過去データに基づく動的サポート・レジスタンス戦略

概要

本戦略は、過去の高値・安値・終値の動的計算に基づきサポート・レジスタンスラインを求め、それを元に取引シグナルを生成します。この戦略は中長期のポジション保有に適しており、市場のサポート・レジスタンスを効果的に活用して利益を獲得できます。

戦略の原理

-

前の期間の高値・安値・終値の平均値を計算し、基準点PPとします。

-

3本のサポートラインを計算します:S1 = 2PP - 高値;S2 = PP - (R1-S1);S3 = 安値 - 2(高値-PP)。

-

3本のレジスタンスラインを計算します:R1 = 2PP - 安値;R2 = PP + (R1-S1);R3 = 高値 + 2(PP-安値)。

-

価格がレジスタンスラインを上抜けたらロング、サポートラインを下抜けたらショートとします。

優位性分析

-

過去データに基づき計算されるサポート・レジスタンスラインは動的に変化するため、市場構造をリアルタイムで捉えられます。

-

複数階層のサポート・レジスタンス設定により、リスク管理の最適化が可能です。

-

取引シグナルと損切りの方法がシンプルで直感的です。

リスク分析

-

高ボラティリティ相場では、過去データから得られる参考価格帯が機能しなくなる可能性があります。

-

ロングとショートのポジションを切り替える際には、取引コストを考慮する必要があります。

-

データの品質を確保し、計算ミスを防ぐ必要があります。

最適化の方向性

-

過去データの参照を拡充し、例えば100日移動平均線などを導入することを検討できます。

-

ポジション管理の最適化、例えばボラティリティに基づいてポジション比率を調整します。

-

ストップロス戦略の追加、例えばトレーリングストップや資金管理に基づくストップロスを検討します。

まとめ

本戦略は、過去のサポート・レジスタンスの概念に基づき、複数階層の参考価格帯を提供します。戦略はシンプルかつ直接的で、中長期のポジション保有による利益獲得に適しています。同時に、高ボラティリティ市場のリスクや取引コストの管理にも注意が必要です。さらなる最適化により、複雑な環境でも安定して動作する戦略にできます。

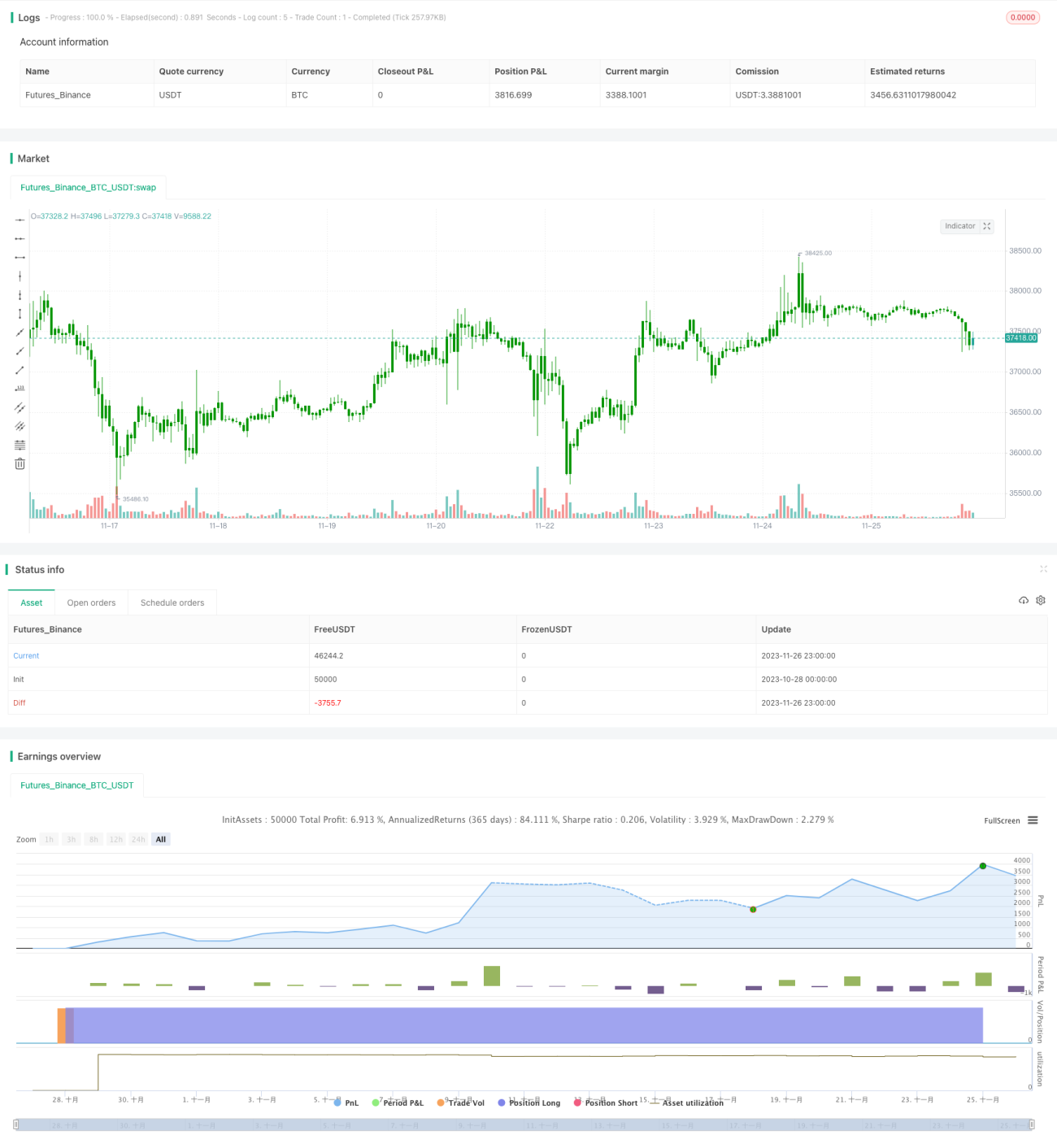

/*backtest

start: 2023-10-28 00:00:00

end: 2023-11-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 09/06/2020

// Pivot points simply took the high, low, and closing price from the previous period and - 1