高値・安値ブレイクアウトのバックテスト戦略

概要

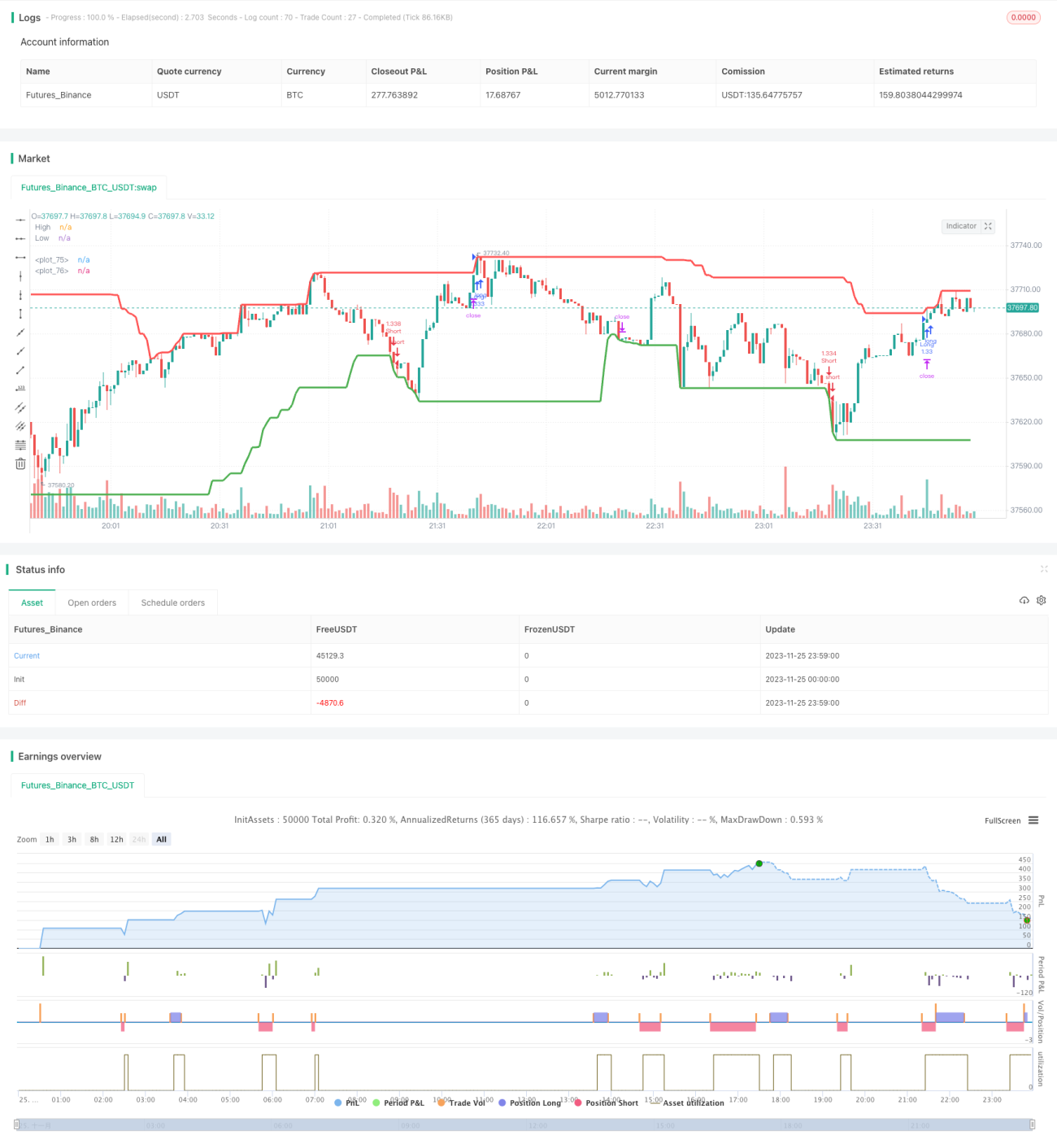

高値・安値ブレイクアウトバックテスト戦略は、株価の過去の高値・安値を利用し、価格がこれらの高値・安値を突破するかどうかを判断するトレンドフォロー戦略です。一定期間内の最高値と最安値を計算し、現在の期間の価格が直近の一定期間の最高値を超えた場合に買いシグナルを生成し、価格が直近の一定期間の最安値を下回った場合に売りシグナルを生成します。この戦略はトレンドフォロー戦略の一種であり、株価のトレンド特性を捉えることができ、実戦価値があります。

