ダブルトレンド移動平均線インテリジェントトラッキング投資戦略

概要

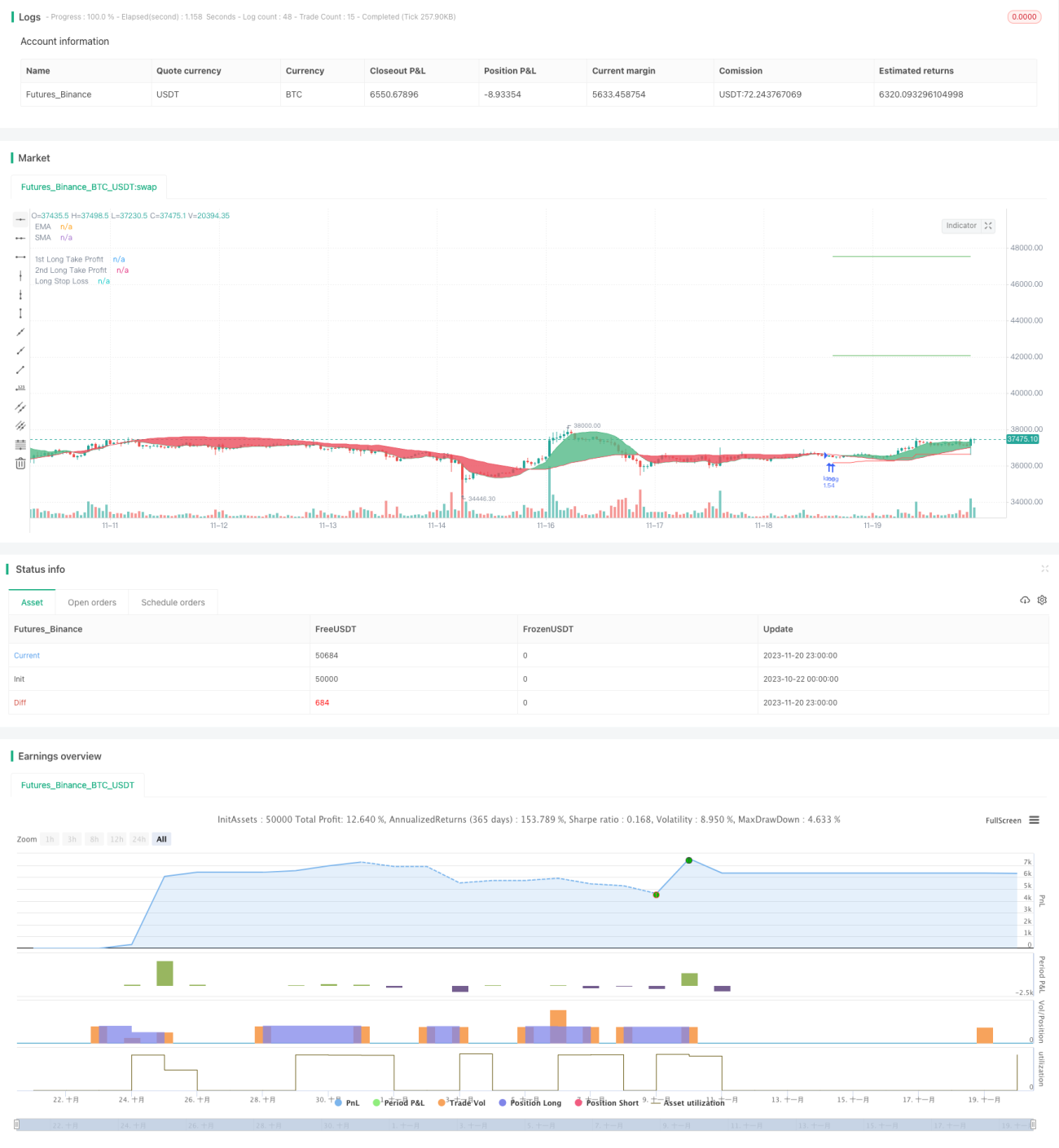

この戦略は主にBTCの長期投資を自動化するためのものです。二重EMAとLSMAのクロスを使用してトレンド方向を判断し、ATRインジケーターで動的ストップロスを計算することで、BTCの強気トレンドを効果的に追跡します。

