モメンタム転換パターン反転戦略

概要

本戦略は、123パターン反転戦略とイージー・オブ・ムーブメント(EOM)戦略を組み合わせたものであり、価格の転換点を捉えて取引することを目的としています。123パターン反転戦略は、株価が3営業日連続で特定のパターンを形成した際にシグナルを生成します。イージー・オブ・ムーブメント戦略は、価格と出来高の変化を利用して市場のモメンタムを判断します。これら2つの戦略を組み合わせることで、価格のテクニカルパターンと市場モメンタムの両方を考慮し、取引シグナルの精度を高めます。

戦略の原理

本戦略は以下の2つの部分から構成されます。

-

123パターン反転戦略

- ストキャスティクス(Stoch)指標を使用して買われ過ぎ・売られ過ぎを判断します。

- 終値が2日連続で下落し、かつStochのFastラインがSlowラインを上回った場合に売りシグナルを生成します。

- 終値が2日連続で上昇し、かつStochのFastラインがSlowラインを下回った場合に買いシグナルを生成します。

-

イージー・オブ・ムーブメント戦略

- 前日のレンジの中間価格(ミッドポイント)を計算します。

- 前日からのミッドポイントの変化(移動)を計算します。

- ミッドポイントの移動と出来高の比率を計算します。

- 比率が閾値を超えた場合に強気、閾値を下回った場合に弱気と判断します。

両方のシグナルを統合し、イージー・オブ・ムーブメントと123パターンが同時に買いシグナルを出した場合に買いポジション、同時に売りシグナルを出した場合に売りポジションを開きます。

優位性分析

本戦略には以下のような利点があります。

-

価格のテクニカルパターンと市場モメンタムを組み合わせることで、シグナルの精度が向上します。

-

123パターン反転は転換点を捉え、イージー・オブ・ムーブメントはトレンドのモメンタムを判断するため、互いに補完し合います。

-

Stoch指標により、レンジ相場での過度な売買を回避できます。

-

取引ロジックがシンプルで分かりやすく、実装が容易です。

-

パラメータをカスタマイズでき、様々な市場環境に対応可能です。

リスク分析

本戦略には以下のようなリスクも存在します。

-

パラメータ設定に依存しやすく、不適切な設定では取引頻度が高すぎたり、シグナルを見逃したりする可能性があります。

-

複数のフィルター条件を組み合わせているため、シグナルの発生頻度が低くなることがあります。

-

イージー・オブ・ムーブメント指標は市場のボラティリティに敏感で、誤ったシグナルを生じる可能性があります。

-

実取引ではバックテストよりもパフォーマンスが劣る場合があり、ポジションサイズの管理が必要です。

-

トレンド相場にのみ有効で、レンジ相場には適していません。

最適化の方向性

以下の点から本戦略を最適化できます。

-

パラメータを最適化し、フィルター条件の厳格さを調整して、取引頻度とシグナル品質のバランスを取ります。

-

ストップロス戦略を導入し、1回の損失を厳密に制御します。

-

トレンドフィルターを組み合わせ、逆張り取引を回避します。

-

資金管理モジュールを追加し、ボラティリティに応じてポジションサイズを動的に調整します。

-

機械学習手法を用いてパラメータを最適化し、市場に動的に適応させます。

まとめ

本戦略は価格テクニカル指標と市場モメンタム指標を統合し、転換点を捉えつつトレンドの質を確認するため、実戦的な価値が高いです。ただし、取引頻度、1回の損失、逆張り取引のリスクを管理する必要があります。パラメータ最適化、ストップロス戦略、トレンドフィルターなどの手段により、戦略の安定性と収益性をさらに向上させることができます。本戦略は考え方が明確で実装も容易であり、定量トレーダーがさらに研究・改良する価値があります。

