MACD 終値中央値タートルハイブリッド戦略

概要

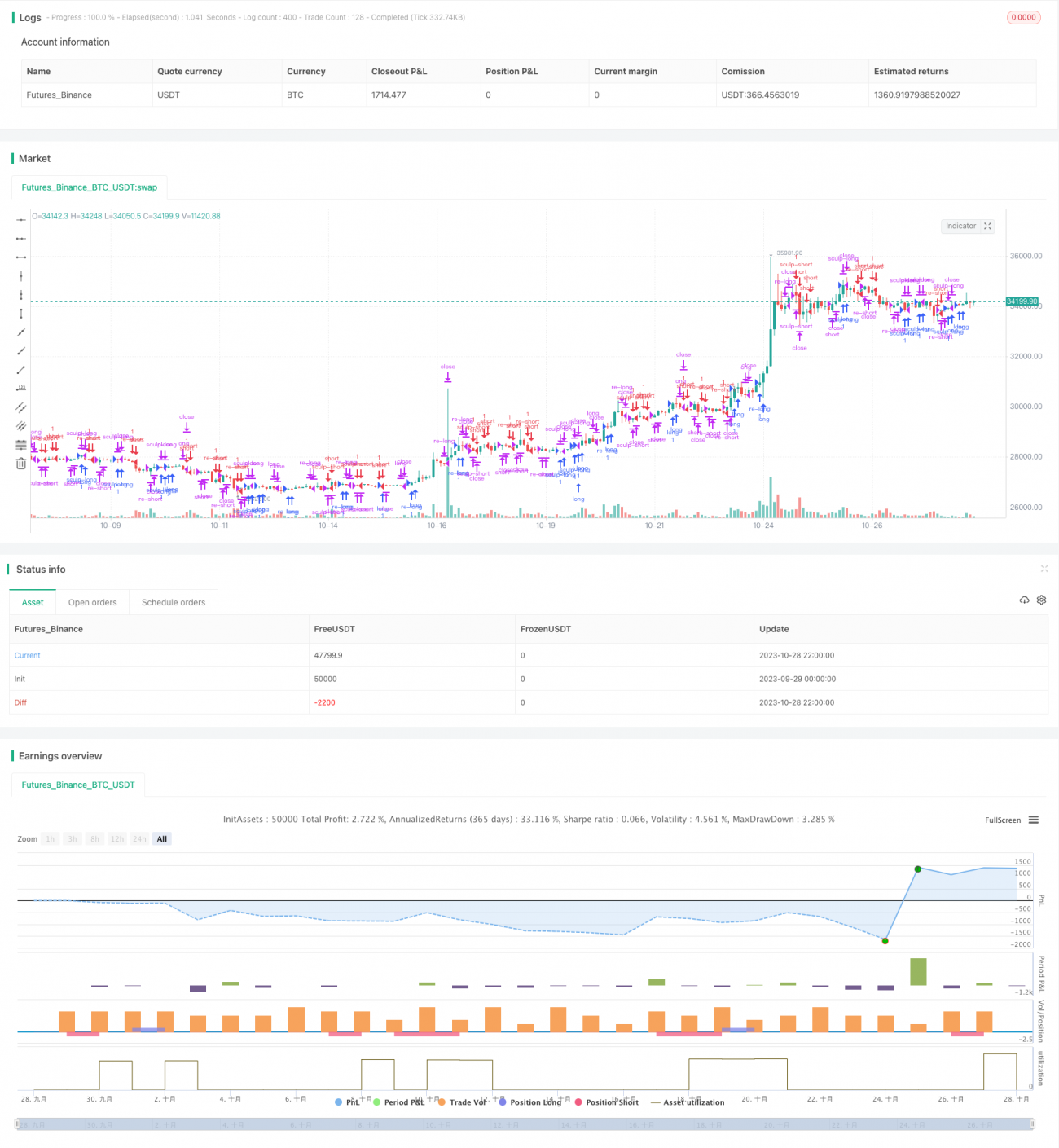

本戦略は、MACD指標のゴールデンクロス・デッドクロスシグナル、ローソク足の終値と中央線の関係、価格のレンジ相場の特徴を総合的に活用して、エントリーとエグジットのタイミングを判断します。同時に、再エントリーと修正エントリーのメカニズムを設定することで、より多くの取引機会を得るとともにリスクをコントロールし、安定した収益を実現します。

