複数移動平均線ギャップ双方向取引戦略

概要

本戦略は、Williamsの新高新低インジケーターを用いて買い・売りの転換シグナルを識別し、複数の移動平均線によるブレイクアウト取引を組み合わせ、さらにRSIインジケーターで偽シグナルをフィルタリングすることで、効率的な双方向取引を実現します。

戦略の原理

-

Williams新高新低インジケーターは、一定期間内の最高値と最安値を用いて転換点を判断し、買い・売りシグナルを発します。

-

20日、50日、100日の移動平均線で構成される複数移動平均線において、価格がそのうち2本の線をブレイクした場合に取引シグナルを発します。

-

RSIインジケーターで買われ過ぎ・売られ過ぎ領域を判断し、不確実なシグナルをフィルタリングします。

-

本戦略は、価格がどの2本の移動平均線をブレイクしたかを判断し、WilliamsインジケーターのシグナルおよびRSIによるフィルタリングを組み合わせることで、安定した買い・売りシグナルを生成します。

-

エントリー判断:短期移動平均線が中期・長期移動平均線を下から上へブレイクし、かつWilliams新低(売られ過ぎ)とRSI低位のシグナルが同時に発生した場合に買い建てます。短期移動平均線が中期・長期移動平均線を上から下へブレイクし、かつWilliams新高(買われ過ぎ)とRSI高位のシグナルが同時に発生した場合に売り建てます。

-

ストップロス・利確:固定比率によるストップロス・利確を設定します。

戦略の優位性

-

Williamsインジケーターは重要なサポート・レジスタンスを正確に判断し、転換シグナルを識別できます。

-

複数移動平均線によるブレイク判断により、単一の移動平均線の振動による誤ったシグナルを回避できます。

-

RSIインジケーターによる偽シグナルのフィルタリングにより、エントリータイミングがより正確で信頼性の高いものになります。

-

固定のストップロス・利確システムによりリスクを管理し、損益を明確にします。

-

転換インジケーターとトレンドインジケーターの二重確認により、取引シグナルの精度と信頼性が向上します。

戦略のリスク

-

取引対象の選択を誤ると、異なる銘柄ごとにパラメーター調整が必要となります。

-

期間設定が不適切な場合、異なる時間足に応じたパラメーター調整が必要です。

-

固定のストップロス・利確は市場の変化に応じて調整できないため、早期のストップロスや利確不足が生じる可能性があります。

-

移動平均線が振動する際に誤ったシグナルが発生しやすくなります。

-

インジケーターが発散している場合にシグナルが遅れることがあります。

戦略の最適化方向

-

取引対象に応じてパラメーターを動的に最適化します。

-

自動調整型のストップロス・利確システムを導入し、損益をより合理的にします。

-

MACDやストキャスティクスなどの追加インジケーターによるフィルタリングを増やし、誤シグナルを低減します。

-

機械学習アルゴリズムを導入し、最適な取引タイミングを自動識別します。

-

より多くのトレンド判断インジケーターを組み合わせ、トレンド相場を識別します。

まとめ

本戦略は、Williamsインジケーター、移動平均線、RSIインジケーターなどの複数のテクニカル分析ツールを総合的に活用し、二重確認により誤シグナルを低減することで、反転の機会を効果的に捉えます。また、固定のストップロス・利確でリスクを管理するため、全体的に信頼性が高く実用的な双方向取引戦略です。今後の課題として、パラメーターの最適化、利確・ストップロスの最適化、モデル統合などの方法により、戦略の効果をさらに高めることが期待されます。

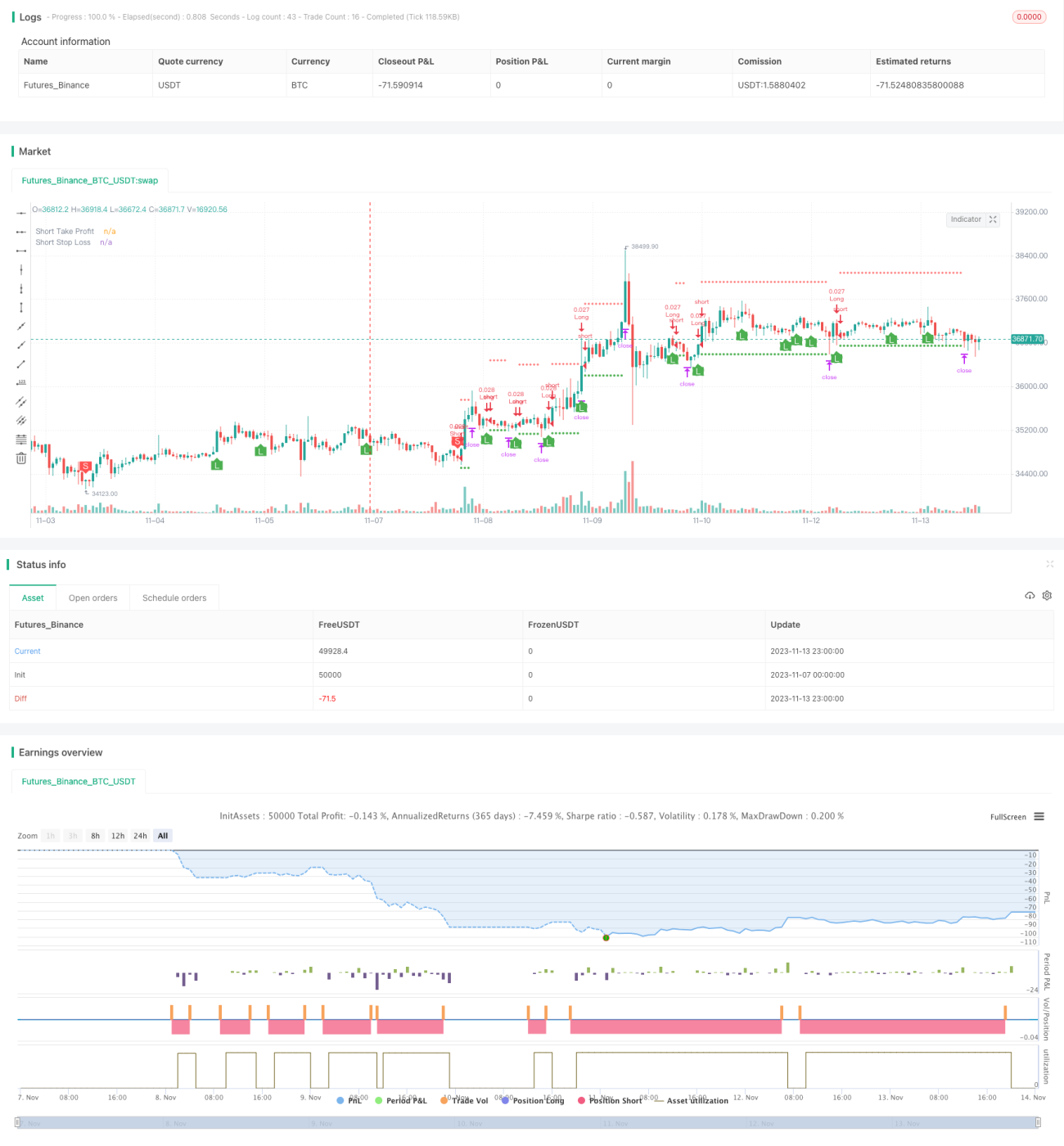

/*backtest

start: 2023-11-07 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1