マルチ指標トレンドフォロー戦略

概要

本戦略は、3つのオープンソース指標を組み合わせることでマルチタイムフレームのトレンド判断を実現し、ストップロス・利確を設定して利益を確定します。具体的には、AK MACD BBインジケーターで短期トレンド方向を判断し、SSLインジケーターで偽のシグナルを一部除去し、最後に出来高指標VSFで実際の買い・売り圧力を判断してエントリータイミングを図ります。同時に、戦略はあらかじめストップロスと利確ポイントを設定して利益を確定し、1回のトレードにおける損失リスクを大幅に低減します。

戦略の仕組み

-

AK MACD BBインジケーター

本インジケーターはボリンジャーバンドをMACD指標に適用し、MACDラインがボリンジャーバンドの上部バンドを突破したときに買いシグナル、下部バンドを突破したときに売りシグナルを生成します。

-

SSLインジケーター

SSLインジケーターは価格が移動平均線を突破したかどうかを判断し、リテストシグナルを検出します。価格が移動平均線を上抜けし、SSLインジケーターが青色の場合は上昇トレンド、価格が移動平均線を下抜けし、SSLインジケーターが赤色の場合は下降トレンドと判断し、トレードシグナルを発します。

-

VSFインジケーター

VSFインジケーターは買い手と売り手の力を判断します。本戦略では、買い手または売り手の力が50%を超えた場合にのみシグナルを出し、無効なブレイクを回避します。

-

ストップロス・利確

戦略には4段階のプログレッシブ利確があり、1.5倍から3倍の利益間隔で設定されています。同時に2%の固定ストップロスを設定し、1回のトレードの最大損失を効果的に制御します。

