均価格を計算し、それらのゴールデンクロスとデッドクロスのシグナルを判断します。これは中長期的なトレンド判断に該当します。

最後に、ストキャスティックRSI指標を計算し、そのゴールデンクロスとデッドクロスのシグナルを判断します。これはオーバーボート・オーバーソールド指標に該当します。

これら3つの次元の指標を総合し、サポート・レジスタンスライン、VWAP移動平均線、ストキャスティックRSIが同時に買いシグナルを発した場合にロングポジションを建て、3つが同時に売りシグナルを発した場合にショートポジションを建てます。

優位性分析

本戦略の最大の優位性は、3つの異なる次元の指標を組み合わせることで判断をより包括的かつ正確にし、勝率が高い点にあります。まずサポート・レジスタンスラインが大勢のトレンドを判断し、次にVWAPが中長期のトレンドを判断し、最後にストキャスティックRSIがオーバーボート・オーバーソールドの状況を判断します。3次元の指標が同時にシグナルを発することで、偽シグナルを大幅にフィルタリングし、エントリーの成功率を高めることができます。

また、本戦略には利確機能が組み込まれており、一定割合の利益を確定できるため、資金管理にも役立ちます。

リスク分析

本戦略の主なリスクは、ロング・ショートの判断が指標の同時シグナルに依存している点です。一部の指標が誤ったシグナルを発した場合、判断ミスにつながる可能性があります。例えば、ストキャスティックRSIがオーバーソールドシグナルを発しても、VWAPやサポート・レジスタンスラインが依然として強気と判断している場合、買いポイントを逃してエントリーできないことがあります。

また、指標のパラメータ設定が不適切な場合にもシグナル判断を誤る可能性があるため、繰り返しバックテストを行い最適なパラメータを見つける必要があります。

さらに、株式市場では短期的にブラックスワンイベントが発生し、指標が無効になることがあります。このリスクを防ぐには、ストップロス戦略を追加し、1回の損失が大きくなりすぎないようにすることが有効です。

最適化の方向性

本戦略は以下の点でさらに最適化が可能です。

- 出来高指標などの追加の指標を組み込み、トレンドの強弱を判断し、判断精度を向上させる。

- 機械学習モデルを追加し、多次元指標を学習させ、最適な取引戦略を自動的に見つける。

- 異なる銘柄のパラメータに応じて最適化し、適応型パラメータを設定する。

- ストップロス戦略を追加し、ドローダウンに応じてポジションサイズを調整し、リスク管理を強化する。

- ポートフォリオ最適化を行い、相関性の低い銘柄を組み合わせてポートフォリオ全体のドローダウンを低減する。

まとめ

本戦略は全体的に短期トレンド取引に非常に適しています。多次元の指標を用いて判断することで、多くのノイズを除去し、勝率が高くなります。ただし、指標が誤ったシグナルを発するリスクには注意が必要であり、継続的な最適化により、本戦略は効率的で安定した短期戦略となる可能性があります。

- 1