二重移動平均線クロス戦略

概要

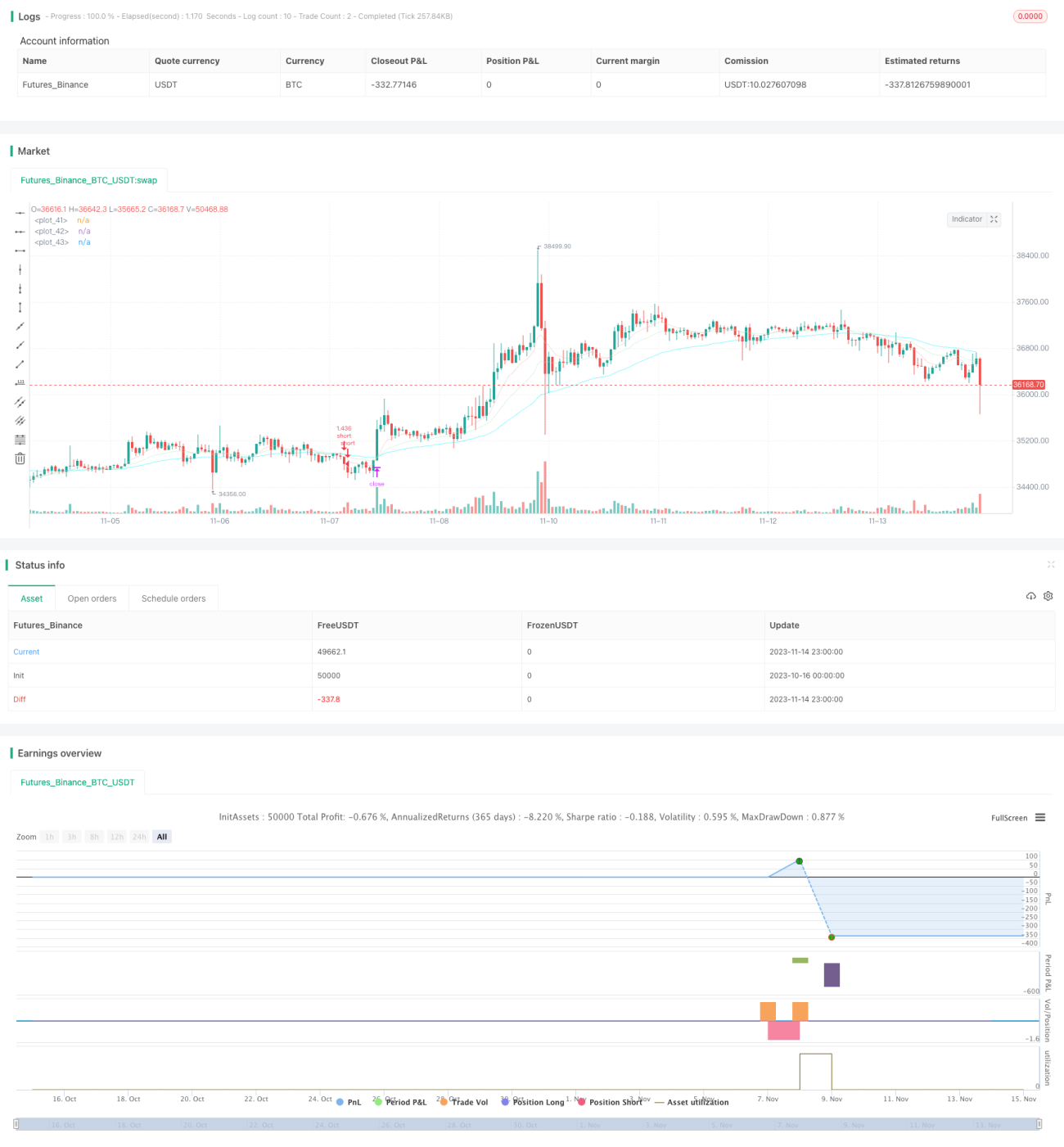

ダブル移動平均線クロス戦略は、異なる期間の移動平均線を計算して価格トレンドの方向性を判断し、トレンドフォローを実現します。短期移動平均線が長期移動平均線を上抜けたら買い、下抜けたら売りという、典型的なトレンドフォロー戦略です。

戦略の原理

本戦略は9期間、21期間、50期間の指数移動平均線(EMA)に基づいています。9期間EMAは短期トレンド、21期間EMAは中期トレンド、50期間EMAは長期トレンドを表します。