戦略の原理

-

25期間のEMAと100期間のLSMAで二重移動平均線を構成し、それらのクロスで相場のトレンドを判断します。EMAは価格変化に素早く反応し、LSMAはダマシのブレイクアウトをフィルタリングします。

-

速いEMAが遅いLSMAを上抜けた場合、まだ強気トレンドにあると判断してロングします。逆に速いEMAが遅いLSMAを下抜けた場合は弱気トレンド入りと判断し、ポジションを決済します。

-

ロングに入った後、ATRインジケーターで計算した動的ストップロスを継続的に調整し、BTCの上昇トレンドを効果的に追跡します。具体的には、ストップロスラインの初期点はエントリー価格とし、その後は調整のたびに固定比率のATR分だけ上方にスライドさせます。

-

ストップロスラインはBTC上昇による含み益を効果的に固定しつつ、ストップポイントが最新価格に近づきすぎて頻繁なストップロスが発生するのを防ぎます。また、戦略では2つの異なる比率の移動利確も設定し、より多くの利益を確定します。

優位性の分析

-

二重移動平均線でトレンドを判断するため信頼性が高く、ダマシのシグナルを効果的に防止できます。

-

ATRによる動的追跡ストップロスは、利益の大部分を固定しつつ、頻繁な小さなストップロスを回避できます。

-

強気相場が終了しているかどうかに関わらず、移動平均線が退出シグナルを出せばストップロスで決済するため、リスク管理がしっかりしています。

-

自動化の度合いが高く、人手を介さずに実戦で長時間稼働させやすいです。

リスク分析

-

突発的な重要ニュースによる大きなスリッページ損失を避けるため、引き続き注意が必要です。

-

二重移動平均線の組み合わせでダマシのシグナルは減りますが、レンジ相場では完全には避けられません。

-

ATRパラメーターの設定が適切でないとストップロスの効果に影響するため、異なる銘柄に応じて調整する必要があります。

-

移動平均線の期間が不適切だったり、適時に更新されなかったりすると、シグナルに遅れが生じる可能性があります。

-

サーバーの安定性を確保し、異常ダウンによる自動取引の中断を防ぐ必要があります。

最適化の方向性

-

ボリンジャーバンドなど、より多くの指標を追加してトレンドを判断したり、機械学習モデルで価格を予測したりすることも試せます。

-

ATR動的ストップロスの計算方法をさらに調整・最適化し、ストップロスをより滑らかにすることができます。

-

取引量や日内ローテーションFEATUREに基づくアラート機構を追加し、重要ニュースの衝撃を防ぐことができます。

-

通貨ごとにパラメーターが異なるため、より多くの過去データを使って個別のパラメーターを訓練することも可能です。

まとめ

本戦略は全体的に見て非常に実用的なBTC自動投資プログラムです。二重EMAで大きなトレンドを判断するのは非常に信頼性が高く、ATRによる追跡ストップロスを併用することで、良好な利益を得られると同時に有効期間も長く維持できます。パラメーターの最適化・調整を続ければ、本戦略の効果はさらに向上する余地があり、実戦での検証に十分値します。

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Wunderbit Trading

//@version=4

strategy("Automated Bitcoin (BTC) Investment Strategy", overlay=true, initial_capital=5000,pyramiding = 0, currency="USD", default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent,commission_value=0.1)

//////////// Functions

Atr(p) =>

atr = 0.

Tr = max(high - low, max(abs(high - close[1]), abs(low - close[1])))

atr := nz(atr[1] + (Tr - atr[1])/p,Tr)- 1