二因子クォンツトレーディング戦略

概要

本戦略は、123反転と素数オシレーター指標という2つのファクターを組み合わせた、デュアルファクター駆動の定量取引戦略です。この戦略は短期的な反転機会を捉えると同時に、より長期的なトレンドを識別し、低リスクで超過リターンを実現します。

戦略の原理

第一部分は123反転戦略です。この戦略は2日間の終値の反転特性を利用して売買ポイントを判断します。終値が2日連続で上昇し、かつ低速Kラインが50未満の場合、行き過ぎた修正と見なし買いシグナルを発生させます。終値が2日連続で下落し、かつ高速Kラインが50超の場合、リバウンドが過剰と見なし売りシグナルを発生させます。

第二部分は素数オシレーター指標戦略です。この指標は指定された価格範囲内で現在の価格に最も近い素数を計算し、現在の価格との差を出力します。正の値は現在価格が素数の上限に近いことを示し、負の値は現在価格が素数の下限に近いことを示します。この差に基づいてトレンドを判断し、123反転シグナルと組み合わせて最終的な取引シグナルを生成します。

2つのサブ戦略の取引シグナルを統合するルールは、同方向のシグナルの場合に実際の取引シグナルを生成し、異方向のシグナルの場合は新規ポジションを開かないというものです。

優位性分析

本戦略は二重ファクターを組み合わせることで、短期的な反転効果と長期的なトレンド特性の両方を考慮し、多角的に市場を判断するため、戦略のリスク耐性が向上します。

単一のモメンタム戦略と比較して、本戦略は突発的なイベントにより価格が一時的に急落した場合に、反転ファクターを用いて迅速に損切りまたは逆張りポジションを取ることができ、日内リスクを効果的にコントロールします。

単一の反転戦略と比較して、本戦略は素数オシレーター指標を導入してトレンド方向を判断するため、頻繁な反転取引によるオーバートレーディングを回避できます。

リスク分析

本戦略の最大のリスクは、2つのファクター間でシグナルの矛盾が生じるケースです。123反転が買われ過ぎ・売られ過ぎの兆候を示し反転シグナルを発生させている一方で、素数オシレーター指標がトレンド継続を示している場合、そのまま反転取引を行うと損失が発生する可能性があります。

このリスクをコントロールするため、戦略には追加の判断ロジックが組み込まれており、2つのファクターのシグナルが同方向の場合にのみ実際の取引シグナルを生成します。ただし、これにより一部の取引機会を逃す可能性もあります。

最適化の方向性

-

ストキャスティクス指標のパラメータを最適化し、特定の銘柄により適した反転パラメータの組み合わせを見つける

-

素数オシレーター指標の許容誤差パーセントパラメータを最適化し、ノイズ取引を低減する

-

ストップロス戦略を追加し、一方向の相場で損失が拡大するのを防ぐ

-

ポジション管理モジュールを追加し、異なる市場環境に応じてポジションサイズを調整する

-

機械学習モデルを導入して2つのファクターのシグナル信頼度を評価し、シグナル矛盾の確率を低減する

まとめ

本戦略は短期反転ファクターと長期トレンドファクターをうまく組み合わせ、低リスクで定量取引を実現します。二重ファクターを効果的に活用してノイズ取引をフィルタリングし、追加の判断ロジックを設定してリスクをコントロールすることで、安定した収益を目指す実戦的な戦略です。今後もパラメータ最適化と機能拡張を継続し、実際の市場特性にさらに適応するよう改善していきます。

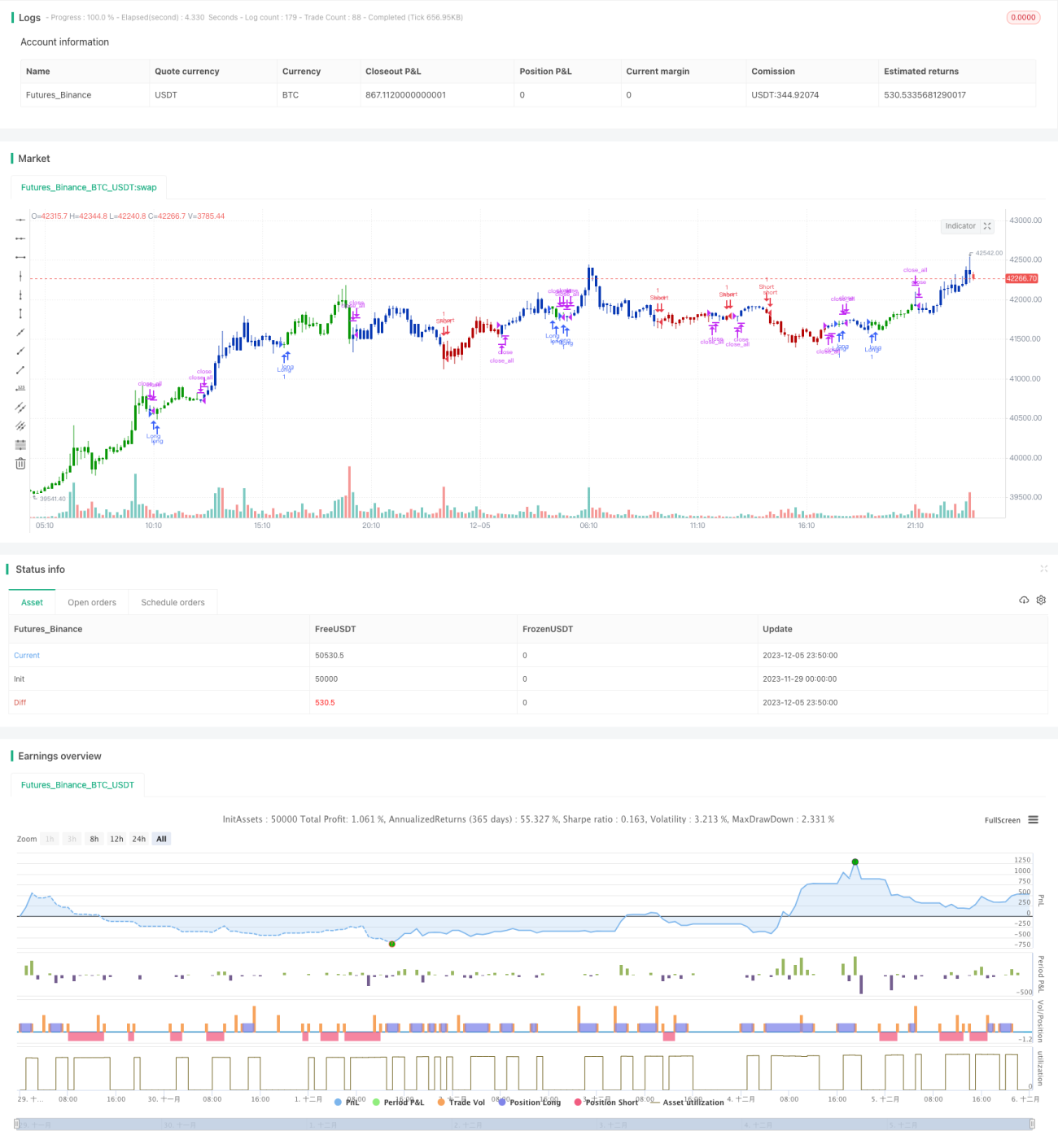

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/04/2021

// This is combo strategies for get a cumulative signal. - 1