日内反転トレンド追跡戦略

1

Follow

1802

Followers

概要

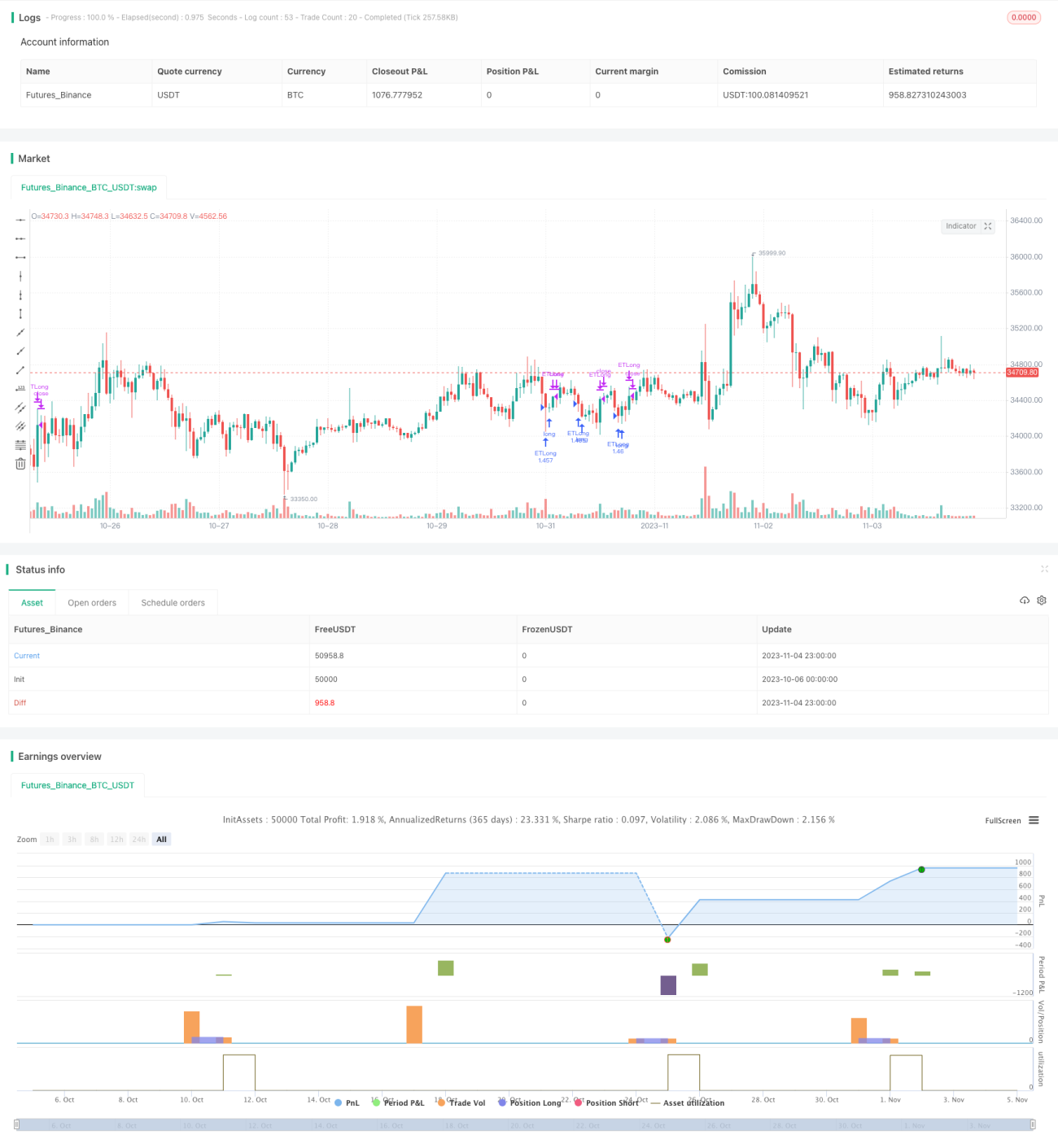

本戦略の主な考え方は、月曜日の取引時間中に、その日の逆転相場を利用してトレンドを追跡し、利益を上げることです。

原理

本戦略の核となるロジックは次の通りです。

- 月曜日の取引日かどうかを判断し、月曜日であれば後続のロジックを実行します。

- 当日のローソク足が下から上への反転形状を示しているかどうかを判断します。具体的には、1本目のローソク足の終値 < 2本目のローソク足の終値、かつ2本目のローソク足の終値 < 3本目のローソク足の終値であること。

- 上記の反転形状が成立した場合、3本目のローソク足の終値で買い建て(ロング)ポジションを開き、トレンドフォローを行います。

- 利益確定条件は、当日の高値ブレイクアウト、または損切りによる退出です。

- ポジションを6時間保有した後は強制的に手仕舞いします。

この戦略は、月曜日の特定時間帯における反転相場を利用し、反転ローソク足パターンを識別することで、安値で買い高値で売るという利益モデルを実現します。同時に、利益確定・損切りの条件を設定し、リスクをコントロールしています。

利点

本戦略の最大の利点は以下の通りです。

- 月曜日の取引時間中における特定の反転相場を利用して利益を上げます。

- 特定のローソク足パターンを識別することで、明確なエントリーシグナルを得られます。

- 利益確定・損切りの条件を設定しており、リスクをうまくコントロールできます。

- トレンドフォロー方式を採用しており、利益を最大化できます。

- 戦略のロジックはシンプルかつ明確で、理解と実装が容易です。

リスク

本戦略には以下のようなリスクも存在します。

- 月曜日の反転相場が明確でない場合、損失が発生する可能性があります。

- 反転後に再び押し戻され、損切りとなる可能性があります。

- 相場が急変し、損切りのコストが大きくなる可能性があります。

- ポジションの保有時間が長すぎると、損失につながる可能性があります。

対応策としては、損切り戦略を最適化し、保有時間を適切に短縮し、1回の損失を厳格にコントロールすることです。

これらの解決策は、損切り戦略の最適化、保有時間の短縮、1回の損失の厳格な管理です。

最適化の方向性

本戦略は主に以下の点から最適化が可能です。

- 機械学習手法を利用して、より正確な反転パターンを識別する。

- 損切り戦略を最適化する(例:トレーリングストップ、分割損切りなど)。

- 出来高の変化など、より多くの要因を組み合わせてトレンドの強さを判断する。

- 保有時間を動的に調整する。

- アルゴリズムを使用して適切なパラメータを自動決定する。

- ポジション切り替えメカニズムを追加し、双方向取引(ロング・ショート)を可能にする。

これらの最適化により、戦略の勝率と収益性を向上させることができます。

まとめ

総じて、本戦略は月曜日の特定時間帯における反転相場を利用し、明確なエントリー・イグジットメカニズムを設定することで、シンプルなトレンドフォローによる収益モデルを実現しています。固定の損切り・利確に比べ、本戦略はより良い結果を得ることができます。もちろん、市場の不確実性に対応するためにはさらなる最適化が必要です。本戦略は、デイトレード(日中立ち会い)における一つの参考アプローチとテンプレートを提供するものです。

Source

Pine

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("ET Forex TurnaroundMonday", overlay=true)

FirstYear = input(2018, minval=2000, maxval=2023, step=1)

FirstMonth = 1 //input(1, minval=1, maxval=12, step=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1