広義のサポート/レジスタンスに基づくリバーサルトレーディング戦略

概要

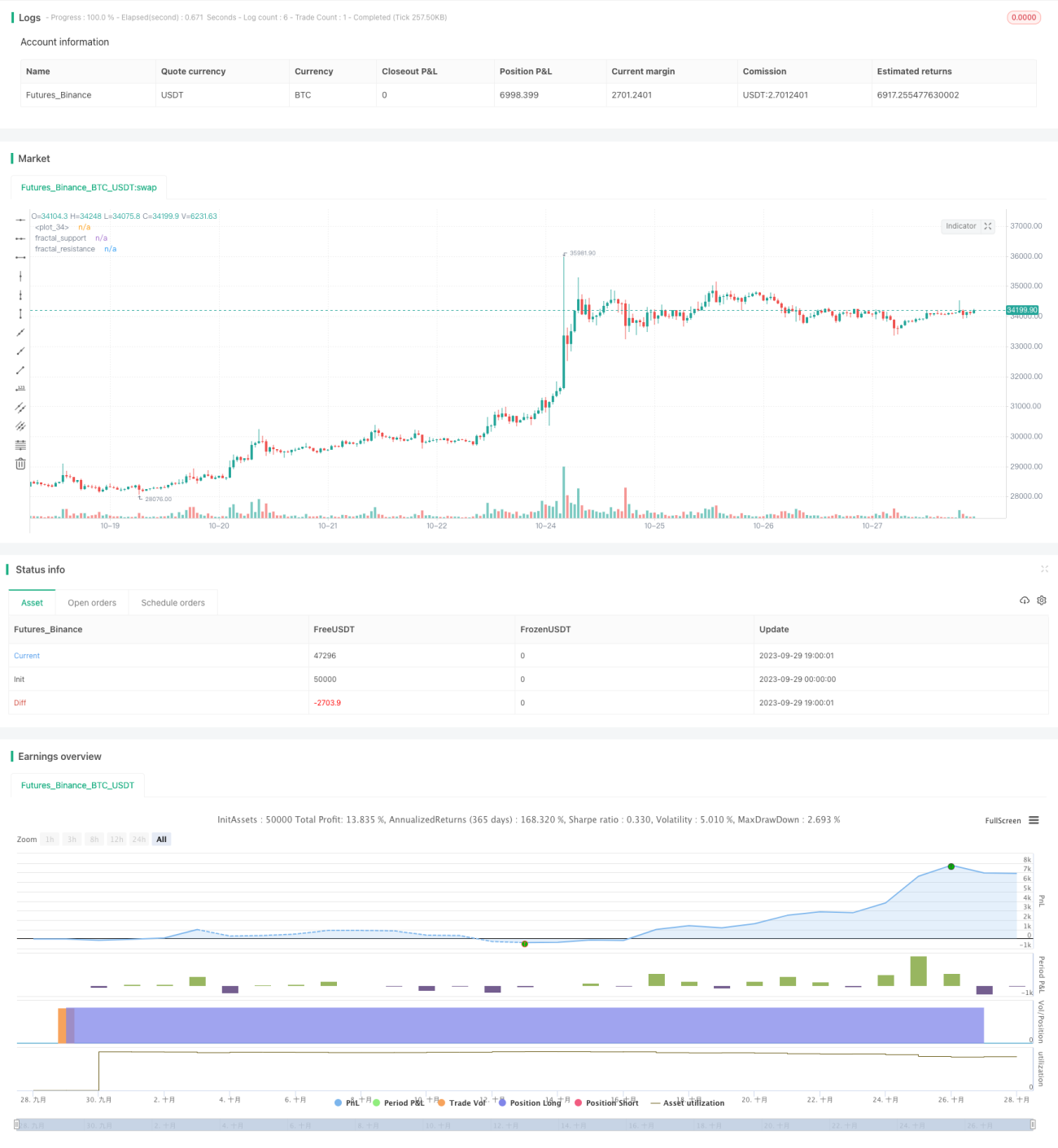

本戦略は、指標の多空因子に基づいて逆張り取引を行い、同時に目標利益点を設定します。多空因子の核心は、取引量に基づく拡張形態「一般的なサポート/レジスタンス」であり、高い取引量とボラティリティを持つ銘柄に適しています。戦略の利点は、中短期的な大きなトレンド反転の機会を捉え、迅速に利益を得られることですが、逆にポジションが拘束されるリスクもあります。

