低点スキャンスマートトラッキング法

概要

低点スキャンスマートトラッキング法は、非反転型の外国為替取引戦略です。低点スキャナーを使用して最安値を見つけ、Hull移動平均線を組み合わせて取引シグナルを判断することで、高い勝率を実現できます。

原理分析

本戦略はまず低点スキャナーを使用して最安値を探索します。低点スキャナーは価格と出来高のRSI値を計算し、そのRSI値をWMA曲線と比較することで、RSI値がWMAを下回った時を最安値と判定します。

次に、戦略はHull移動平均線を使用して取引シグナルを判断します。異なる期間の2つのHull MAを計算し、短期Hull MAが長期Hull MAを上抜けた時に買い、下抜けた時に売りとします。

最後に、戦略は最安値スキャンとHull MAのシグナルを組み合わせ、低点スキャナーが最安値シグナルを出力した場合にのみ、Hull MAの取引シグナルを発行し、エントリー戦略を構成します。

これにより、市場の最安値を特定してからトレンドを追跡することで、誤ったエントリータイミングを効果的に回避し、取引システムの勝率を向上させます。

優位性分析

低点スキャンスマートトラッキング法の主な優位性は以下の通りです:

-

低点スキャナーを使用することで、市場の最安値を正確に識別でき、高値での買いによる損失を回避できます。

-

Hull MAは優れたトレンド追跡指標であり、流れに乗って大きな相場を捉えることができます。

-

低点スキャンとHull MAを相互検証することで、大量のノイズを除去し、偽シグナルを低減できます。

-

段階的ストップロス決済メカニズムを採用することで、利益を最大限に確定し、利益の吐き出しを回避できます。

-

本戦略は非反転指標駆動型であり、過去データを操作せず、信頼性が高く現実的です。

リスク分析

本戦略には主に以下のリスクが存在します:

-

低点スキャナーが一部の最安値を見逃し、取引機会を逃す可能性があります。パラメータを適切に調整し、スキャン範囲を拡大することで対応できます。

-

相場が急激に反転し、ストップロスが執行される可能性があります。ストップロス範囲を適度に緩和し、ポジション規模を適切に管理することで対応できます。

-

パラメータ設定が不適切だと、取引シグナルが過多または過少になる可能性があります。何度も最適化を繰り返し、最適なパラメータの組み合わせを見つける必要があります。

-

本戦略はトレンドが明確な外国為替銘柄にのみ適用可能であり、レンジ相場やもみ合い相場の取引には適していません。

最適化の方向性

本戦略は以下の点から最適化できます:

-

低点スキャナーのパラメータを最適化し、最安値をより正確に識別できるようにします。

-

Hull MAのパラメータを最適化し、トレンドをより正確に追跡できるようにします。

-

MACD、KDJなどの他のインジケーターによるフィルターを追加し、シグナルの信頼性を高めます。

-

機械学習モデルの予測結果を追加し、取引シグナルの判断を補助します。

-

ストップロスメカニズムを最適化し、市場の変動に応じて動的に調整できるようにします。

-

ポジション管理戦略を最適化し、資金管理ルールに従ってシステムが動的にポジションを調整できるようにします。

まとめ

低点スキャンスマートトラッキング法は、高い勝率を持つ非反転型の外国為替取引戦略です。市場の最安値を正確に識別し、トレンドが明確なときに流れに乗ってエントリーし、段階的ストップロスで利益を確定します。本戦略は最適化の余地が大きく、多方面から改良することで、強力な自動売買システムへと発展させることができます。

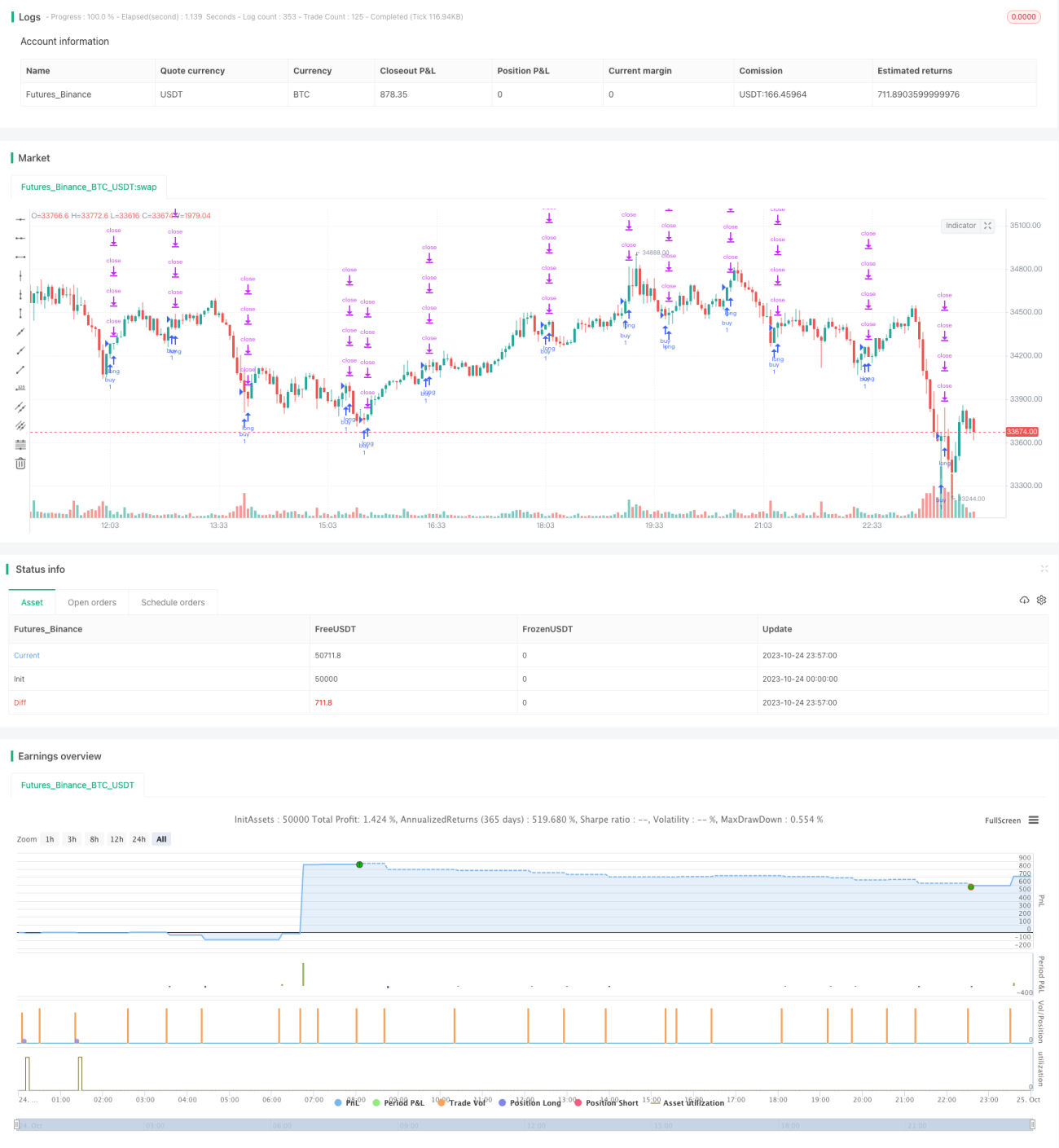

/*backtest

start: 2023-10-24 00:00:00

end: 2023-10-25 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © theCrypster 2020

//@version=4

// strategy(title = "Low Scanner Forex strategy", overlay = false, pyramiding=1,initial_capital = 1000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0)- 1