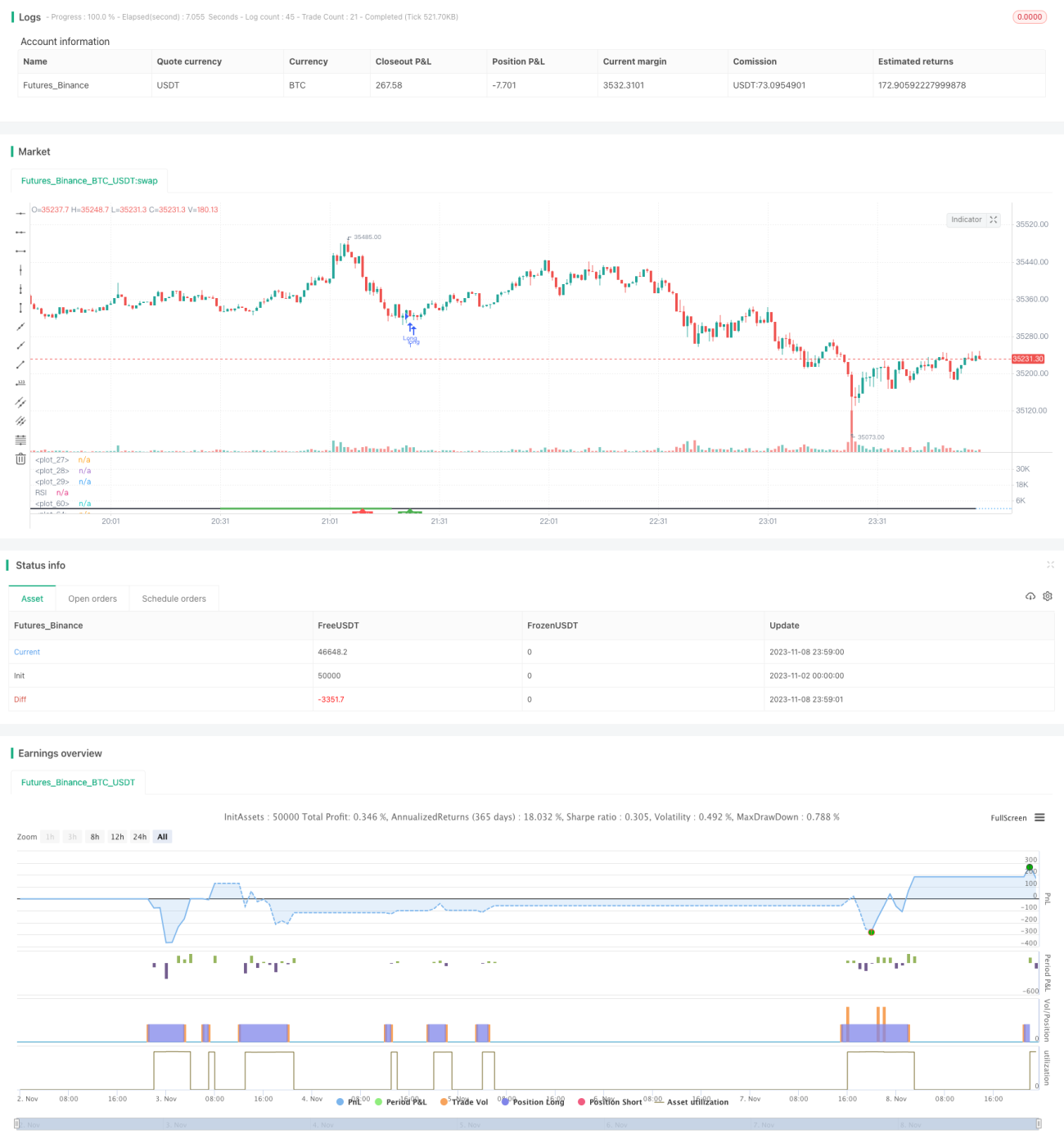

ブル・ベア長期ロング戦略

概要

本戦略は、RSI指標の強気ダイバージェンス(ブルダイバージェンス)を検出することで、短期的にビットコイン価格が反発上昇するタイミングを判断し、適切な買い入れタイミングを特定します。

戦略の原理

-

RSI指標を用いて強気ダイバージェンスの有無を判断

- RSI指標のパラメータを定義(デフォルト14期間)

- 現在のRSI値を計算

- 以下の強気ダイバージェンス状況が存在するか判断:

- RSI指標がより低い安値を形成

- その時点で価格もより低い安値を形成

- その後、RSI指標がより高い安値を形成

- その時点で価格がより高い安値を形成

-

RSI値が閾値より低いか判断

- RSI安値判定閾値を定義(デフォルト40)

- 現在のRSI値がこの閾値より低い場合、買い入れタイミングである可能性あり

-

終値がダイバージェンス開始時の安値より低いか判断

- そうであれば、ダイバージェンスの買いシグナルをさらに検証

-

損切りの条件を定義

- 損切りパーセンテージを設定(デフォルト5%)

- ドローダウンがこのパーセンテージに達した場合、損切りで退出

-

利益確定の条件を定義

- RSI高値判定閾値を設定(デフォルト75)

- RSIが上昇してこの閾値に達した場合、利益確定で退出

優位性分析

-

RSI指標を用いた強気ダイバージェンスの判断で、価格の短期的な反発タイミングを効果的に捉えられる

-

RSI安値判断と組み合わせることで、反発前に具体的な買い入れポイントを確定できる

-

損切りと利確条件を設定することで、取引のリスクと利益を管理できる

-

本戦略はビットコインの実際の取引におけるRSI指標の特性を多く参考にしており、ビットコインの短期ロングに非常に適している

-

戦略パラメータは合理的に設定されており、様々な市場状況に対応可能で、実戦応用に有利

リスク分析

-

RSI指標が機能しない可能性があり、判断を誤ると取引損失につながる

-

単一のテクニカル指標では偽シグナルが発生しやすいため、他の指標と組み合わせて使用すべき

-

適切なパラメータ値を選択する必要があり、設定が不適切だと戦略の収益率に影響する

-

ロング方向の取引では、大きなトレンドに注意し、逆張りを避ける必要がある

-

取引コストに注意する必要があり、頻繁な取引は最終的な収益に悪影響を及ぼす

-

定期的にバックテストでパラメータを最適化し、市場に応じて戦略を調整すべき

最適化の方向性

-

移動平均線などの他の指標を追加し、フィルター条件を設定して偽シグナルを減らすことを検討

-

異なる期間のパラメータ設定をテストし、最適なパラメータ組み合わせを探す

-

より大きな時間軸のトレンド判断と組み合わせ、トレンド反転時のロングを避ける

-

動的な損切りを設定し、利益が一定水準に達したら徐々に損切りラインを引き上げる

-

具体的なポジション状況に応じて、異なる損切り幅を設定する

-

機械学習などの技術を導入し、パラメータの自動最適化を実現する

まとめ

本戦略は、RSI指標の強気ダイバージェンスを捉えることで、ビットコインが短期的に反発上昇する可能性を判断し、買い入れタイミングを特定します。戦略はシンプルで効果的であり、多くの実戦経験を反映しており、ビットコインの短期ロングに非常に適しています。ただし、単一のテクニカル指標では偽シグナルが発生しやすいため、他の指標と組み合わせて使用するとともに、パラメータ最適化、損切り設定、取引コストなどの問題に注意する必要があります。適切に使用すれば、本戦略は実戦で大きな利益を得ることができます。

- 1