双方向リバーサルとモメンタム移動平均線戦略

概要

本戦略は、リバーサル戦略とモメンタム指標を組み合わせたコンビネーション戦略です。双方向リバーサル戦略と香氏モメンタムオシレーターを統合し、リバーサルの機会を発見すると同時にモメンタムシグナルを検証することで、より信頼性の高い取引シグナルを実現します。

戦略の原理

本戦略は以下の2つの部分から構成されます。

第1の部分は双方向リバーサル戦略です。これは前2日間の終値の変化を検出することでリバーサルの機会を判断します。具体的には、前2日間の終値が減少し、当日の終値が前日の終値より上昇し、かつストキャスティクスが設定水準を下回っている場合に買いシグナルとなります。逆に、前2日間の終値が増加し、当日の終値が前日の終値より下落し、かつストキャスティクスが設定水準を上回っている場合に売りシグナルとなります。

第2の部分は香氏モメンタムオシレーターです。これは価格変化量と一定期間内の平均変化量の大きさを比較することでモメンタムを判断します。モメンタム指標が設定上限を上回っていれば買いシグナル、下限を下回っていれば売りシグナルとなります。

本戦略は双方向リバーサルによる反転点の判断とモメンタム指標によるモメンタム状況の検証を総合的に行い、両方のシグナルが同じ方向である場合にのみ実際の売買シグナルが発生します。

戦略の利点

-

二重検証メカニズムにより、偽シグナルを回避し、シグナルの信頼性を向上させます。リバーサル戦略で潜在的な反転点を判断し、モメンタム指標で反転シグナルの有効性を検証します。

-

リバーサル戦略とトレンド戦略を組み合わせることで、リバーサルとトレンドの両方に対応し、市場の機会を柔軟に捉えます。

-

モメンタム指標を導入することで、リバーサルの罠を回避し、モメンタムが確認された場合にのみ取引を行います。

-

様々なパラメータを調整可能であり、異なる市場に合わせて最適化することができます。

戦略のリスク

-

リバーサルシグナルは大きく逆行する可能性があり、適切なストップロスが必要です。

-

反転ポイントの捕捉には精度が求められ、誤判定が発生する可能性があります。

-

モメンタム指標にはラグが生じるため、最適な反転ポイントを逃す可能性があります。

-

パラメータ設定は特定の市場に応じて慎重に最適化する必要があり、不適切な設定は取引リスクを増大させる可能性があります。

適切なストップロスで1回の損失を抑えることができます。パラメータ設定を最適化し、パラメータのロバスト性を追求します。リバーサルシグナルのトリガー条件を適度に緩和し、余裕を持たせるなどの方法でリスクを低減できます。

戦略の最適化方向

-

異なるリバーサルパラメータの組み合わせをテストし、市場の反転に対して感度の高いパラメータ設定を探します。

-

相対力指数(RSI)や出来高変化率など、異なるモメンタム指標を試します。

-

ブレイクアウトなどのフィルター条件を追加し、重要でない反転ポイントでの取引を避けます。

-

ストップロス戦略を評価し、最大ドローダウンが制御可能なストップロス方法を見つけます。

-

ポジション管理戦略を評価し、市場状況に応じてポジションサイズを調整します。

まとめ

本戦略はリバーサル戦略とモメンタム戦略の長所を融合しており、シグナルの信頼性が高く、市場の機会を柔軟に捉えることができるという利点があります。パラメータの最適化、ストップロス管理、ポジション管理などの方法によりリスクを低減し、戦略の安定性と収益性を向上させることができます。全体として、本戦略はリバーサル戦略とトレンド戦略の効果的な組み合わせを先駆的に模索しており、さらなる研究と応用に値します。

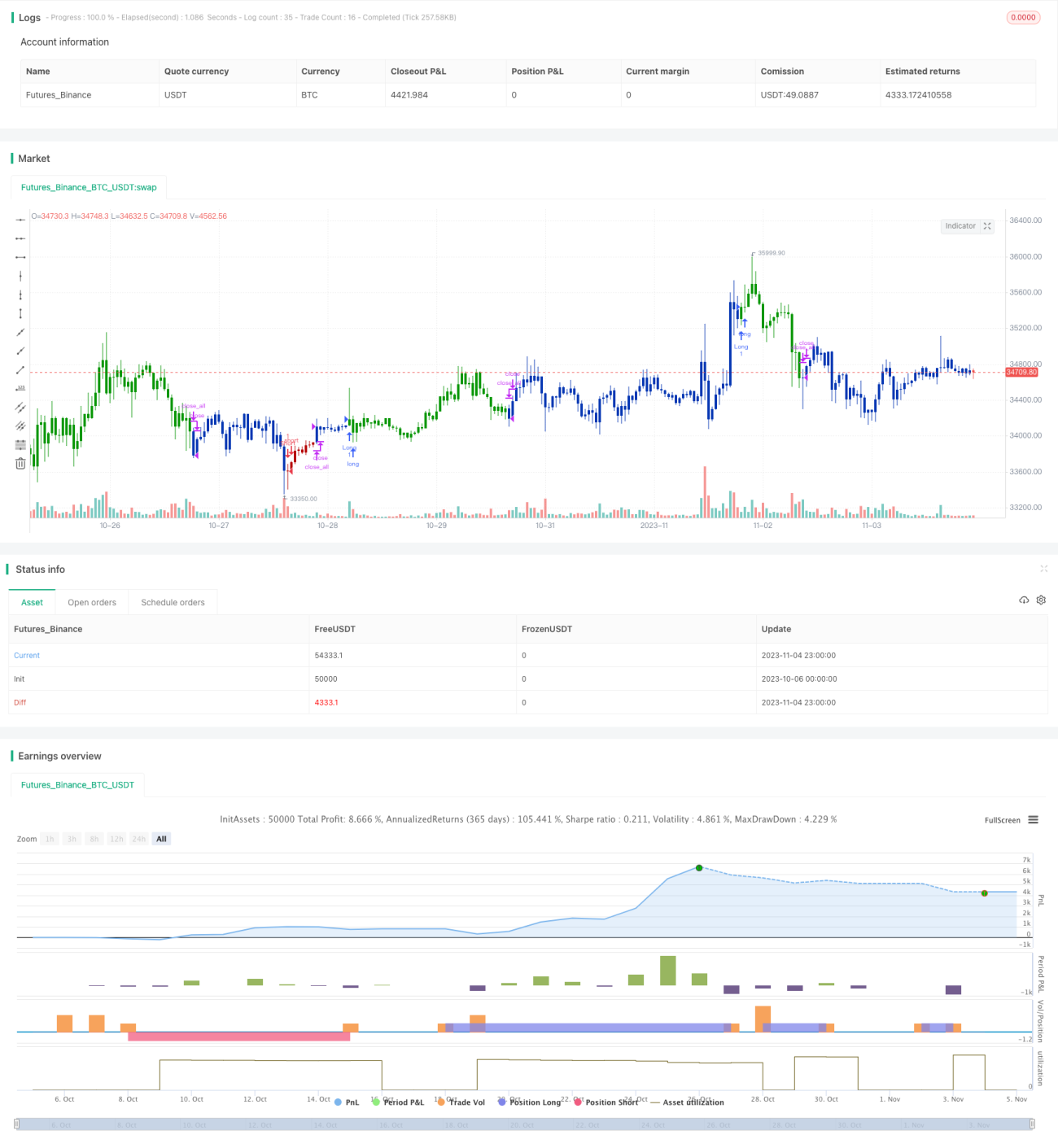

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/08/2019

// This is combo strategies for get a cumulative signal. - 1