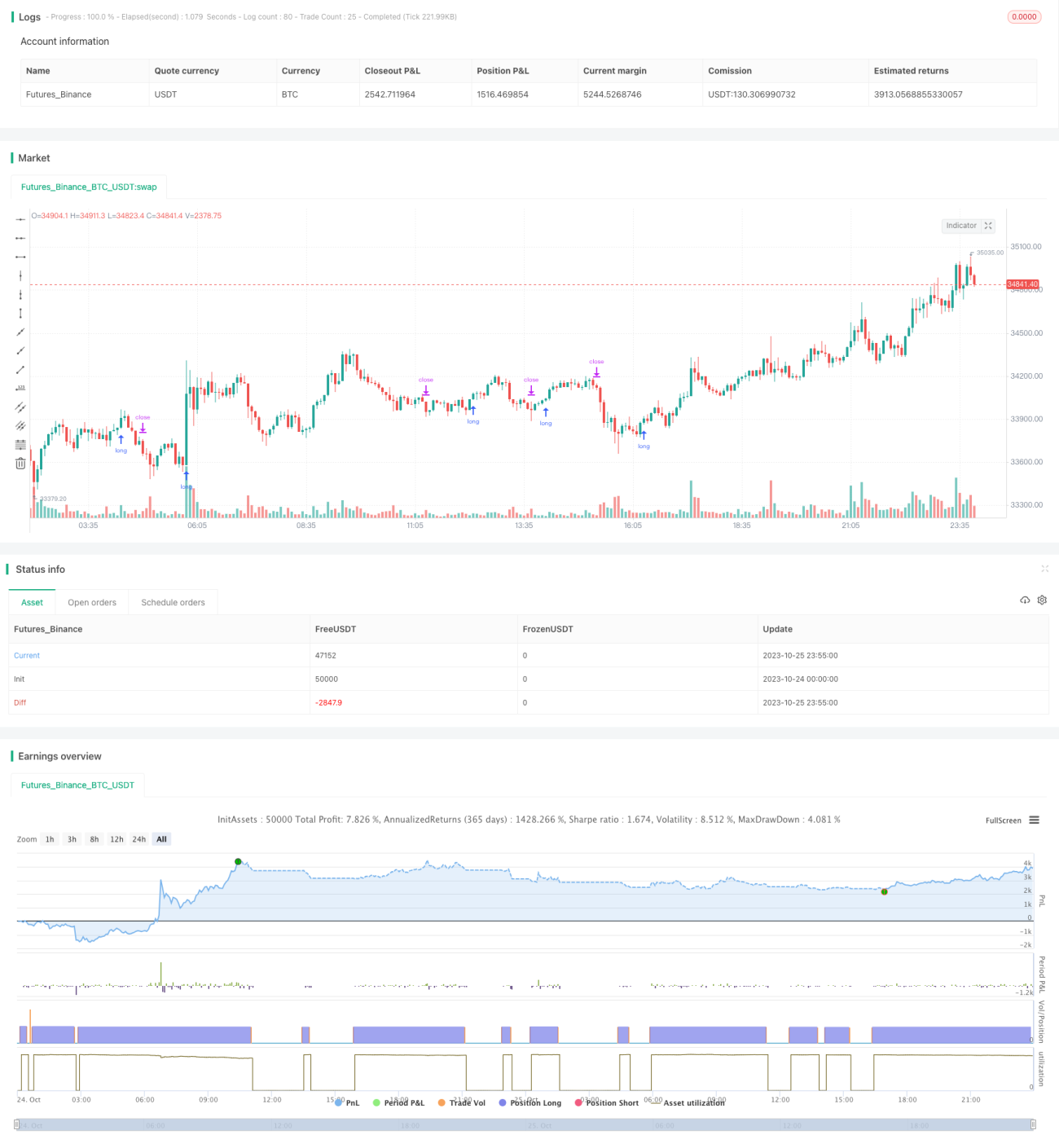

ブレイクアウト・トレンドフォロワーV2

概要

本戦略は、私が以前に開発した別のブレイクアウトトレンド追従戦略のバリエーションです。別の戦略では、移動平均線を取引のフィルターとして使用できます(つまり、価格が移動平均線を下回っている場合、買いは行われません)。より高い時間枠のトレンドを検出するツールを作成した後、それが移動平均線よりも優れたフィルターになる可能性があるかどうかを検証したくなりました。

そのため、本戦略では、より高い時間枠のトレンド(つまり、より高い高値とより高い安値があるかどうか?もしそうなら上昇トレンド)を確認できます。トレンドの方向にのみポジションを持ちます。フィルターとして最大2つのトレンドを選択できます。各トレンド方向はチャート上のテーブルに表示され、参照しやすくなっています。現在のサポートラインとレジスタンスラインはチャート上に描画され、いつ現在の時間枠のトレンドやより高いレベルのトレンドがブレイクする可能性があるかを確認できます。

この戦略は、他の戦略と比較して全体的なパフォーマンスはあまり良くないことが多いですが、取引をより厳選する傾向があるようです。より高い勝率とより良いプロフィットファクターを示します。取引数は少なく、純利益もあまり良くありません。

