ダブルタイムフレームとモメンタム指標に基づくアダプティブ利確・損切り戦略

概要

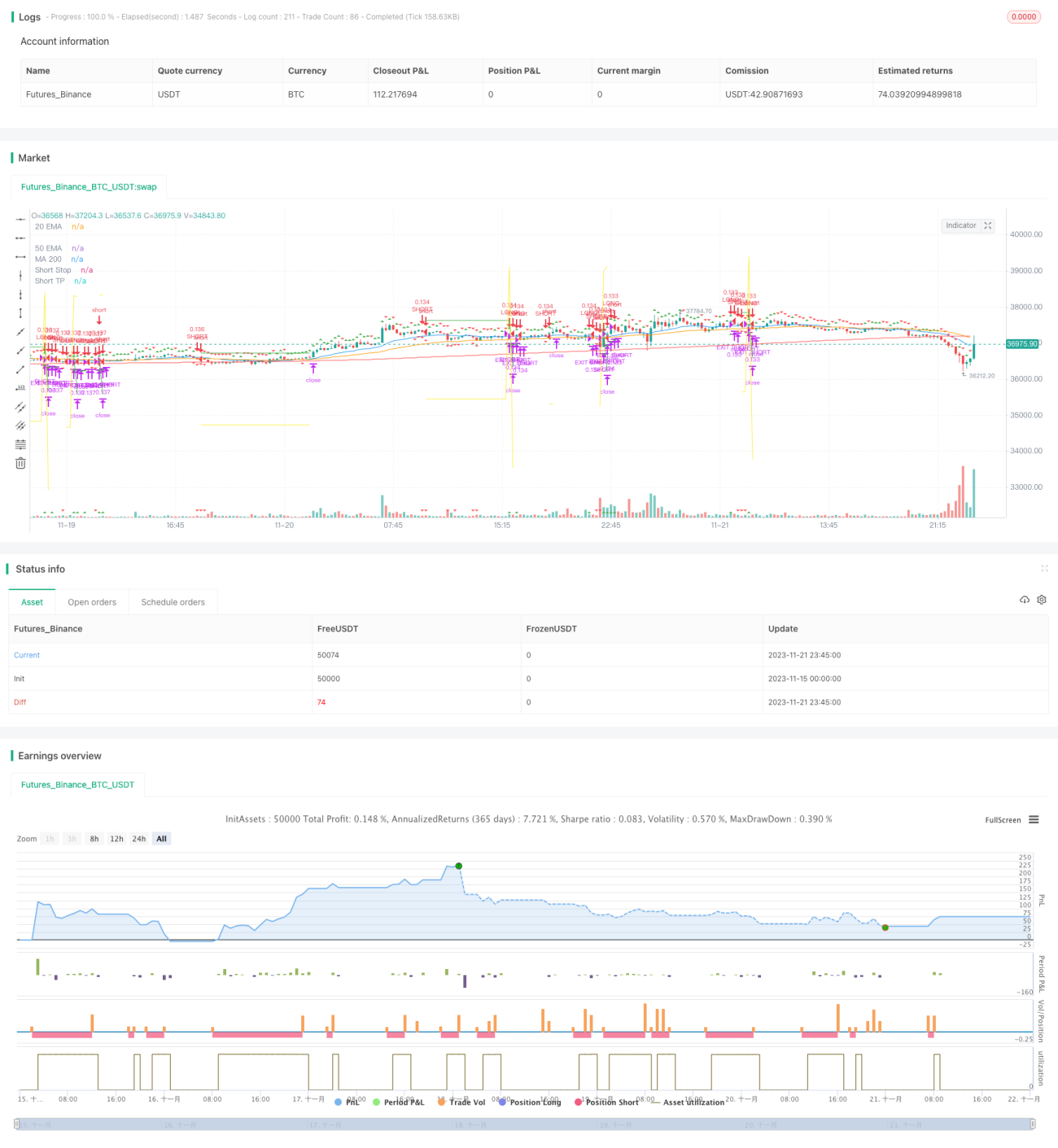

本戦略は、二つの時間枠とモメンタム指標を組み合わせ、適応型の利益確定・損切りを実現します。主要な時間枠でトレンド方向を監視し、補助的な時間枠でシグナルを確認します。両者の方向が一致した場合に取引シグナルを生成します。エントリー後は、段階的な利益確定方式で利確ラインと損切りラインを更新します。

戦略の原理

-

主時間枠では線形回帰指標Squeeze Momentum(SQM)を用いてトレンドを判断し、補助時間枠ではSQM指標のEMA(指数平滑移動平均)による組み合わせで偽シグナルをフィルタリングします。

-

主チャートのSQMが上方ブレイクし、補助チャートのSQMも上方にある場合に買い;主チャートのSQMが下方ブレイクし、補助チャートのSQMも下方にある場合に売りを行います。

-

エントリー後は、入力パラメータに基づいて初期の利益確定ラインと損切りラインを設定します。価格が利益確定ラインに達すると、利益確定ラインと損切りラインを更新します。具体的には、利益確定ラインは設定比率で段階的に上げ、損切りラインは比率で段階的に下げることで、漸進的な利益確定を実現します。

戦略の優位性

-

二つの時間枠で偽シグナルをフィルタリングし、シグナルの精度を確保します。

-

SQM指標でトレンド方向を判断するため、市場ノイズに惑わされにくい。

-

適応型の利益確定・損切りメカニズムにより、利益を最大限に確保し、リスクを効果的にコントロールします。

リスク分析

-

SQM指標のパラメータ設定が不適切だと、トレンドの転換点を見逃し、損失を招く可能性があります。

-

補助チャートの時間枠選択が不適切だと、ノイズを効果的にフィルタリングできず、誤った取引が発生する恐れがあります。

-

損切り幅の設定が大きすぎると、1回の損失が比較的大きくなる可能性があります。

最適化の方向性

-

SQM指標のパラメータは、市場に応じて調整し、その感度を確保する必要があります。

-

補助チャートの時間枠も異なる周期でテストし、どの周期が最も効果的にフィルタリングできるかを確認します。

-

損切り幅は固定値ではなく変動範囲を設定し、市場の変動度合いに応じて調整できるようにします。

まとめ

本戦略は全体的に非常に実用的であり、二つの時間枠とモメンタム指標を組み合わせてトレンドを判断し、適応型の利益確定・損切り方式で安定した収益を実現します。SQM指標のパラメータ、補助チャートの周期、損切り幅の設定を最適化することで、戦略の効果をさらに高めることができ、実取引での応用と改善に値します。

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1