9期間EMAが21期間EMAを上抜けた場合、短期トレンドが上昇に転じたと判断して買い;9期間EMAが21期間EMAを下抜けた場合、短期トレンドが下降に転じたと判断して売りを行います。ここではクロス関数crossover()を用いて移動平均線のクロス状況を判断しています。

コード内では、買いポジションと売りポジションのエントリー、利確、損切りのロジックが設定されています。エントリー条件は移動平均線の上抜けまたは下抜けです。買いの利確はエントリー価格×(1+入力された利確比率)、売りの利確はエントリー価格×(1-入力された利確比率)です。買いの損切りはエントリー価格×(1-入力された損切り比率)、売りの損切りはエントリー価格×(1+入力された損切り比率)です。

さらに、コードにはいくつかのフィルター条件が追加されています。例えば、トレンド性フィルター:移動平均線が上下にクロスする前のローソク足がレンジ相場でないことを要求します。また、資金効率フィルター:戦略の純資産がN日移動平均線を下回らないようにし、損失が大きすぎる場合でも取引を続けないようにします。これらのフィルター条件は、ある程度偽のシグナルを回避できます。

全体として、本戦略はダブルEMAクロスを使用して価格トレンドの方向性を判断し、合理的な利確・損切りロジックにより中長期トレンドを捉えることができます。しかし、単一ファクター戦略であるため、シグナルが不安定になる可能性があり、さらなる最適化が可能です。

メリット分析

- ダブル移動平均線クロスでトレンド方向を判断するため、原理がシンプルで理解・実装が容易。

- 異なる期間のEMAを使用することで、長期・短期のトレンドを判断できる。

- 利確・損切りロジックを設定することで、利益を確定しリスクをコントロール。

- フィルター条件を追加することで、ある程度偽のシグナルを除去可能。

- パラメータを自由に設定でき、期間の組み合わせを最適化してさまざまな市場環境に対応可能。

リスク分析

- 単一ファクター戦略であるため、取引シグナルが不安定になる可能性がある。価格がレンジ相場の場合、無駄な取引が何度も発生する可能性がある。

- EMAクロス時には価格がすでにある程度動いている可能性があり、高値掴みや底値売りのリスクがある。

- 取引コストを考慮しておらず、実運用では収益が減少する可能性がある。

- 損切りを設定していない場合、相場が急変した際の損失をコントロールできない。

対応方法:

- MA期間パラメータを最適化し、シグナルをより安定させる。

- 他の指標と組み合わせてシグナルをフィルタリングする。

- 取引量を増やしてコストの影響を低減する。

- 損切りポイントを設定し、最大損失を制限する。

最適化の方向性

本戦略は以下の点で最適化可能です:

-

移動平均線の期間パラメータを最適化し、最適な期間の組み合わせを見つける。適応型最適化技術を導入し、動的に最適期間を選択することも可能。

-

他のテクニカル指標(MACD、KDなど)を追加してシグナルをフィルタリングし、シグナル品質を向上させる。または、機械学習を導入してシグナルを評価し、偽のシグナルを自動的に除去する。

-

出来高分析を組み合わせる。例えば、移動平均線をブレイクしても出来高が不足している場合はシグナルを採用しない。

-

ブレイク発生時、その前の値動きのボラティリティを検討する。レンジ相場でのブレイクは偽のブレイクである可能性がある。

-

動的な損切りメカニズム(トレーリングストップ、Chandelier Exitなど)を構築し、損切り幅を縮小しつつ効果的に損失を制限する。

-

ポジション管理を最適化する(固定ポジション、動的ポジション、レバレッジポジションなど)。損益比率をより合理的にする。

-

取引コストやスリッページの影響を総合的に考慮する。利確・損切り比率を最適化し、実運用でも戦略が利益を出せるようにする。

まとめ

本戦略は全体的に構造が合理的で、原理もシンプルです。ダブルEMAクロスでトレンド方向を判断し、利確・損切りロジックも設定されているため、トレンドを捉えることができます。しかし、単一ファクター戦略であるため、パラメータ設定やシグナルフィルタリングなどのさらなる最適化により、より堅牢な戦略にすることができます。損切りやポジション管理などのメカニズムを追加することで、リスクをさらに低減できます。全体として、本戦略は信頼性の高いトレンドフォロー戦略のフレームワークを提供しており、最適化と調整を経て安定した投資リターンを得ることができます。

- 1