戦略の原理

-

取引量に基づく「一般的なサポート/レジスタンス」による多空因子の識別

- ローソク足のパターンを使用して古典的なサポート/レジスタンスを識別し、大きな取引量で偽のブレイクアウトをフィルタリングします。

- 一般的なサポート/レジスタンスは、古典的なパターンよりも包含性が高い。

- 一般的なサポートのブレイクアウトは強気因子シグナル、一般的なレジスタンスのブレイクアウトは弱気因子シグナル。

-

逆張り取引

- 因子シグナルが発生した後、逆方向の取引を行う。

- 既にポジションを保有している場合、逆方向にポジションを減らすか、新規に逆方向のポジションを建てる。

-

利益目標の設定

- ATRに基づいてストップロスを設定。

- 1R/2R/3Rなど複数の目標利益点を設定。

- 異なる利益目標に達したら、段階的にポジションを減らす。

優位性分析

-

中短期的な大きな反転を捉えられる

サポート/レジスタンスのブレイクアウトは強いトレンド反転シグナルを表し、一定の信頼性があり、中短期的な大きな反転を捉えることができる。 -

迅速な利益獲得、ドローダウンが小さい

ストップロスと複数の利益目標の設定により、迅速に利益を得られ、個別銘柄のドローダウンを抑えることができる。 -

大量の機関資金と高いボラティリティを持つ銘柄に適している

本戦略は取引量指標に依存するため、トレンドを支える十分な機関資金の流入が必要。同時に利益を実現するための一定のボラティリティも必要。

リスク分析

-

レンジ相場での足止めリスク

相場がレンジの場合、ストップロスで退出してから逆方向にエントリーする操作により、頻繁に足止めされる可能性がある。 -

サポート/レジスタンスの無効化リスク

一般的なサポート/レジスタンスは絶対的な信頼性はなく、失敗したテストによる反転の確率が存在する。 -

片方向ポジション保有リスク

純粋な逆張り戦略であり、トレンドフォローを考慮しないため、大きな方向性の機会を逃す可能性がある。 -

リスク管理面

- 逆張り取引の因子条件をやや緩和し、全てのブレイクアウトで反転する必要はない。

- 他の指標(例:出来高と価格のダイバージェンス)を組み合わせてフィルタリングできる。

- ストップロス戦略を最適化し、足止めされる確率を低減できる。

最適化の方向性

-

パラメータの口径を最適化

一般的なサポート/レジスタンスのパラメータを最適化し、より信頼性の高い因子を識別する。 -

利益戦略の最適化

より多くの段階的な利益目標を追加したり、固定されていない目標利益を採用できる。 -

ストップロス戦略の最適化

ATRパラメータを調整するか、isticsストップロスを使用して、不必要な激しいストップロスによる取引コストを削減する。 -

トレンドや他の因子との組み合わせ

移動平均線などのトレンド判断を導入し、トレンドとの激しい対抗を避ける。また、他の補助因子を導入できる。

まとめ

本戦略の核心は、逆張り取引を利用して中短期的な大きな変動を捉えることです。戦略の考え方はシンプルかつ直接的で、パラメータ調整により実運用で良好な結果を得られます。しかし、逆張り戦略は積極的であり、一定のドローダウンと足止めリスクが存在するため、ストップロスと利益戦略をさらに最適化し、トレンド判断を適宜組み合わせて不必要な損失を減らす必要があります。

- 1