優位性分析

-

複数指標の組み合わせによる正確な判断

異なる指標によるマルチタイムフレームのトレンド判断により、偽シグナルをフィルタリングし、より正確な判断が可能です。

-

自動利確・ストップロスによるリスク管理

戦略に組み込まれた利確・ストップロス設定により、1回のトレードの損失を約2%に抑え、大きな損失を回避できます。

-

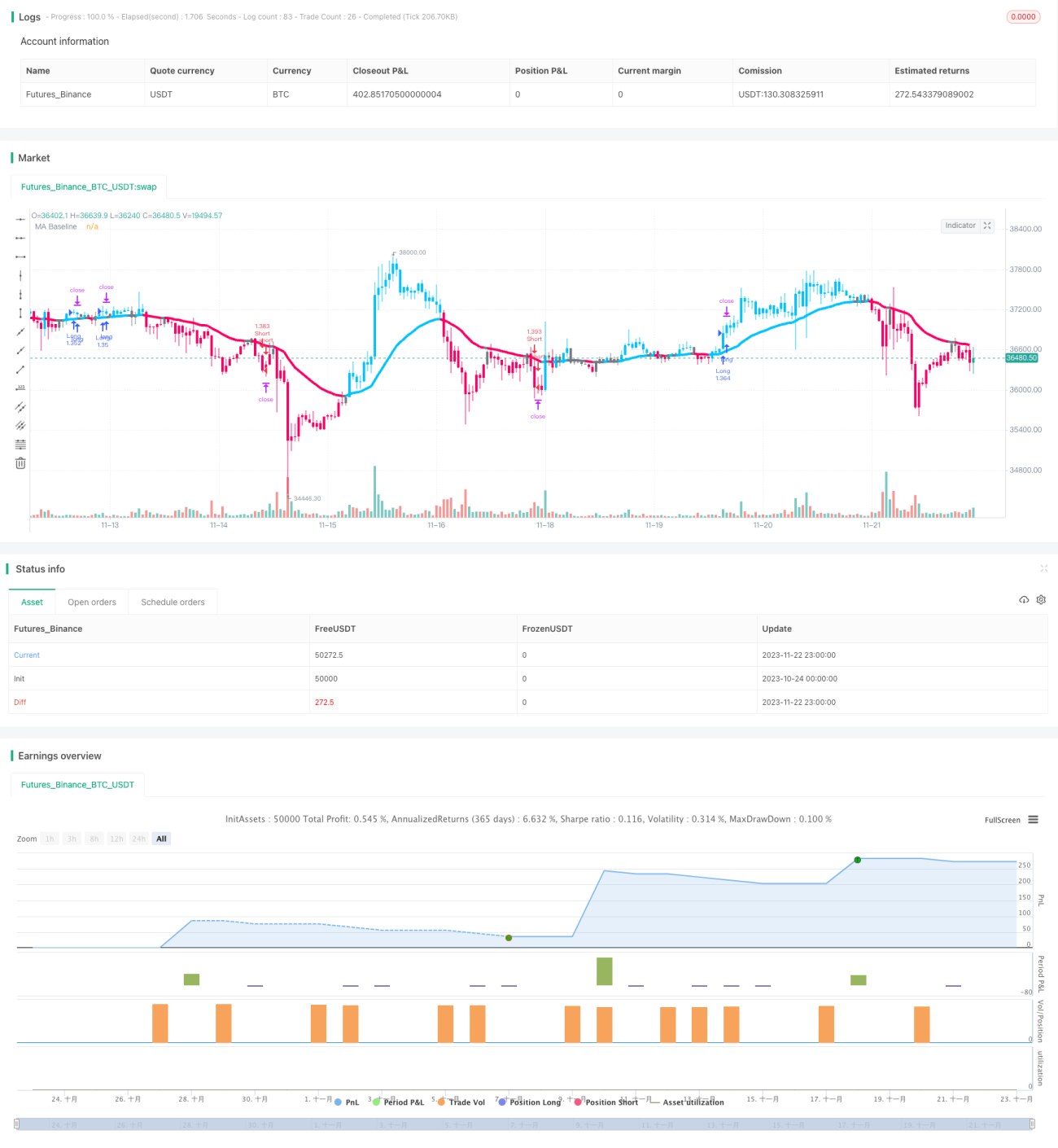

優れたバックテストデータ

公開者のバックテストによると、100トレード中、利益を出したトレードが74%を占め、総利益は427%に達しています。

リスクと対策分析

-

市場の急激な変動リスク

大きなレンジ相場では、小幅な損失が複数回発生する可能性があります。その場合は、固定ストップロスの幅を調整するか、トレードを一時停止します。

-

ロング・ショートの制限リスク

現状ではロング・ショート両方が可能です。ロングのみまたはショートのみに制限すると、利益を得る機会が半減します。

-

取引時間帯のリスク

戦略は5分足データで判断するため、1日の取引時間が数時間しかない場合、サンプル数が不足し、シグナルが信頼できない可能性があります。

戦略の最適化方向

-

ストップロス・利確パラメータの最適化

異なるストップロス・利確水準をテストし、最適なパラメータを見つけることができます。ストップロスが小さすぎるとリスクを効果的に制御できず、大きすぎるとさらなる利益を逃す可能性があります。

-

自動ポジション調整の追加

トレーリングストップや移動ストップロスを設定して利益を確定したり、特定の条件でポジションを追加して利益を増やすことが可能です。

-

他の指標との組み合わせ

異なる指標の組み合わせをテストし、どの組み合わせが最も効果的かを判断します。また、より多くの指標を追加してクロス検証を行うこともできます。

-

パラメータの最適化

異なるパラメータでバックテストを行い、最適化の方向性を見つけます。本戦略では、ボリンジャーバンドのパラメータや移動平均線のパラメータを変更することで、より良い結果が得られる可能性があります。

まとめ

本戦略は複数の指標を統合してトレンド方向を判断し、自動利確・ストップロスを設定することで、強いトレンドの中で利益を得るとともに、1回のトレードの損失を非常に小さな範囲に抑えることができます。公開者のバックテストデータを見ると、勝率と利益率は非常に良好です。さらなる最適化により、戦略の安定性と収益性の向上が期待できます。

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1