トレンド反転トレーリングストップ戦略

概要

本戦略はトレンド反転指標をベースとし、トレンドフォロー型のストップロス機構と組み合わせることで、トレンド相場ではトレンドに追随し、レンジ相場では損失を最小限に抑える効果を実現します。

戦略の原理

本戦略では、Hull移動平均線を主要なトレンド判断指標として使用します。価格がHull平均線を上抜けた場合に買い、下抜けた場合に売りを行います。同時に、McGinley平均線を用いてトレンドを確認します。

ポジション保有中に価格が反転し、Hull平均線のクロスオーバーが発生した場合には、トレンド変更ロジックが実行され、現在のポジションをクローズします。

また、本戦略にはトレンドフォロー型のストップロス機構が導入されています。ポジション保有後は、ATRに基づいて動的なストップロス価格を計算します。価格の動きに応じてストップロスラインも動的に調整され、利益のトレーリングストップロスを実現します。

戦略の利点

- Hull平均線を使用してトレンド反転ポイントを判断。Hull平均線はブレイクアウトシグナルに対する感度が高い。

- McGinley平均線と組み合わせてトレンドを確認することで、誤ったブレイクアウトの一部をフィルタリング可能。

- 動的なトレーリングストップロス機構により、市場のボラティリティに応じてストップロスの幅を調整でき、損失を効果的に抑制。

- Hull平均線のクロスオーバー確認時、トレンド反転に素早く対応し、損失拡大を防止。

- 異なるパラメータ組み合わせを容易に切り替えてテストし、最適なパラメータを探索可能。

リスクと解決策

-

レンジ相場ではストップロスが発動される可能性がある。

- ストップロスの幅を適度に拡大し、バッファーゾーンを追加することで対応可能。

-

急激な相場変動では、トレーリングストップロスが価格変動に追いつかない場合がある。

- 平滑化期間を短縮することで、ストップロスが価格に迅速に追随するように調整可能。

-

誤ったブレイクアウトにより、不必要な損失が発生する可能性がある。

- 他の指標を追加して確認し、誤ったブレイクアウトを回避。

-

パラメータ設定が不適切だと、戦略のパフォーマンスが低下する可能性がある。

- 異なる市場サイクルでバックテストを実施し、最適なパラメータを見つけることが推奨される。

最適化のアイデア

- 他の指標(ローソク足パターン、ボリンジャーバンド、RSIなど)を追加して確認することで、シグナルの品質を向上。

- 異なる銘柄や期間のパラメータを最適化し、最適なパラメータ組み合わせを見つける。

- 機械学習などの手法を用いて、パラメータの適応的最適化を試みる。

- ストップロスアルゴリズムを最適化し、ストップロス機能を維持しつつ、不必要なストップロスを最小限に抑える。

- 資金管理と組み合わせてポジション管理戦略を最適化。

- 自動利益確定メカニズムの追加を検討。

まとめ

本戦略は総じて堅実なトレンドフォロー戦略です。固定ストップロスと比較して、動的なストップロス機構を採用することで、市場のボラティリティに応じてストップロスの幅を調整し、ストップロスがかかる確率を効果的に低減します。また、Hull平均線とトレンド変更ロジックの導入により、トレンド反転に迅速に対応できます。しかし、レンジ相場でのストップロスリスクや誤ったブレイクアウトリスクなどの一定のリスクも存在します。指標パラメータ、ストップロスアルゴリズム、ポジション管理などをさらに最適化することで、さまざまな市場においてより安定したパフォーマンスを発揮することが期待できます。

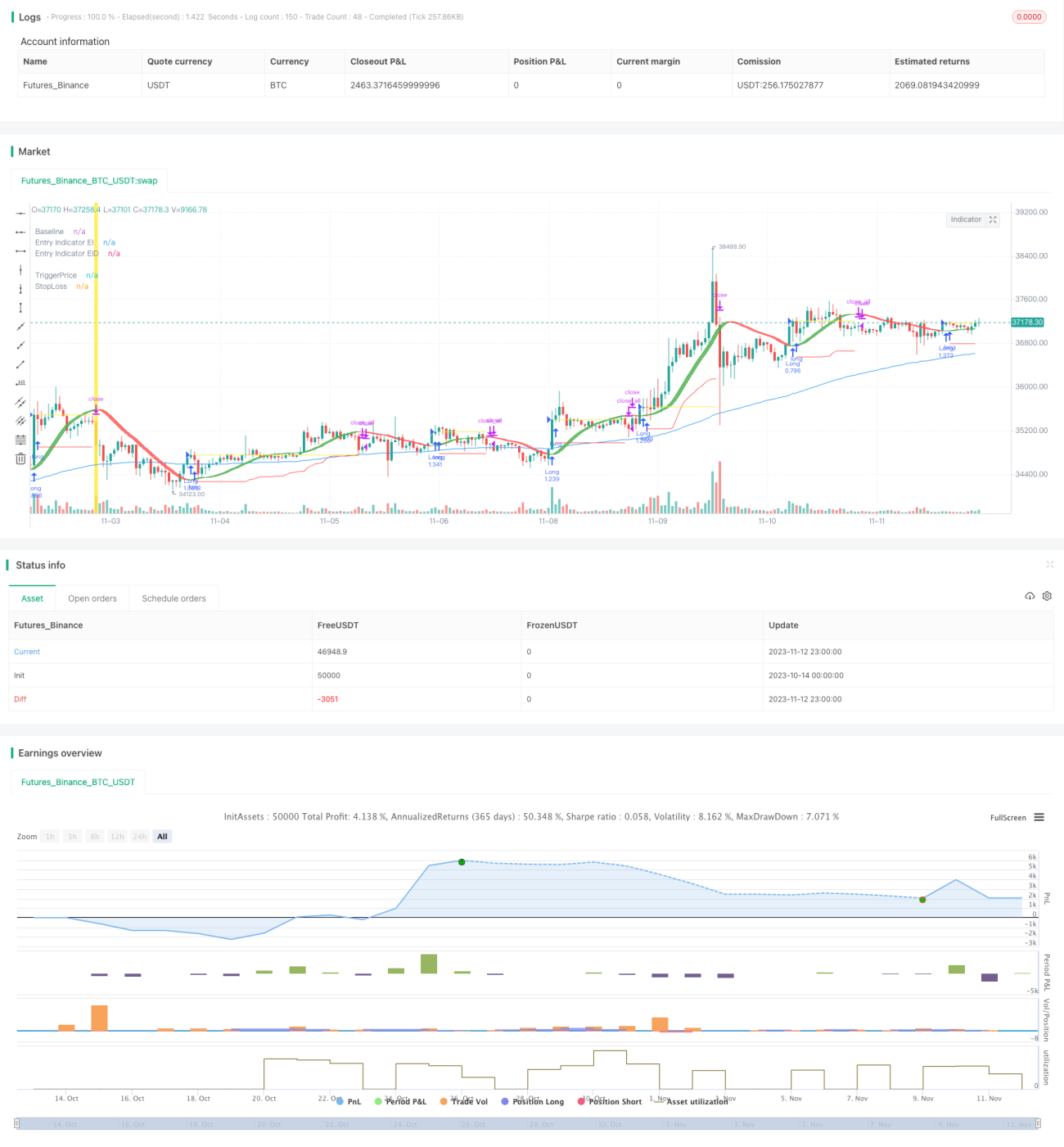

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1