ランダムRSIとEMAに基づく自律型買いエントリーのスキャルパー戦略

1

Follow

1802

Followers

概要

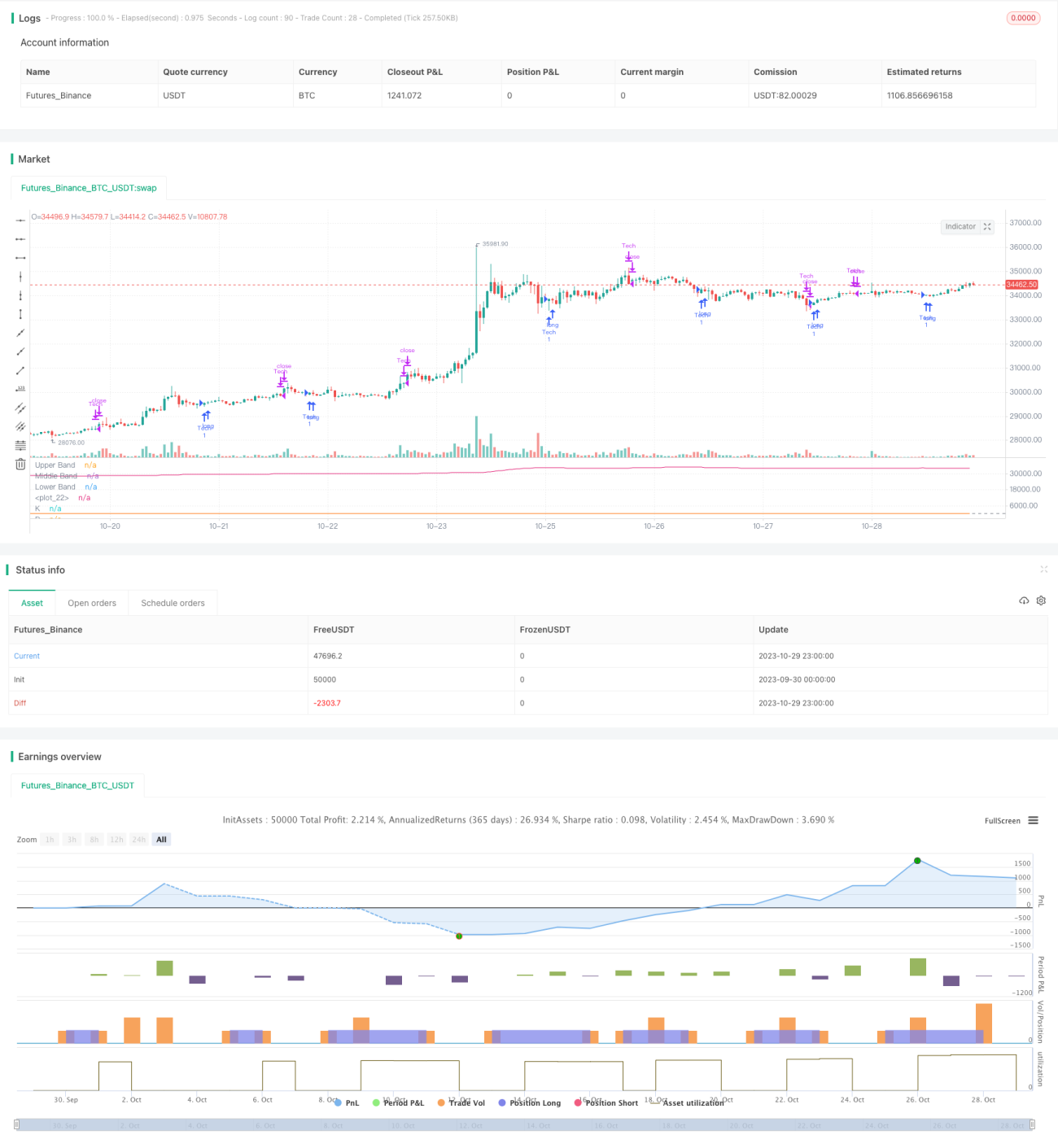

本戦略は、確率的RSI(ストキャスティクスRSI)と指数移動平均(EMA)指標に基づく、自律的なBuy&Hold型のスカルピング戦略を実現するものです。5分足のチャートに対応し、BTC向けに最適化されています。戦略の目標は、横ばい相場または大幅な下落がない状況で、できるだけ多くのコインを保有することです。

戦略の原理

この戦略では、RSI指標を用いて買われすぎ・売られすぎの領域を判断し、確率的RSI指標のK値とD値の関係から買いシグナルと売りシグナルを生成します。

確率的RSIのKラインが20を下回った場合を売られすぎと見なし、KラインがDラインを上回ったときに買いシグナルが発生します。その後、以下の3つの条件で売りを判断します:1) 価格が1%上昇した後にEMAが反転した場合、2) 確率的RSI指標のKラインがDラインを下回った場合、3) ストップロス価格がエントリー価格の98.5%に達した場合。

また、短期EMAが上昇後に下方反転した場合も売りシグナルと判断します。

戦略の優位性

- 確率的RSI指標を用いて買いタイミングを判断することで、偽のブレイクアウトを効果的にフィルタリングできます。

- EMA指標と組み合わせることで、トレンド変化のタイミングをより正確に判断できます。

- ストップロスを採用することで、損失を効果的に抑えられます。

- できるだけ多くのコインを保有することで、取引頻度を減らし、手数料を低減できます。

戦略のリスク

- RSI指標が偽のシグナルを発する可能性があります。RSIパラメータを適宜調整することで最適化できます。

- ストップロス価格が小さすぎると損失が拡大する恐れがあります。ストップロスの幅を適宜調整してください。

- EMA指標のパラメータ設定が不適切だと、トレンド変化のタイミングを見逃す可能性があります。異なるEMA期間のパラメータをテストすることをお勧めします。

最適化の方向性

- 異なるRSIおよび確率的RSIのパラメータ設定をテストし、最適なパラメータの組み合わせを探す。

- 異なるストップロスの幅を試し、損失防止と利益の減少のバランスを取る。

- EMAの短期・長期の組み合わせをテストし、トレンド変化を判断する最適なパラメータを見つける。

- 他の指標を追加して、売買タイミングの判断精度を高めることも検討する。

まとめ

本戦略は、確率的RSIやEMAなど複数の指標の利点を統合し、堅実な方法で買い・売りのタイミングを判断します。パラメータの最適化とリスク管理により、戦略の収益性と安定性をさらに向上させることができます。総じて、本戦略のロジックは合理的であり、実運用での検証と最適化に値します。

Source

Pine

/*backtest

start: 2023-09-30 00:00:00

end: 2023-10-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Stochastic RSI W Auto Buy Scalper Scirpt III ", shorttitle="Stoch RSI_III", format=format.price, precision=2)

smoothK = input.int(3, "K", minval=1)

smoothD = input.int(3, "D", minval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1