戦略の原理

本戦略は主に以下の点に基づいています。

-

MACDの分析における短期線と長期線のゴールデンクロス・デッドクロスを利用して、強気相場と弱気相場、および具体的なエントリーポイントを判断します。

-

ローソク足の終値と中央線の関係を利用して、強気・弱気トレンドが終了したかどうか、およびエグジットポイントを判断します。

-

再エントリーメカニズムを設定し、MACDによる今回の相場が終了した後も、引き続きトレンドに適合する場合に再度エントリーすることで、利益獲得の機会を増やします。

-

修正エントリーメカニズムを設定し、価格が部分的に調整したもののまだ反転していない場合にポジションを追加します。これはトレンド内の調整に該当します。

-

上記を総合して、動的にポジションを調整し、トレンドの中で可能な限り多くの利益を獲得し、トレンド終了時には迅速に離脱します。

具体的には、戦略はまずMACDの短期線と長期線がゴールデンクロスまたはデッドクロスを起こしているかを判断し、ゴールデンクロスなら買い、デッドクロスなら売りを行います。次に、ローソク足の終値が中央線にタッチしているかを判断し、タッチした場合はトレンド終了とみなしてポジションをクローズします。

さらに、戦略は再エントリーメカニズムも設定しています。最初の方向のトレンドが終了した後も、MACDが同じ方向のシグナルを継続して示している場合、戦略は再度ポジションを開きトレンドを追跡します。また、修正エントリーメカニズムも設定しており、価格が小幅に調整したものの全面的に反転していない場合、戦略は適切にポジションを追加します。これはトレンド中の正常な調整行動に該当します。

これらの設定により、戦略はトレンドの中で動的にポジションを調整し、エントリーとエグジットの回数が増え、リスクをコントロールしつつより高いリターンを得ることができます。

戦略の優位性

本戦略は複数の指標を総合的に活用しており、以下の主な優位性があります。

-

MACDはトレンドと反転点を識別し、具体的なエントリーポイントを確定できます。

-

終値と中央線の関係の判断により、トレンド終了を正確に判断できます。

-

再エントリーメカニズムによりポジションを開く回数が増え、資金の利用効率が向上します。

-

修正エントリーメカニズムによりタイムリーにポジションを追加し、トレンド相場を十分に捉えることができます。

-

戦略の取引頻度は高いもののリスクはコントロール可能で、高いプロフィットファクターを得やすくなります。

-

各パラメータは調整可能で、異なる銘柄や相場に合わせて最適化できます。

-

戦略の考え方は明確で理解しやすく、コード記述はシンプルであり、実運用も容易です。

-

バックテストのデータは十分で信頼性が高く、実運用での効果検証が容易です。

戦略のリスク

本戦略には以下の主なリスクも存在します。

-

MACDが誤ったシグナルを発する可能性があり、他の指標と組み合わせて検証する必要があります。

-

大きなレベルのストップロス設定が小さすぎると、特大相場で振り落とされる可能性があります。

-

再エントリーと修正エントリーにより取引頻度が増えるため、資金利用効率をコントロールする必要があります。

-

リバウンド相場での修正エントリーは大きな損失をもたらす可能性があります。

-

取引銘柄とパラメータ設定は最適化が必要であり、すべての銘柄に適用できるわけではありません。

-

継続的なバックテストと最適化が必要で、市場に応じてパラメータを調整する必要があります。

-

実運用ではスリッページコストの影響を考慮する必要があります。

対応するリスク管理策としては、ストップロスとテイクプロフィットを設定して1回の損失を限定すること、資金利用率を評価し適切な現金準備金を維持すること、銘柄に適したパラメータの組み合わせを選択してバックテストを行うこと、相場特性の変化を継続的に監視してパラメータを最適化すること、バックテストとシミュレーションでスリッページコストの影響を考慮することなどが挙げられます。

戦略の最適化方向

本戦略は以下の点からさらに最適化できます。

-

他の指標(KDJ指標など)と組み合わせてシグナルを検証し、シグナルの正確性を高める。

-

適応型の動的なストップロス・テイクプロフィット基準を設定する。

-

再エントリーと修正エントリーの条件ロジックを最適化する。

-

銘柄ごとにパラメータを最適化し、最適なパラメータの組み合わせを設定する。

-

資金利用比率を最適化し、再エントリーと修正エントリーの資金制限を設定する。

-

出来高指標と組み合わせて、リバウンド相場での追加入札による損失を回避する。

-

エグジットメカニズム(移動ストップロスなど)を追加する。

-

戦略を取引ロボットとしてパッケージ化し、自動売買を実現することを検討する。

-

実運用での考慮要因(スリッページコストなど)を追加する。

これらの最適化により、戦略の安定性、適応性、自動化の度合い、および実運用での効果をさらに向上させることができます。

まとめ

本戦略は、MACD指標の取引シグナル、ローソク足終値の分析、および複数回のエントリーメカニズムを統合して活用し、トレンドを捉えながらリスクをコントロールする、効率の高い定量取引戦略の考え方です。本戦略は取引頻度が高く、資金利用率が良く、実装難易度が低いなどの利点がありますが、リスク管理と戦略の最適化にも注意を払う必要があり、実用的な価値と拡張性が高いです。ロボット技術と組み合わせて自動化を実現できれば、非常に実用的な定量取引ソリューションとなり得ます。

- 1