移動平均線のギャップ追跡戦略

本稿では、Noro氏が作成した「追跡移動平均ギャップ戦略」について詳細に分析します。この戦略は、終値と単純移動平均との乖離度合いを計算し、市場トレンドの転換点を判断することで、安値で買い、高値で売ることを目指します。

戦略の原理

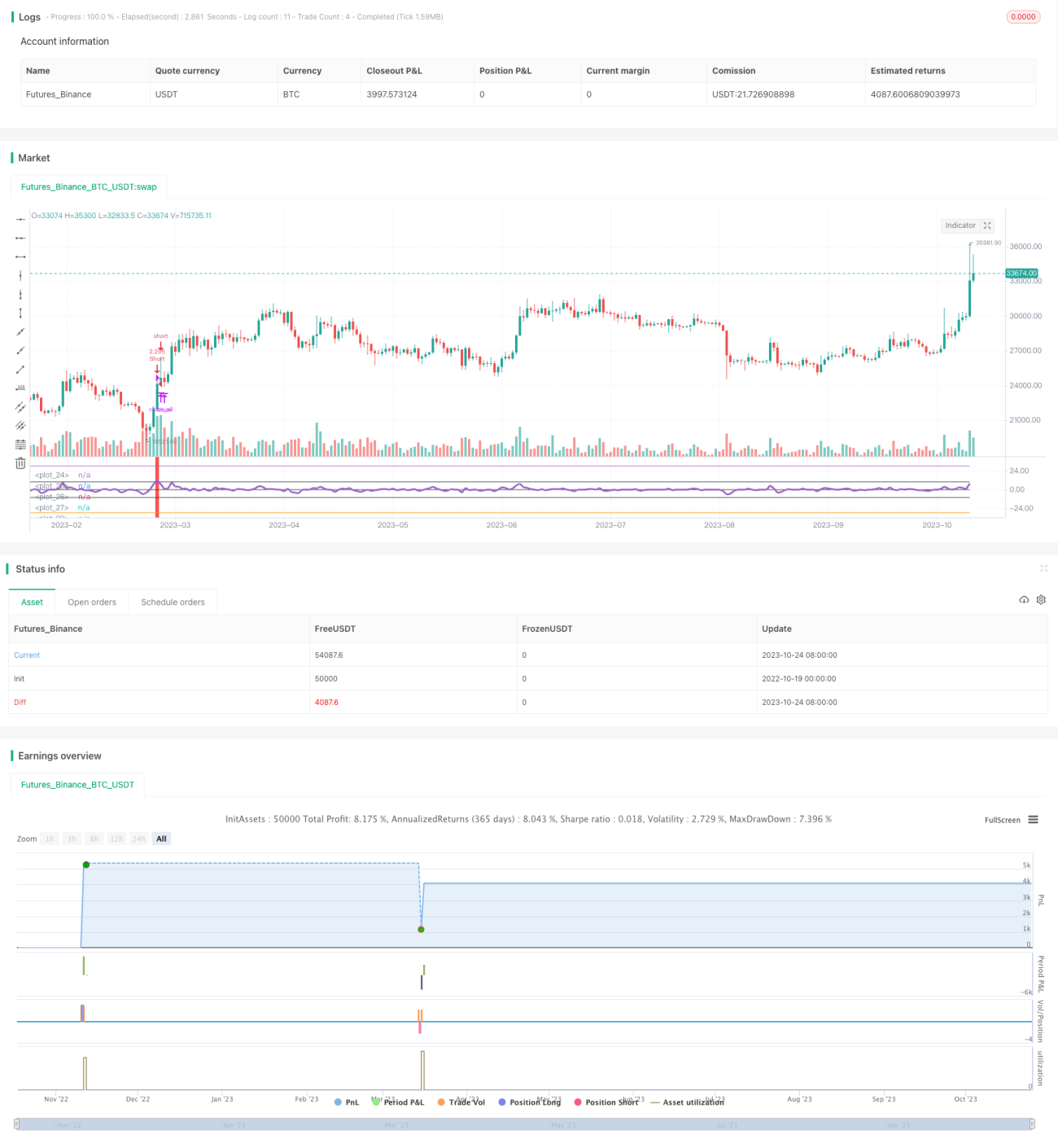

まず3日間の単純移動平均(sma)を計算します。次に、終値(close)とsmaの比率を計算し、そこから1を引いた指標indを算出します。indが事前に設定されたパラメータlimitを上抜けた場合、終値がsmaを明らかに上回っていることを示し、買い(ロング)を検討します。indが-limitを下抜けた場合、終値がsmaを大幅に下回っていることを示し、売り(ショート)を検討します。

また、0軸、limit軸、-limit軸も描画されます。ind指標が異なる領域にある場合、色分けされて表示され、判断を補助します。ind指標がlimitまたは-limitをクロスした場合、買いまたは売りのシグナルが発生したことを示します。

買いまたは売りのシグナルが発生すると、まず現在の反対方向のポジションを決済し、その後、新たに買いまたは売りのポジションを建てます。ind指標が0軸の範囲内に戻った場合、すべてのポジションを決済します。

戦略のメリット

-

ギャップ原理を利用し、価格が移動平均線から大きく乖離した際に逆張りを行います。これはトレンドフォローとは異なり、転換点を捉えることを狙います。

-

指標の軸線を描画することで、指標の位置やクロスを直感的に判断できます。

-

決済ロジックが最適化されており、現在のポジションを決済した後にのみ反対方向の新規ポジションを建てるため、不必要な逆方向のポジションを回避します。

-

取引時間範囲を設定し、不要なオーバーナイトポジションを避けます。

-

売り買い両方向の取引スイッチを設定でき、買いのみまたは売りのみの取引も可能です。

戦略のリスク

-

移動平均線を追跡する戦略は、損失取引が複数回発生しやすく、忍耐強いポジション保有が求められます。

-

移動平均線は判断指標として柔軟性に欠け、価格変動に迅速に対応できません。

-

事前設定パラメータlimitは静的に固定されており、異なる銘柄や市場環境に応じて調整が必要です。

-

移動平均線の追跡ではトレンド内の変動を識別できないため、ボラティリティ指標などと組み合わせて使用すべきです。

-

ストップロスや利確の設定、あるいはトレンド初期にのみギャップを捉えるなど、ポジション管理ルールの最適化が必要です。

戦略の最適化方向

-

SMAの期間など、さまざまなパラメータ設定をテストできます。また、指数移動平均などの適応型移動平均線を採用することも検討できます。

-

移動平均線の方向や角度などの判定を追加し、レンジ相場での無駄な取引を避けられます。

-

ボラティリティ指標(例:ボリンジャーバンド)と組み合わせ、ボラティリティが拡大した際には取引を一時停止する方法が考えられます。

-

固定数量での建て玉、段階的な増し玉、資金管理など、ポジション管理ルールを設定できます。

-

ストップロス・利確ラインを設定するか、一定割合の損失が発生した場合に新規注文を停止し、一取引あたりのリスクをコントロールできます。

まとめ

本稿では、Noro氏が作成した追跡移動平均ギャップ戦略について詳細に分析しました。本戦略は、価格が移動平均線から乖離する特性を利用し、指標軸線と色分けを設計してエントリータイミングを判断します。同時に決済順序のロジックを最適化し、取引時間範囲を設定しています。しかし、本戦略には移動平均線追跡に固有の欠点があり、パラメータ設定、ストップロスルール、他の指標との組み合わせなどをさらに最適化し、安定性を高める必要があります。

- 1