戦略の原理

この戦略の核となるロジックは、一定期間(デフォルトでは50本のローソク足)内の最高値と最安値を計算することです。最高値と最安値を計算する際には、終値を使用するか、最高値と最安値(デフォルトでは最高値と最安値を使用)を選択できます。次に、現在のローソク足の終値または最高値が直近の一定期間内の最高値を超えたかどうかを判断し、超えていて、かつ前回の最高値から一定期間(デフォルトでは30本のローソク足)が経過していれば、買いシグナルを生成します。同様に、現在のローソク足の終値または最安値が直近の一定期間内の最安値を下回ったかどうかを判断し、下回っていて、かつ前回の最安値から一定期間が経過していれば、売りシグナルを生成します。

買いシグナルが生成されると、戦略はその価格で買い注文を出し、ストップロス価格と利確価格を設定します。価格がストップロス価格に達すると、戦略は損失を確定してポジションをクローズし、価格が利確価格に達すると利益を確定してポジションをクローズします。売りシグナルのロジックも同様です。

優位性分析

この高値・安値ブレイクアウトバックテスト戦略には、以下の利点があります。

- 戦略のロジックがシンプルで、理解・実装が容易。

- 株価のトレンド特性を捉え、価格のトレンドに沿って取引できる。

- パラメータを調整することで最適なパラメータの組み合わせを見つけられる。

- ストップロスと利確の仕組みが組み込まれており、リスクをコントロールできる。

- 可視化された表示により、パラメータ調整と結果分析が大幅に容易になる。

リスク分析

この戦略には以下のようなリスクも存在します。

- 頻繁な取引や過剰取引が発生しやすい。

- 価格がレンジ相場の場合、ポジションが頻繁にオープンされる。

- 指標のパラメータが不適切な場合、大きなトレンド機会を逃す可能性がある。

- 株価の変動頻度や振幅を考慮していない。

- 他の指標と組み合わせてシグナルを検証していない。

これらのリスクをコントロールするためには、以下の点から最適化を行うことができます。

- ストップロスの幅を適切に狭め、ポジション保有時間を長くする。

- ポジションオープンの条件を追加し、頻繁なエントリーを避ける。

- パラメータを最適化し、最適な組み合わせを見つける。

- 他の指標を組み合わせてシグナルをフィルタリングする。

最適化の方向性

この高値・安値ブレイクアウトバックテスト戦略は、以下の点から最適化が可能です。

-

パラメータ最適化:異なるパラメータの組み合わせをより体系的にテストし、最適なパラメータを見つける。

-

他の指標を組み合わせたシグナルフィルタリング:例えば、移動平均線指標を組み合わせ、価格が最高値を突破した時点で、かつ短期移動平均線が長期移動平均線を上抜けた場合のみ買いシグナルを生成する。

-

株価の変動頻度を考慮:例えばATR指標を組み合わせ、株価の変動が大きい場合は、ブレイクアウトの幅を適宜広げる。

-

トレンド相場とレンジ相場を区別:トレンドが明確な局面ではパラメータを緩めてトレンドに追随し、レンジ相場ではパラメータを引き締める。

-

ポジション管理メカニズムの追加:例えば、損失が一定比率に達した場合に新規エントリーを停止するなど。

まとめ

総じて、高値・安値ブレイクアウトバックテスト戦略は、シンプルで実用的なトレンドフォロー戦略です。一定期間内の最高値と最安値を価格が突破するかどうかを判断して取引シグナルを決定します。この戦略は、シンプルさ、トレンドフォロー、パラメータ最適化が可能などの利点がある一方で、過剰取引の発生やレンジ相場への対応ができないなどのリスクも存在します。パラメータ最適化、指標によるフィルタリング、ポジション管理など、複数の側面からこの戦略を最適化することで、その効果をさらに高めることができます。

/*backtest

start: 2023-11-25 00:00:00

end: 2023-11-26 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("High/Low Breaker Backtest 1.0", overlay=true, initial_capital=1000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, max_bars_back=700)

// Strategy Settings- 1