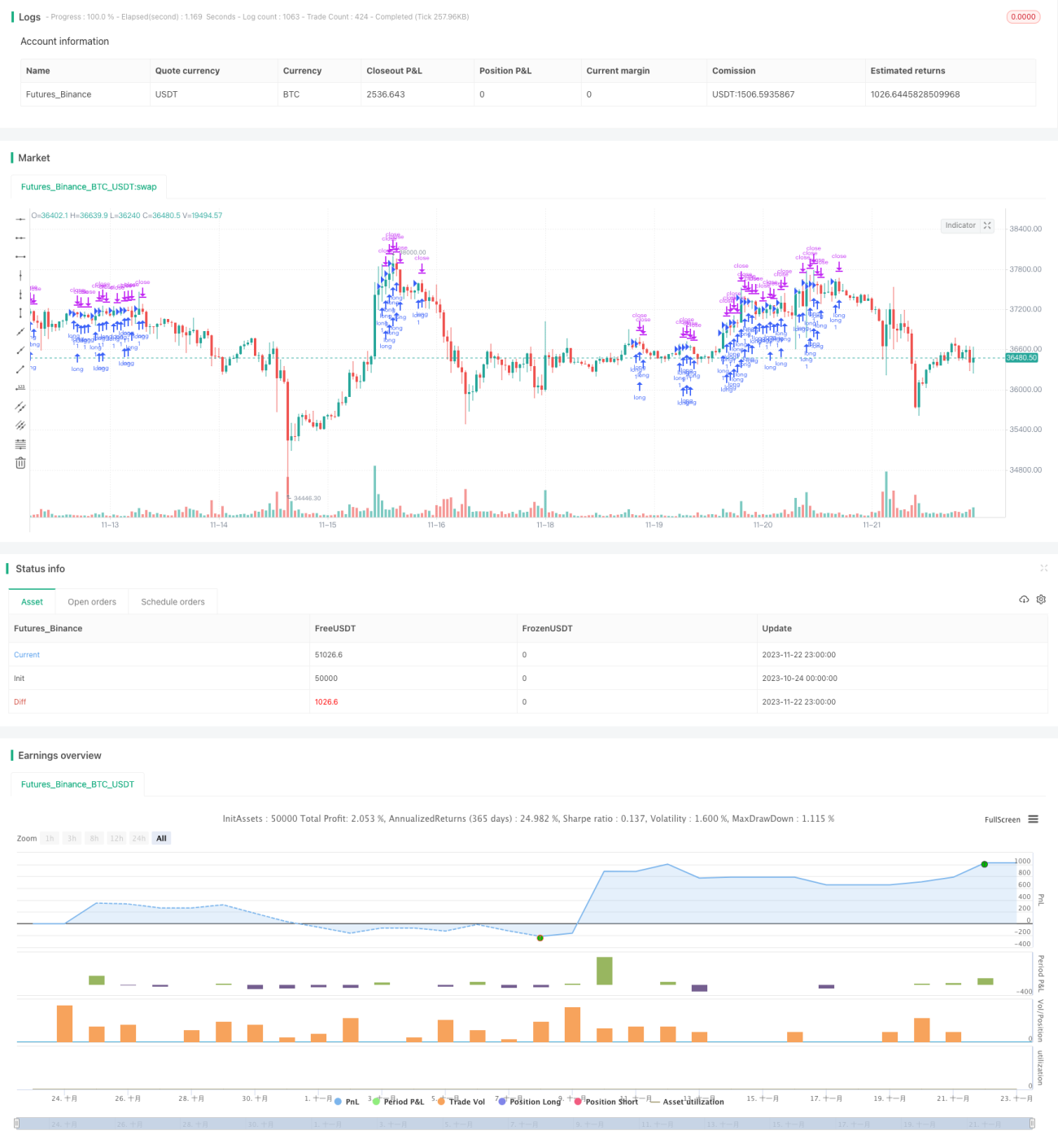

堅実で安定した移動平均システム戦略

概要

本戦略は、異なる4つの期間のSMMA(平滑移動平均線)と1つのEMA指標に基づく移動平均システムです。複数のテクニカル分析ツールを組み合わせ、トレンド判断を通じて取引戦略を形成します。主に高レバレッジ口座のEURUSD 15分足を用いたデイトレードを対象としています。

戦略の原理

本戦略では、異なるパラメータの4つのSMMA(3,6,9,50)と1つのEMA(200)を使用して、多層的な移動平均システムを構築します。SMMA指標は市場ノイズを効果的に除去し、トレンド方向を判断します。EMA指標は長期トレンドを検出します。具体的な取引ロジックは以下の通りです:

短期移動平均線(例:3期間SMMA)が長期移動平均線(例:200期間EMA)を上抜けたときに買いシグナルを生成します。短期移動平均線が長期移動平均線を下抜けたときに売りシグナルを生成します。これにより、複数の移動平均線の並び関係を判断してトレンド方向を特定します。

さらに、本戦略ではリスク管理のために利益確定・損切りポイントも設定しています。

優位性の分析

本戦略には以下の優位性があります:

- 多層的な移動平均線構造によりトレンド方向を効果的に判断し、偽シグナルを低減します。

- SMMA指標が市場ノイズを効果的に除去し、EMA指標が長期的なトレンドを捉えます。

- 高レバレッジ口座に適しており、取引収益を拡大できます。

- 利益確定・損切りポイントを設定しているため、リスクを効果的にコントロールできます。

- 取引対象(EURUSD)と時間軸(15分)を最適化しており、より有利な条件で取引できます。

リスク分析

本戦略には以下のリスクも存在します:

- 移動平均線を多用するため、短期的な反転のチャンスを逃す可能性があります。

- 高レバレッジは損失を拡大する一方で、利益も拡大します。

- 移動平均線がシグナルを生成した時点で、短期的な相場がすでに反転している可能性があります。

- EURUSD為替レートは激しく変動する可能性があり、より大きなリスクをもたらします。

これらのリスクに対しては、レバレッジ倍率を適宜調整したり、移動平均線のパラメータを最適化したり、相場反転を判断するための他の指標を導入するなどの対策が考えられます。

最適化の方向性

本戦略の主な最適化の方向性は以下の通りです:

- 異なる銘柄や時間軸でのパフォーマンスを評価し、最適なパラメータを選択します。

- 異なるパラメータの組み合わせや移動平均線の本数をテストします。

- 出来高やボラティリティ指標を追加して短期的な反転ポイントを判断します。

- 利益確定・損切りの幅を動的に調整します。

- ENU指標を追加して反転ポイントを判断します。

多角的なテストと最適化により、戦略の安定性と収益性を大幅に向上させることができます。

まとめ

本移動平均線戦略は、均線指標の利点を統合し、堅牢なトレンド判断システムを形成しています。取引対象と時間軸が最適化されており、高レバレッジのデイトレードに非常に適しています。パラメータ調整と最適化テストを通じて、本戦略は効率的で信頼性の高いアルゴリズム取引戦略となり得ます。

- 1