二重指標買いフィルター買いシグナル戦略

概要

二重指標フィルター買いフィルター買いシグナル戦略は、ストキャスティックRSI(確率的指数平滑移動平均線)とボリンジャーバンドの組み合わせを利用して、潜在的な買い機会を特定します。この戦略は複数のフィルター条件を採用し、最も有利な買いポイントを区別します。これにより、相場が変動する環境でも、高い確率の買いタイミングを識別できます。

戦略の仕組み

本戦略は2つの指標グループを使用して買い機会を識別します。

まず、ストキャスティックRSIを使用して市場が売られ過ぎかどうかを判断します。この指標は確率的指数とその平滑移動平均線を組み合わせ、%Kラインが安値から%Dラインを上抜けた時を売られ過ぎシグナルとみなします。ここでは閾値を設定し、%Kラインが20を超えている場合を売られ過ぎとします。

次に、ボリンジャーバンドを使用して価格変動を識別します。ボリンジャーバンドは価格の標準偏差に基づいて上限・下限バンドを計算します。価格が下限バンドに近づくと、売られ過ぎ状態となります。本戦略では2倍標準偏差のパラメータを設定し、バンドの範囲を広げることで偽シグナルをさらにフィルタリングします。

上記2つの指標で売られ過ぎシグナルを得た後、戦略はさらに複数のフィルター条件を追加し、買いタイミングをより詳細に識別します:

- 価格がボリンジャーバンドの下限バンドを上にブレイクしたばかり

- 現在の終値がN本前のローソク足の終値より高い(買いの勢いを示す)

- 現在の終値が長期または中期の過去終値より低い(押し目買いに有利)

これらの条件を総合的に判断して識別された買いタイミングで買いシグナルを発します。

優位性分析

この二重指標フィルター戦略にはいくつかの大きな利点があります:

- 二重指標で判断することで、買いシグナルの信頼性が高まり、偽シグナルを回避できます。

- 複数のフィルター条件により、レンジ相場での頻繁な買いを防ぎます。

- ストキャスティックRSIで売られ過ぎ状態を、ボリンジャーバンドで価格の異常を判断します。

- 価格の勢い判断を追加し、十分な買いの力を確保します。

- 押し目判断を追加し、買いポイントの信頼性をさらに高めます。

総じて、本戦略は複数のテクニカル指標とフィルター手段を総合的に活用することで、買いタイミングの識別をより正確かつ信頼性の高いものにし、優れたトレードパフォーマンスを実現します。

リスク分析

二重指標フィルター戦略には多くの利点がある一方で、注意すべきリスクも存在します:

- パラメータ設定が不適切だと、買いシグナルが多すぎたり少なすぎたりするため、綿密なテストと最適化が必要です。

- 複数のフィルター条件により一部の買い機会を逃す可能性があり、急激な相場変動に対応できないことがあります。

- 指標が乖離した場合、誤ったシグナルが発生するため、指標の整合性に注意が必要です。

- トレンドを判断できないため、弱気相場では誤ったシグナルで損失を出す可能性があります。

これらのリスクに対して、本戦略は以下のように最適化できます:

- 指標パラメータを調整し、フィルター条件の感度をバランスさせる。

- トレンド判断指標の助けを借りて、弱気相場での誤シグナルを回避する。

- ストップロス手段を追加する。

最適化の方向性

本二重指標フィルター戦略は、以下の次元でさらに最適化できます:

- より多くのテクニカル指標の組み合わせをテストし、より良い買いタイミング判断方法を探す。例:VRSI、DMIなど。

- 機械学習アルゴリズムを追加し、パラメータを自動最適化する。

- 適応型ストップロス機構を追加。利益が一定水準に達したら、徐々にストップロスラインを引き上げる。

- 出来高指標を組み合わせ、十分な買いの力が存在することを確認する。

- 資金管理戦略を最適化。動的な取引数量を設定し、1回の損失を低減する。

より高度な技術や手法を取り入れることで、本二重指標フィルター戦略はより正確な買いタイミング選択と強力なリスク管理能力を得ることができます。これにより、実運用でより安定した信頼性の高い収益を実現します。

まとめ

以上より、二重指標買いフィルター買いシグナル戦略は、ストキャスティックRSIやボリンジャーバンドなどの複数のテクニカル指標と、価格の勢いや押し目判断などの複数のフィルター条件を組み合わせることで、高い確率で信頼性の高い買いタイミングを識別します。パラメータ最適化、ストップロス設定などのさらなる改良により、本戦略は安定した収益をもたらす定量取引戦略の一つとなり得ます。