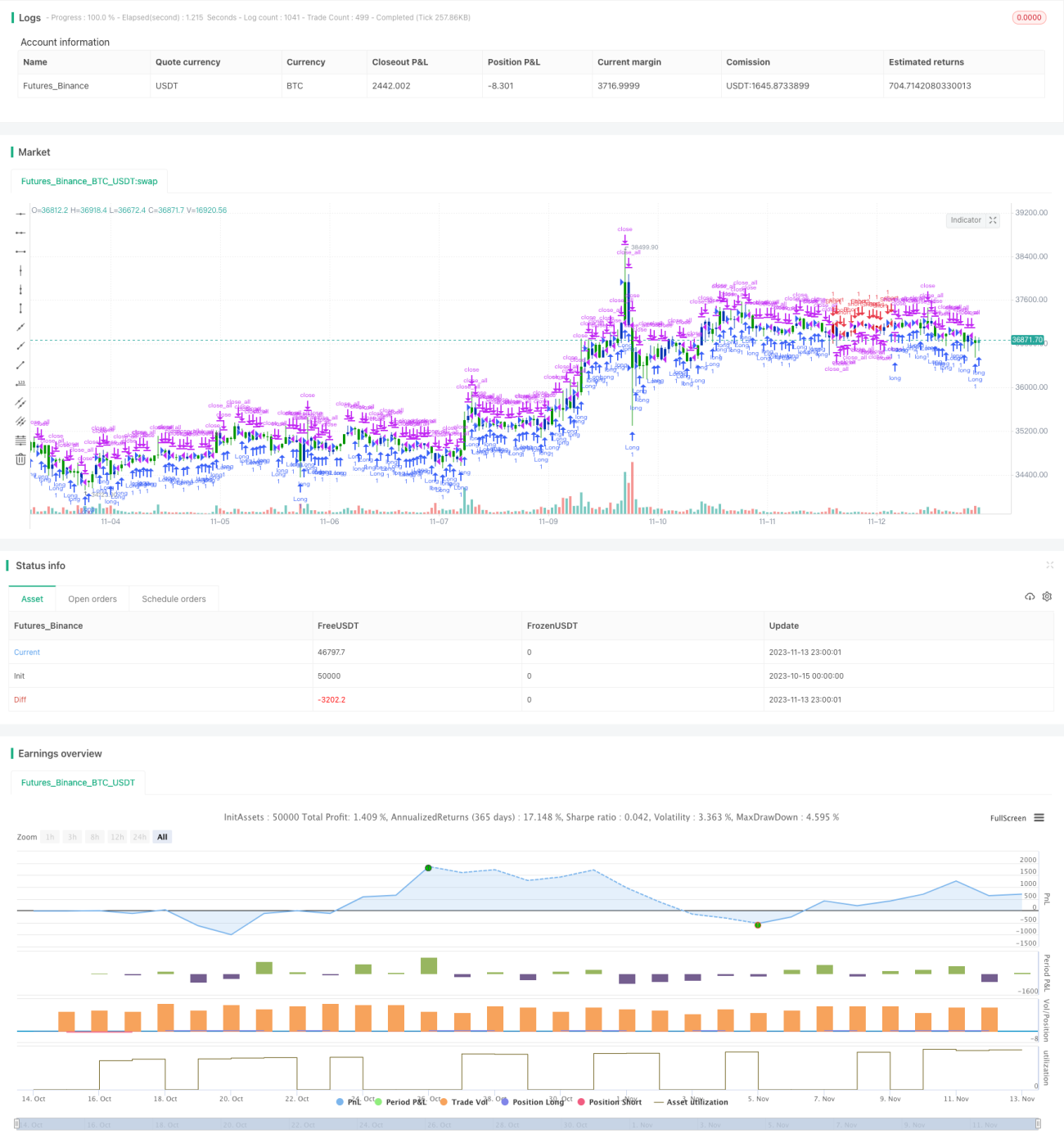

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 14/04/2020

// This is combo strategies for get a cumulative signal. - 1