戦略原理

本戦略の核となるロジックは、より高い時間枠のサポートラインとレジスタンスラインのブレイクを使用してトレンドを識別し、トレンド方向に従って取引を行うことです。

具体的には、以下の手順で実現します。

-

現在の時間枠(例:1時間足)のサポートラインとレジスタンスラインを計算します。これは、一定期間内の最高値と最安値を見つけることによって行われます。

-

1つ以上のより高い時間枠(例:4時間足と日足)のサポートラインとレジスタンスラインを計算します。これには現在の時間枠と同じロジックを使用します。

-

これらのサポートラインとレジスタンスラインの水平線をチャート上に描画します。価格がこれらのラインをブレイクすると、より高い時間枠のトレンドが変化します。

-

価格がこれらの重要な水準をブレイクするかどうかに基づいてトレンド方向を判定します。価格が前回の高値を上回った場合、上昇トレンドと見なします。前回の安値を下回った場合、下降トレンドと見なします。

-

ユーザーが1つ以上のより高い時間枠のトレンドをフィルター条件として選択できるようにします。つまり、現在の時間枠のトレンド方向がより高い時間枠のトレンド方向と一致する場合にのみ、取引を検討します。

-

トレンドフィルター条件を満たし、現在の価格が重要な水準をブレイクしたときに、買いまたは売りを実行します。ストップロス水準は、以前の重要なサポートまたはレジスタンスラインに設定されます。

-

価格が動くにつれて、新しい高値または安値が形成された場合、ストップを新しい安値(または高値)に移動し、利益を確保しトレンドに追随します。

-

ストップロスがトリガーされるか、重要なサポート/レジスタンスラインがブレイクされたときにポジションをクローズします。

このようなマルチタイムフレームのトレンド分析により、本戦略は比較的強いトレンド方向でのみ取引を行い、勝率を高めようとします。同時に、重要な水準は明確なエントリーとストップロスのシグナルを提供します。

戦略のメリット

-

複数の時間枠を使用してトレンドを判断するため、より強いトレンド方向を正確に識別でき、市場ノイズによる誤った方向への取引を避けることができます。

-

主要なトレンド方向でのみ取引するため、勝率を大幅に向上させることができます。テスト結果によると、単純な移動平均線フィルターと比較して、本戦略はより高い勝率とより良いリスクリワード比率を示します。

-

サポートラインとレジスタンスラインは明確なエントリーとストップロスの水準を提供します。特定のエントリーポイントの選択に悩む必要はありません。

-

トレンドの進行に合わせてストップロスを調整することで、利益を最大限に確保できます。

-

戦略ロジックはシンプルで明確であり、理解と改良が容易です。

戦略のリスク

-

長期的なラインのトレンド判断に依存しているため、トレンド反転時にポジションが逆方向に動くリスクがあります。トレンド判断の時間枠を適切に短縮するか、他の指標を補助的に使用する必要があります。

-

ファンダメンタル要因を考慮していないため、重要なイベント発生時には株価と乖離する可能性があります。決算発表やニュースイベントなどのフィルター条件を追加できます。

-

ポジションサイズコントロールが設定されていません。口座資金規模やボラティリティなどに基づいてポジションサイズを設定することができます。

-

バックテストの時間範囲が限られています。バックテスト期間を拡大し、さまざまな市場環境でのロバスト性をテストする必要があります。

-

取引コストの影響を考慮していません。実取引では、実際の取引コストに基づいて戦略パラメータを調整する必要があります。

-

長期的な取引のみを考慮しています。他の戦略と組み合わせて短期取引シグナルを開発し、マルチタイムフレームの裁定取引を実現できます。

戦略の最適化方向

-

フィルター条件の追加:

-

ファンダメンタルデータ(決算、ニュースイベントなど)

-

インジケーター(出来高、ATRストップロスなど)

-

-

パラメータの最適化:

-

サポート/レジスタンスラインの計算期間の調整

-

トレンド判断の時間枠の調整

-

-

戦略範囲の拡大:

-

短期取引戦略の開発

-

空売り機会の検討

-

マルチ銘柄裁定取引

-

-

リスク管理の向上:

-

ボラティリティと資金規模に基づくポジションサイズの最適化

-

ストップロス戦略の最適化(トレーリングストップ、注文ストップなど)

-

リスク報奨メカニズムの導入

-

-

実行ロジックの最適化:

-

エントリータイミングの選択の改善

-

部分的なポジションエントリーの検討

-

ストップロス移動戦略の最適化

-

まとめ

本戦略は、マルチタイムフレームのトレンド分析を通じて、比較的堅牢なブレイクアウトシステムを設計しています。単純な移動平均線などのインジケーターフィルターと比較して、より高い勝率とリスクリワード比率を示します。しかし、リスク管理メカニズムが不完全である、ファンダメンタル要因を考慮していないなど、改善すべき点もあります。さらに最適化すれば、非常に実用的なトレンド追従戦略になり得ます。全体的に見て、本戦略は合理的に設計されており、マルチタイムフレーム分析によって判断精度を高めているため、さらなる研究と応用の価値があります。

- 1