二重波動フィルタートレーディング戦略

概要

ダブルウェーブ振動フィルター戦略は、価格のボラティリティに基づく取引戦略です。異なる2つのパラメータで設定された平均変動幅インジケーターと、価格と変動幅の関係を利用して取引シグナルを生成します。この戦略は、ビットコインなどのボラティリティの高いデジタル資産に適しています。

戦略の原理

この戦略では、異なる期間長さの平滑化変動幅インジケーターを2つ使用します。高速変動幅インジケーター(デフォルト期間27)と低速変動幅インジケーター(デフォルト期間55)です。変動幅インジケーターの計算式は、現在の期間の価格変動幅の指数平滑移動平均に倍数(例:1.6)を乗じたものです。

ダブルウェーブ振動フィルター戦略は、価格と2つの変動幅インジケーターの関係を比較し、現在が一定の振幅のレンジ内にあるかどうかを判断します。価格がそのレンジを突破した場合に取引シグナルを生成します。

具体的には、戦略は中央線を基準とします。中央線は2つの変動幅インジケーターの平均値です。価格が中央線より上で高速変動幅1つ分を超えた場合にロングシグナルを生成し、価格が中央線より下で高速変動幅1つ分を下回った場合にショートシグナルを生成します。

誤報をフィルタリングするために、この戦略にはもう1つの条件が追加されています。それは、価格が1つ前の期間の価格の動きと一致している場合にのみシグナルを生成するというものです。例えば、価格が上昇していて中央線を変動幅1つ分超えた場合にのみロングシグナルを生成します。

要約すると、この戦略はダブル変動幅インジケーターを使用してレンジを特定し、価格がそのレンジを突破したことをシグナルとして取引注文を生成します。同時に価格方向のフィルターを追加することで、誤ったシグナルを減らします。

戦略の利点

ダブルウェーブ振動フィルター戦略の利点は以下の通りです。

- 価格のボラティリティ特性を利用しており、ビットコインなどのボラティリティの高い資産に適応できます。ダブル変動幅インジケーターにより、価格のレンジをより正確に特定できます。

- ダブル変動幅インジケーターには異なる時間長が含まれています。高速インジケーターは短期的なブレイクアウトの機会を捉え、低速インジケーターは長期的なトレンドを考慮します。

- 価格方向のフィルター条件を追加することで、短期的な変動による誤ったシグナルを減らすことができます。

- 取引ロジックはシンプルで明確であり、理解・実装が容易で、定量取引に適しています。

戦略のリスク

ダブルウェーブ振動フィルター戦略には、注意すべきリスクもいくつかあります。

- ボラティリティ指標に依存しているため、低ボラティリティ市場では効果が薄い可能性があります。

- 変動幅のパラメータは、異なる銘柄に合わせて調整・最適化する必要があります。そうしなければ、取引機会を逃したり、誤ったシグナルを生成したりする可能性があります。

- 価格がボラティリティから乖離する状況を考慮していません。ボラティリティが上昇しても価格がそれに見合った上昇を見せない場合、誤ったシグナルが発生する可能性があります。

- 高ボラティリティ環境では、ストップロスの設定を調整する必要があるかもしれません。積極的すぎるストップロスは頻繁に損切りを発生させます。

戦略の最適化

この戦略は、以下の点から最適化が可能です。

- 変動幅のパラメータをテスト・最適化し、異なる銘柄・異なる期間における最適なパラメータの組み合わせを見つけます。

- 直近のボラティリティに基づいてストップロス位置を動的に調整するメカニズムを追加し、ストップロス戦略を最適化します。

- 価格とボラティリティの乖離に基づくフィルター条件を追加し、誤ったシグナルを回避します。

- 出来高の変化など他の指標を組み合わせることで、エントリーの確実性を高めます。

- 戦略に適した利食い・エグジットメカニズムをテストし追加します。

まとめ

ダブルウェーブ振動フィルター戦略は、全体的に高ボラティリティ資産に対する効果的な取引戦略です。価格のボラティリティ特性を正しく活用し、シンプルで明確な取引ロジックを生み出しています。パラメータの最適化やリスク管理などを通じてさらに改善することで、この戦略は定量取引システムにおいて価値ある構成要素となり得ます。また、市場のボラティリティ特性に基づいたアルゴリズム取引の考え方を提供してくれます。

