モメンタム商品選択指数戦略

概要

モメンタム商品選択指数(Commodity Selection Index、CSI)戦略は、市場のモメンタムを追跡する短期取引戦略です。商品のトレンド性と変動性を計算することで、強いモメンタムを持つ商品を特定し取引を行います。この戦略は、ウェルズ・ワイルダー(Welles Wilder)が著書『New Concepts in Technical Trading Systems』で提唱しました。

戦略の原理

この戦略の中核指標はCSI指数であり、商品のトレンド性と変動性を総合的に考慮します。具体的な計算方法は以下の通りです。

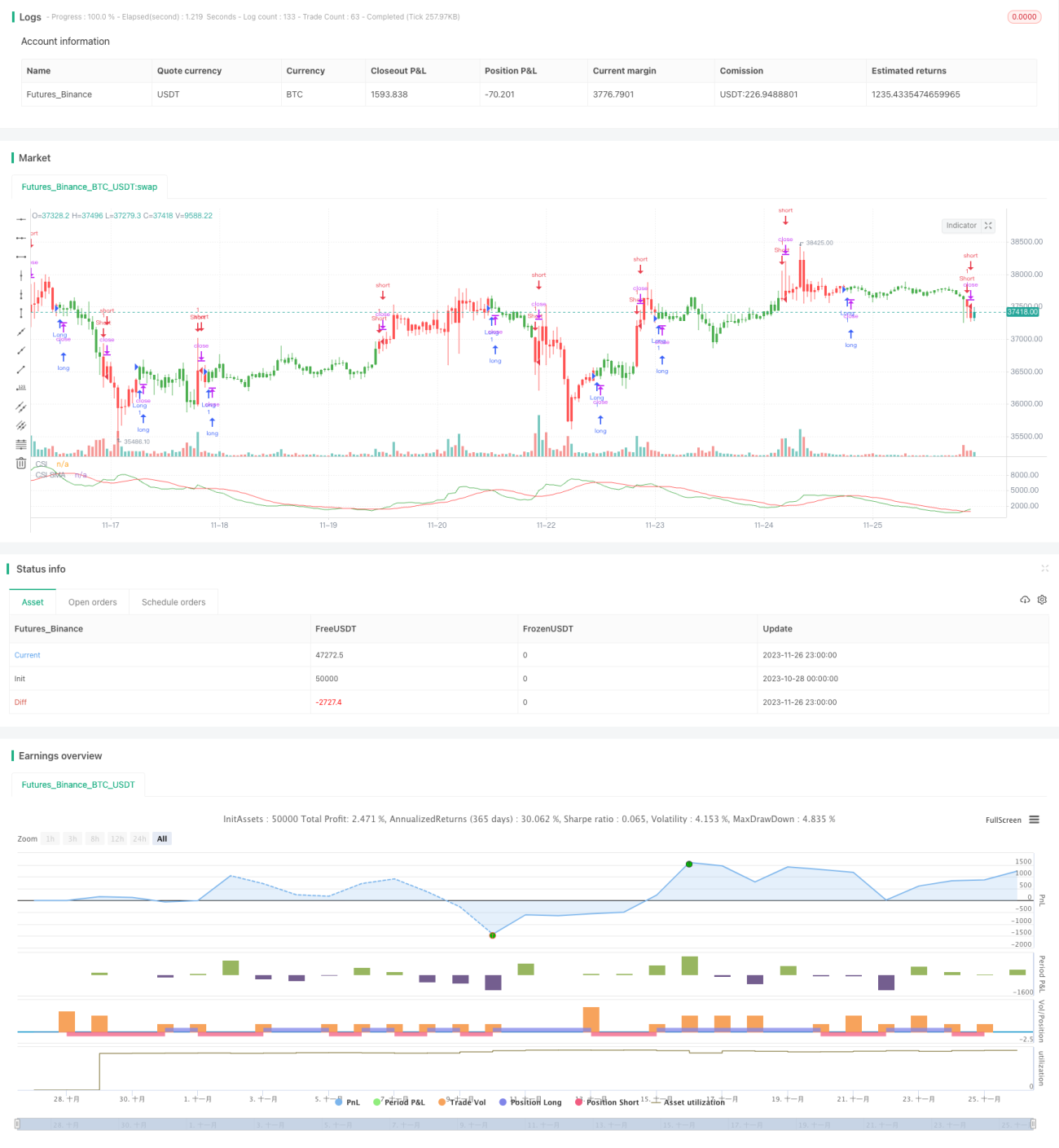

CSI = K × ATR × ((ADX + ADXのn日移動平均線) / 2)

ここで、Kはスケーリング係数、ATRは平均真のレンジ(平均真実変動幅)を表し、市場の変動性を測定します。ADXは平均方向性指数を表し、市場のトレンド性を反映します。

各商品のCSI指数値を計算し、そのn日単純移動平均線と比較します。CSIが移動平均線を上回った場合に買いシグナル、下回った場合に売りシグナルが発生します。

この戦略はCSI指数が高い商品を選択して取引します。これらの商品は強いトレンド性と変動性を持ち、短期間でより大きな利益を得る可能性があります。

優位性分析

この戦略には以下のような優位性があります。

- 市場のモメンタムを捉え、商品のトレンド性と変動性の特性を最大限に活用できます。

- 二重の指標を用いることで、取引シグナルの信頼性が高まります。

- シンプルで明確な取引ルールにより、自動取引に適しています。

- 短期取引に特化して設計されており、短期的な機会を迅速に捉えることができます。

リスク分析

この戦略には以下のようなリスクも存在します。

- テクニカル指標に過度に依存するため、誤ったシグナルが発生する可能性があります。

- モメンタムを追跡する特性上、短期取引にのみ適しています。

- 変動が大きすぎるとストップロスが発動され、取引に損失が生じる可能性があります。

- ある程度のレバレッジ水準に耐える必要があり、その結果、より大きな資金リスクに直面します。

リスクを管理するためには、ストップロス水準を適切に設定し、1回のポジションサイズを制御し、異なる市場環境に適合するようパラメータを適宜調整する必要があります。

最適化の方向性

この戦略は以下の側面から最適化が可能です。

- より多くのパラメータ組み合わせをテストし、最適なパラメータを探し出す。

- 他の補助指標を追加してシグナルをフィルタリングする。

- ボラティリティ逆転などの他の戦略と組み合わせてポートフォリオを構成する。

- 機械学習を利用してモデルを訓練し、より信頼性の高い取引シグナルを生成する。

まとめ

モメンタム商品選択指数戦略は、市場におけるトレンド性が強く変動性の大きい商品を捉えることで、シンプルかつ迅速な短期取引を実現します。このモメンタム追跡に特化したアプローチにより、シグナルは明確で、自動化が容易です。もちろん、リスク管理に注意を払い、市場環境の変化に適応するために継続的に改善・アップグレードを行う必要があります。

/*backtest

start: 2023-10-28 00:00:00

end: 2023-11-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 20/03/2019

// The Commodity Selection Index ("CSI") is a momentum indicator. It was - 1