量的ダブルクリック利益反転戦略

概要

本戦略は、まず123フォーメーションで反転シグナルを判定し、次にクリンガー・クォンティティブ・オシレーターをフィルターとして組み合わせることで、反転の機会を高効率に捉える「クォンティタティブ・ダブルヒット戦略」です。

戦略の原理

戦略は以下の2つの部分から構成されます。

-

123フォーメーションによる反転シグナル判定

・ロングの場合:終値が2日連続で下落した後、3日目に陽線となり、かつストキャスティクス指標が低位にあるとき。

・ショートの場合:終値が2日連続で上昇した後、3日目に陰線となり、かつストキャスティクス指標が高位にあるとき。 -

クリンガー・クォンティティブ・オシレーター

価格変動幅と出来高の変化を組み合わせて資金の流入・流出を判断します。オシレーターがその平均線を上抜けたときがロングシグナル、下抜けたときがショートシグナルです。

最終的に、上記2つのシグナルを総合し、ダブルヒットで最終的なエントリーを確定します。

優位性の分析

本戦略の最大の強みは、反転フォーメーションと出来高系指標を組み合わせることで、反転の機会を高効率に捉えられる点です。さらに、ストキャスティクス指標を活用して偽のブレイクアウトを回避し、クリンガー・クォンティティブ・オシレーターで実際の資金の流れを判断することで、エントリータイミングを正確にできます。

リスク分析

本戦略の主なリスクは、反転フォーメーションの判定とパラメータ設定にあります。反転シグナルには一定の遅れが生じるため、パラメータを適切に設定し、最適な反転タイミングを逃さないようにする必要があります。また、反転フォーメーション自体が機能しない場合もあります。

リスクを軽減するには、パラメータを適切に最適化して反転シグナルの感度と即時性を高めることが考えられます。さらに、他のフィルター条件を追加して反転の回数と振幅を十分に確保し、ドローダウンの拡大を防ぐことも有効です。

最適化の方向性

本戦略の主な改善余地は、パラメータ調整と他の補助的な判定条件の追加にあります。具体的には、ストキャスティクス指標のパラメータを適度に短縮し、123フォーメーション判定の感度を最適化できます。また、現在主流の指標やフォーメーション(MACDのゴールデンクロス・デッドクロス、ダブルトップ/ダブルボトムなどの多重底判定)を組み合わせることも可能です。

さらに、ストップロスやテイクプロフィット条件を動的に調整し、戦略を市場の変化に適応させることも検討できます。また、機械学習を活用してパラメータをリアルタイムで最適化することも考えられます。

まとめ

本戦略は、古典的な反転理論と出来高系テクニカル指標を統合し、反転の機会を高効率に捉えます。最適化の余地が大きく、さらなる効果向上の可能性を秘めており、実戦での検証と継続的な改善に値する戦略です。

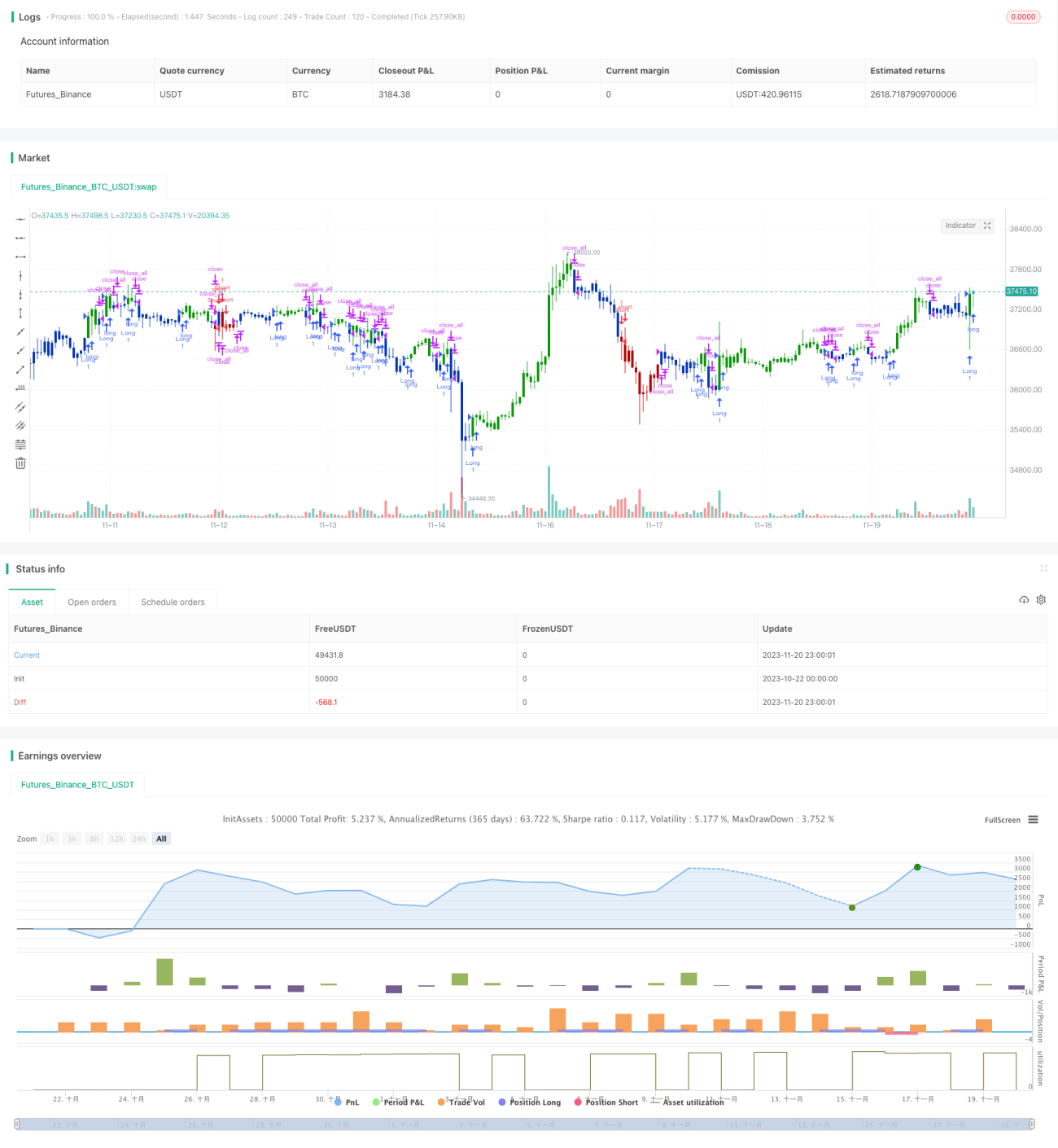

/*backtest

start: 2023-10-22 00:00:00

end: 2023-11-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/12/2020

// This is combo strategies for get a cumulative signal. - 1