その中核的な優位性は、指標とフィルター条件の効果的な組み合わせにより、買いタイミング判断がより正確になることです。リスクや最適化の方向性も制御可能かつ解決可能です。総合的に見て、これは実運用可能な効率的な定量戦略です。

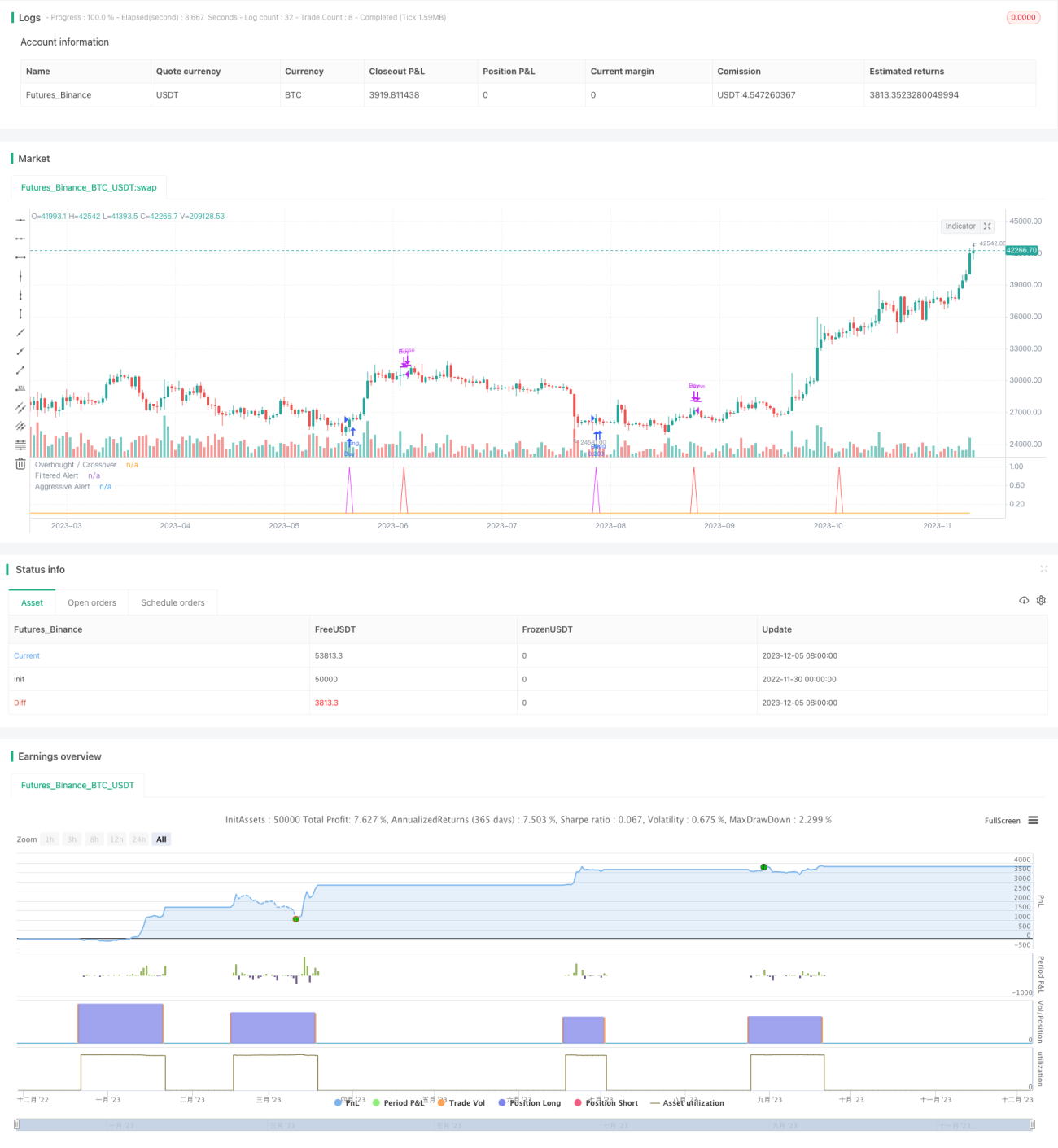

/*backtest

start: 2022-11-30 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SORAN Buy and Close Buy", pyramiding=1, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=10, overlay=false)

////Buy and Close-Buy messages- 1