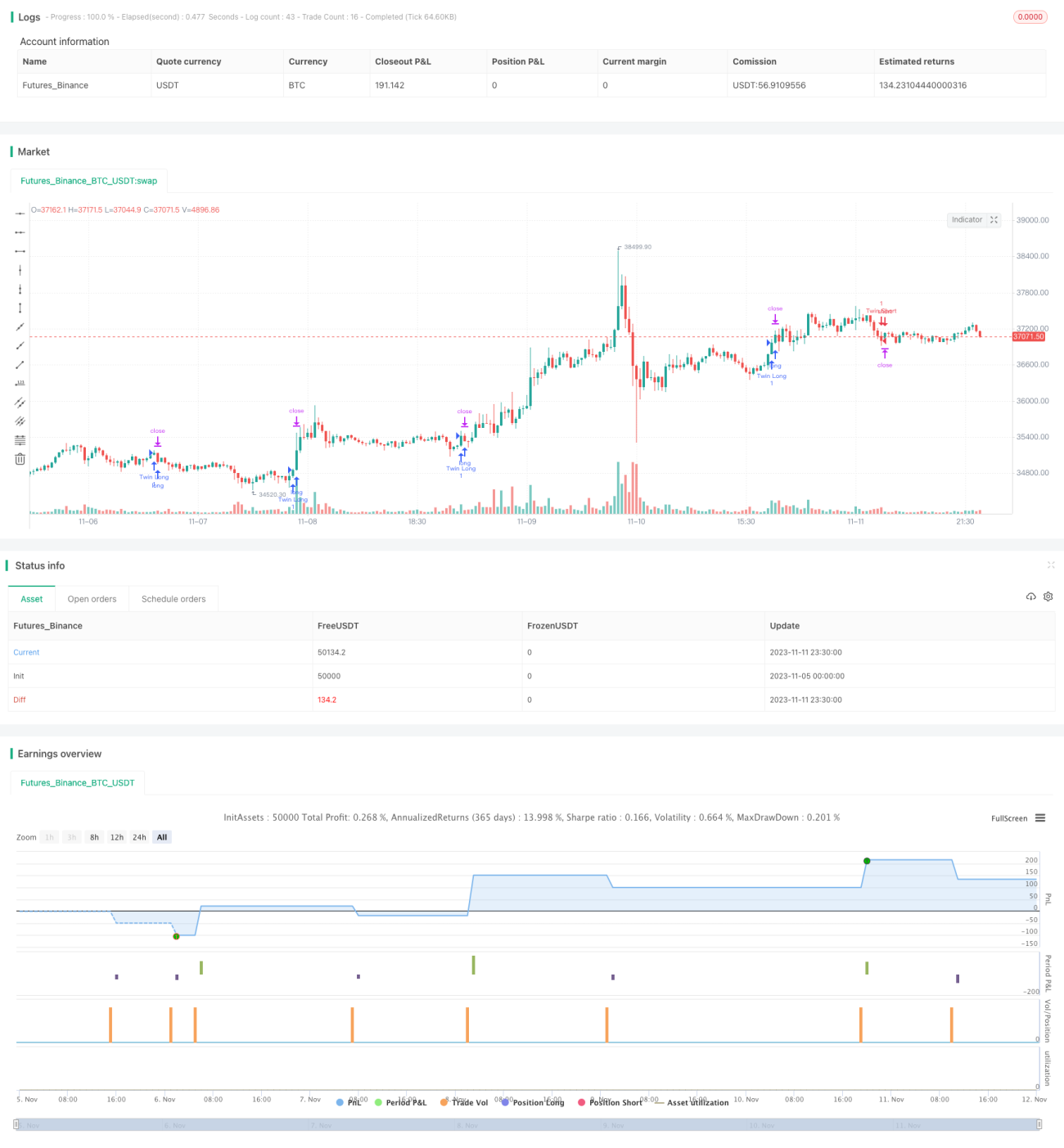

/*backtest

start: 2023-11-05 00:00:00

end: 2023-11-12 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © colinmck, greenmask9

//@version=4- 1