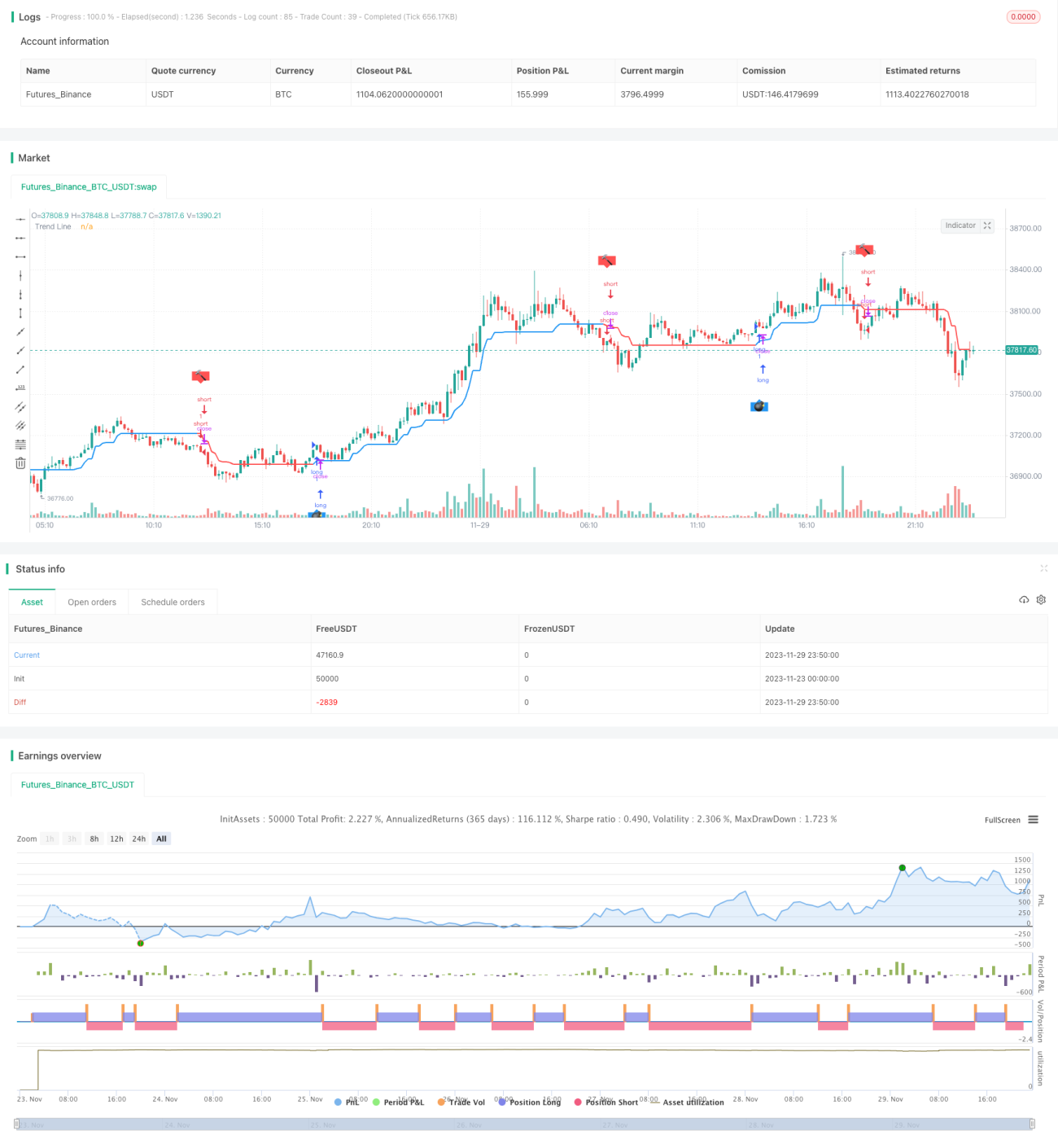

概要

トレンドライン戦略は、ボリンジャーバンド指標とATR(平均真のレンジ)を利用したトレンドフォロー戦略です。トレンド判定ラインを動的に調整し、ボリンジャーバンドの上部バンドを突破した場合は上方に、下部バンドを突破した場合は下方に調整することで、トレンドの判断と追跡を行います。

戦略の原理

本戦略はまず、ボリンジャーバンドの上部バンドと下部バンド、および平均真のレンジ(ATR)を計算します。その後、価格がボリンジャーバンドの上部バンドまたは下部バンドを突破したかどうかを判定します。

価格が上部バンドを突破した場合、ATRフィルターが有効になっていれば、トレンド判定ラインを最安値からATRを引いた値に設定します。ATRフィルターが無効な場合は、最安値そのものを設定します。

価格が下部バンドを突破した場合、ATRフィルターが有効になっていれば、トレンド判定ラインを最高値にATRを加えた値に設定します。ATRフィルターが無効な場合は、最高値そのものを設定します。

これにより、トレンド判定ラインは価格がボリンジャーバンドの上下バンドを突破するたびに動的に調整され、トレンドの判断が可能になります。

現在のトレンド判定ラインが前回のラインより高い場合、上昇トレンドと判断します。現在のラインが前回より低い場合、下降トレンドと判断します。

トレンド判断に基づき、本戦略はロングまたはショートのポジションを取ることができます。

優位性分析

- トレンド判定ラインを動的に調整するため、価格トレンドを柔軟に捉えることができます。

- ボリンジャーバンド指標と組み合わせることで、価格突破時にトレンド転換をタイムリーに判断できます。

- ATRパラメータの導入により、一部の偽のブレイクアウトシグナルをフィルタリングできます。

リスク分析

- ボリンジャーバンドのパラメータ設定が不適切な場合、頻繁な偽のブレイクアウトが発生する可能性があります。

- ATRパラメータが大きすぎると、トレンド転換の機会を逃す可能性があります。

- 極端な相場変動による損失を防ぐため、ストップロスの考慮が必要です。

パラメータ調整やストップロスの導入により、一部のリスクを回避できます。また、他の指標と組み合わせてフィルタリングすることで、ブレイクアウトの有効性を高めることも可能です。

最適化の方向性

- ボリンジャーバンドとATRのパラメータを最適化し、最適な設定を探します。

- 他の指標を追加して偽のブレイクアウトをフィルタリングします。

- 特定の取引銘柄に合わせて、ボリンジャーバンドの期間とATRの期間を選択します。

まとめ

トレンドライン戦略は、ボラティリティの高い相場で価格トレンドを捉えることを目指した、効果的なトレンドフォロー戦略です。パラメータ調整と最適化により、良好な収益を得ることが可能です。ただし、リスク管理やストップロス、偽のブレイクアウトへの対策も考慮する必要があります。本戦略を他の指標や戦略と組み合わせて使用することで、さらに利益率を高めることが推奨されます。

/*backtest

start: 2023-11-23 00:00:00

end: 2023-11-30 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Dreadblitz

//@version=4

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒ //- 1